IN THE HIGH COURT OF KARNATAKA AT BENGALURU

S.R. KRISHNA KUMAR, J.

Sri. Kewal Chand Jain, S/o Sri Hastimal Jain - Petitioner

Versus

The Assistant Commissioner Of Income Tax - Respondent

WRIT PETITION NO. 20135 OF 2021 (T-IT)

Decided On : 11-12-2025

| Table of Content |

|---|

| 1. petitioner seeks judicial review. (Para 1 , 2) |

| 2. petitioner's arguments on jurisdiction. (Para 3) |

| 3. requirement of incriminating evidence for assessment. (Para 5 , 9) |

| 4. court's interpretation of section 153c. (Para 6) |

RDER :

S.R.KRISHNA KUMAR, J.

In this petition, petitioner seeks for the following reliefs:-

“ a) Issue a writ of Certiorari and direction in the nature of a writ of certiorari quashing the assessment order passed by the Respondent under Section 153C read with Section 144 of the Income-tax Act, 1961 dated 30.09.2021 for the assessment year 201-16 herein as Annexure-A1.

b) Issue a writ of Certiorari and direction in the nature of is writ of certiorari quashing the computation sheet issued by the Respondent dated 30.09.2021 in respect of assessment year 2015-16 herein marked as Annexure-A2.

c) Issue a writ of Certiorari and direction in the nature of a writ of certiorari quashing the Notice of demand issued under section 156 of the Income –tax Act, 1961 by the Respondent dated: 30.09.2021in respect of assessment year 2015-16, for the payment of Rs.99,15,732/- herein marked as Annexure-A3.

d) Issue a writ of Certiorari and direction in the nature of a writ of certiorari quashing the Notice of penalty under section 274 read with section 271(1) (c) of the Income-tax Act, 1961 dated 03.09.2021 in respect of assessment year 2015-16 herein marked as Annexure-A4.

e) Declare that the assessment order (Annexure-A1) passed under section 153C read with section 144 of the Income-tax Act, 1961 is without jurisdiction.

f) And pass such other orders as this Hon'ble Court deems fit and proper in the interest of justice and equity.”

2. Heard learned Senior counsel for the petitioner and learned counsel for the respondents – revenue and perused the material on record.

3. In addition to reiterating the various contentions urged in the petition and referring to the material on record, learned Senior counsel for the petitioner submits that the impugned assessment order is illegal and arbitrary and contrary to law and facts for the following reasons:-

(a) The notice issued under Section 153C of the Act is without jurisdiction and bad in law.

(b) The assessment order dated 30.09.2021 passed under Section 153C r/w Section 144 of the Act is barred by limitation.

(c) The assessment order passed without issuance of notice under section 143(2) of the Act is bad in law.

(d) The assessment order passed under Section 153C of the Act is unsigned.

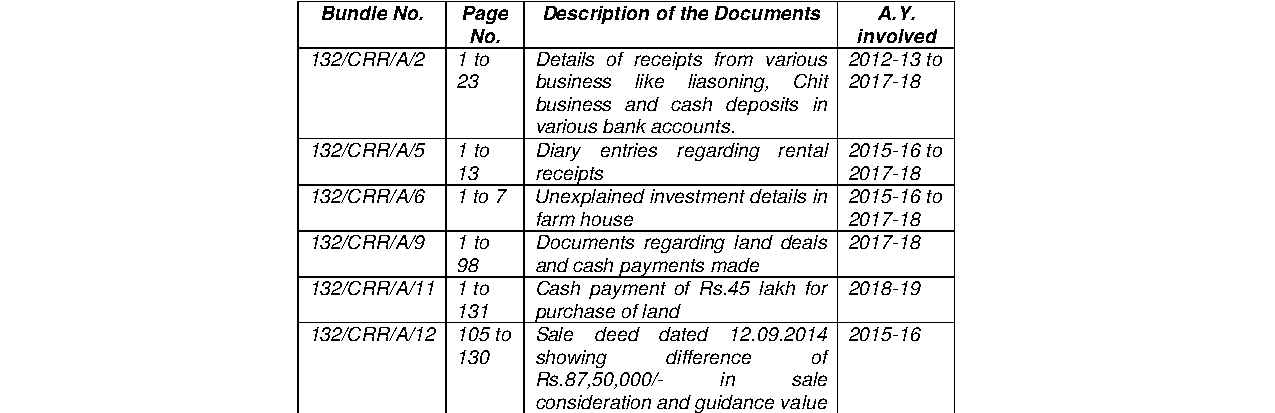

(e) The reasons recorded indicate that the seized documents pertain to the petitioner but have a bearing on the income for the A.Y.2020-21 and consequently, the notice issued for A.Y. 2015-16 is bad in law.

(f) The notice under Section 153C of the Act does not indicate whether the Respondent proposes to assess or reassess the income of the petitioner and consequently the same is defective and bad in law.

(g) The addition made in the assessment order is Rs.80,00,000/- while in the computation sheet it is taken as Rs.1,60,000/- without any basis.

(h) The assessment order passed is in violation of principles of natural justice.

(i) The transfer of case without serving notification under Section 127 of the Act is bad in law.

4. Per contra, leaned counsel for the respondents – revenue submits that there is no merit in the petition and that the same is liable to be dismissed.

5. A perusal of the material on record will indicate that insofar as the first ground urged by the petitioner that he was a ‘searched person’, since his premises was searched and consequently, the impugned proceedings and issuance of notice under Section 153C of the Income Tax Act, 1961 (for short ‘the I.T.Act’) as against the petitioner were not maintainable and is directly and squarely covered by the judgment of this Court in the case of C.R. Ram Mohan Raju vs. The Deputy Commissioner of Income Tax - W.P. No.33057/2024 dated 27.10.2025, wherein it is held as under:-

“7. Before adverting to the rival submissions, it would be apposite to ext

The court ruled that assessment orders under Section 153C of the Income Tax Act are void if the petitioner was a searched person and no incriminating evidence was found linking them to potential undi....

For invoking Section 153C, the petitioner must not be treated as a non-searched person; proper jurisdiction requires a satisfaction note linking seized documents to undisclosed income of another part....

The court held that a petitioner searched under Section 132 of the Income Tax Act cannot be treated as a non-searched person for proceedings under Section 153C, and thus impugned notices issued again....

A person may only be assessed under Section 153C of the Income Tax Act if they are not the 'searched person'; procedural safeguards must precede assessment actions.

The court held that in cases of search under Section 132, the provisions of Section 153A apply mandatorily, overriding Section 147 and 148, unless incriminating material is found.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :