2025 KHC 42657

IN THE HIGH COURT OF KARNATAKA AT BENGALURU

S.R.KRISHNA KUMAR, J.

Sri. C. R. Ram Mohan Raju S/o Changama Raju - Appellant

Vs.

The Deputy Commissioner Of Income Tax - Respondent

Writ Petition No. 33057 of 2024 (T-IT)

Decided On : 27-10-2025

Advocate Appeared :

For the Appellant : Sri. A.Shankar, Senior Counsel For Sri. Chandrasekhar V., Advocate

For the Respondent : Sri.Y.V.Raviraj And Sri.M.Dilip, Advocates

| Table of Content |

|---|

| 1. petition for quashing income tax notices. (Para 1 , 3) |

| 2. court's observations on procedural fairness. (Para 2 , 6 , 7) |

| 3. arguments on applicability of section 153c. (Para 4 , 5) |

| 4. conclusion of quashing invalid notices. (Para 10 , 14 , 15) |

| 5. definition and requirements for invoking section 153c. (Para 12) |

ORDER :

S.R.KRISHNA KUMAR, J.

In this petition, petitioner seeks quashing of the impugned Notices issued by the 1st respondent to the petitioner for the assessment years 2011-12, 2012-13, 2013-14, 2014-15, 2015-16, 2016-17, 2017-18 and 2018-19 under Section 153C of the Income Act, 1961 (for short ‘the I.T.Act’) and for other reliefs.

2. Heard learned Senior counsel for the petitioner and learned counsel for the respondents – Revenue and perused the material on record.

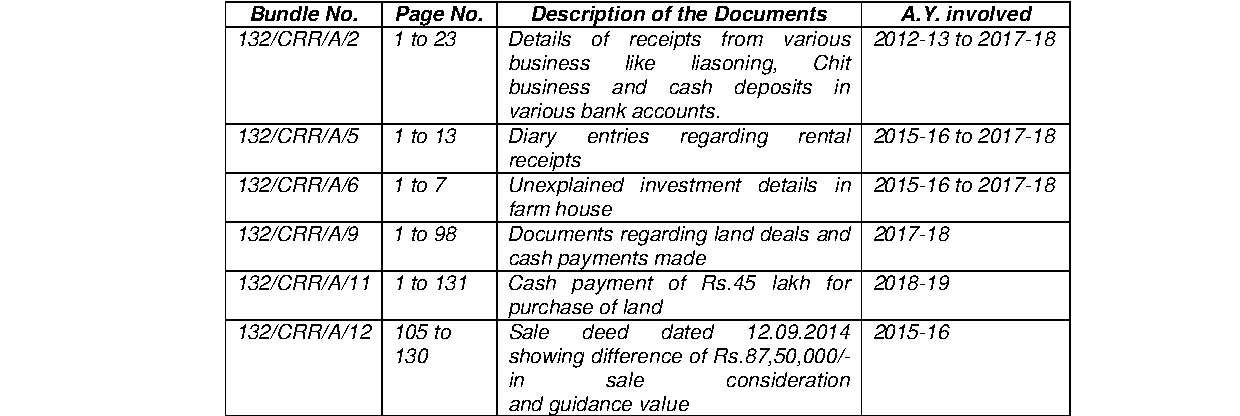

3. A perusal of the material on record will indicate that on12.09.2017, the respondents obtained a warrant of authorization under Section 132 of the I.T.Act and Rule 112 of the I.T.Rules in relation to one K.Narayana Raju and in respect of residential premises of the petitioner at No.24, Lakshmi Nivas, 4th cross Road, K.R.Layout, J.P.Nagar, 6th phase, Bangalore. In pursuance of the same, the respondents conducted a search in the aforesaid premises of the petitioner during the period from 14.09.2017 to 16.09.2017 and recorded the statement of the petitioner, pursuant to which, the respondents prepared a satisfaction note recording reasons for initiating action against the petitioner under Section 153C of the I.T.Act, in pursuance of which, the 1st respondent issued the impugned notices under Section 153C of the I.T.Act to the petitioner which were followed by subsequent notices under Sections 142(1) and 143(2) of the I.T.Act to the petitioner, who is before this Court by way of the present petition.

4. In addition to reiterating the various contentions urged in the petition and referring to the material on record, learned Senior counsel for the petitioner submits that Section 153C of the I.T.Act would not be applicable to the petitioner, inasmuch as the respondents conducted a search of the petitioner at his residential premises in his presence and had recorded his statement, thereby indicating that the petitioner was a “searched person” and not “such other person / non-searched person” within the meaning or scope and ambit of Section 153C of the I.T.Act. It was therefore submitted that the impugned notices issued by the respondents to the petitioner under Section 153C of the I.T.Act are illegal, arbitrary and without jurisdiction or authority of law and contrary to the said provisions and as such, the impugned notices and all further proceedings pursuant thereto, deserve to be quashed. In support of his submissions, learned Senior counsel for the petitioner placed reliance upon the following judgments:-

(i) Deputy Commissioner of Income Tax vs. Sunil Kumar Sharma ; (2024) 168 taxmann.com 77 (SC)

(ii) Deputy Commissioner of Income Tax vs. Sunil Kumar Sharma ; (2024); 159 taxmann.com 179 (Kar.)

(iii) Sunil Kumar Sharma vs. Deputy Commissioner of Income Tax; (2022) 448 ITR 485 (Kar.)

(iv) Commissioner of Income Tax vs. St. Ann’s Education Society in ITA No. 1254/2006 dated 28.09.2011

(v) Commissioner of Income Tax vs. St. Ann’s Education Society in ITA No. 1253/2006 dated 28.09.2011

(vi) St. Ann’s Education Society vs. Deputy Commissioner of Income Tax (Exemptions) in ITA No. 165/Bang/2002 dated 04.04.2006

(vii) C. Ramaiah Reddy vs. Assistant Commissioner of Income Tax; (2011) 339 ITR 210 (Kar.)

(viii) Commissioner of Income Tax vs. IBC Knowledge Park (P.) Ltd.; (2016) 385 ITR 346 (Kar.)

(ix) Commissioner of Income Tax vs. Calcutta Knitwears; (2014) 362 ITR 673 (SC)

(x) Vinit Kumar vs. Central Bureau of Investigation and Ors.; 2019 Scc OnLine Bom 3155

(xi) Manish Maheshwari vs. Assistant Commissioner of Income Tax; [2007] 159 taxmann 258 (SC)

5. Per contra, learned counsel for the respondents – revenue would reiterate the various contentions urged in the

The court held that a petitioner searched under Section 132 of the Income Tax Act cannot be treated as a non-searched person for proceedings under Section 153C, and thus impugned notices issued again....

For invoking Section 153C, the petitioner must not be treated as a non-searched person; proper jurisdiction requires a satisfaction note linking seized documents to undisclosed income of another part....

A person may only be assessed under Section 153C of the Income Tax Act if they are not the 'searched person'; procedural safeguards must precede assessment actions.

The court ruled that assessment orders under Section 153C of the Income Tax Act are void if the petitioner was a searched person and no incriminating evidence was found linking them to potential undi....

The court held that in cases of search under Section 132, the provisions of Section 153A apply mandatorily, overriding Section 147 and 148, unless incriminating material is found.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :