IN THE HIGH COURT OF JUDICATURE AT BOMBAY

M. S. Sonakitendra Jain, JJ

Dilip Gangaram Patil - Appellant

Versus

Additional/joint/deputy Assistant Commissioner Of Income/income Tax Officer, National Faceless Assessment Centre, Delhi - Respondent

WRIT PETITION NO.2771 OF 2022 WITH WRIT PETITION NO.2021 OF 2022

Decided On : 20-02-2025

(A) Income Tax Act, 1961 - Sections 147, 148, and 263 - Challenge to notice issued under Section 148 for reassessment of income for the assessment year 2013-14 - The court held that reopening was impermissible as the original assessment had been set aside under Section 263, and the issues were identical to those previously examined - The reopening was quashed as it was based on change of opinion and lacked fresh material. (Paras 12-18)

(B) Legal Principles - Reopening of assessment beyond four years requires fresh material; reliance on prior proceedings under Section 263 bars reopening on identical issues. (Paras 14-16)

Facts of the case:

The petitioner, engaged in real estate, challenged a notice for reassessment issued after an earlier assessment was set aside under Section 263. The petitioner argued that the reopening was invalid due to lack of fresh material and change of opinion.

Findings of Court:

The court found that the reopening was not justified as the original assessment did not exist at the time of recording reasons, and the issues had already been addressed in prior proceedings.

Issues: Whether the reopening of assessment was valid given the prior proceedings under Section 263 and the lack of fresh material.

Ratio Decidendi: The court ruled that reopening assessments requires fresh material and cannot be based on previously examined issues, reaffirming that reopening beyond four years is subject to strict scrutiny.

Result: Notice under Section 148 quashed.

| Table of Content |

|---|

| 1. challenge to notice under section 148 (Para 2) |

| 2. petitioner engaged in real estate (Para 3) |

| 3. notice under section 263 issued (Para 4) |

| 4. notice under section 148 issued (Para 5 , 6 , 7) |

| 5. reliance on prior proceedings (Para 8 , 9 , 10 , 11) |

| 6. reopening beyond four years (Para 12) |

| 7. original assessment did not exist (Para 13) |

| 8. reopening requires fresh material (Para 14 , 15 , 16 , 17 , 19 , 20) |

| 9. notice under section 148 quashed (Para 18) |

JUDGMENT :

Jitendra Jain, J.

1. Rule. By consent of the parties, since pleadings are completed, taken up for final disposal. By consent of the parties, both the writ petitions are disposed of by common order since the issue involved is identical. We propose to treat Writ Petition No.2771 of 2022 as a lead matter.

2. The petitioner challenges notice dated 25 March 2021 issued under Section 148 of the Income Tax Act, 1961 (‘the Act’) for the assessment year 2013-14.

Brief facts :

3. The petitioner is engaged in the business of real estate and has filed his return of income on 27 September 2013 declaring total income of Rs.54,91,960/-. On 31 December 2015, an assessment order under Section 143(3) of the Act came to be passed accepting the return income.

Proceedings u/s 263 :

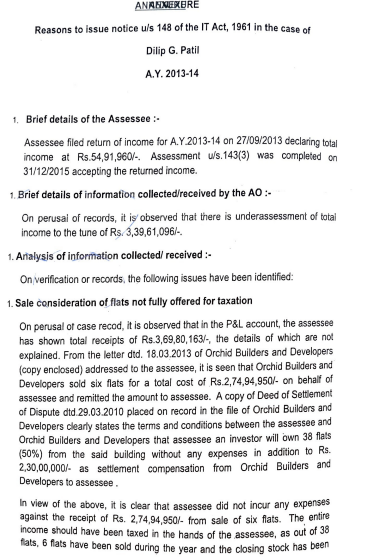

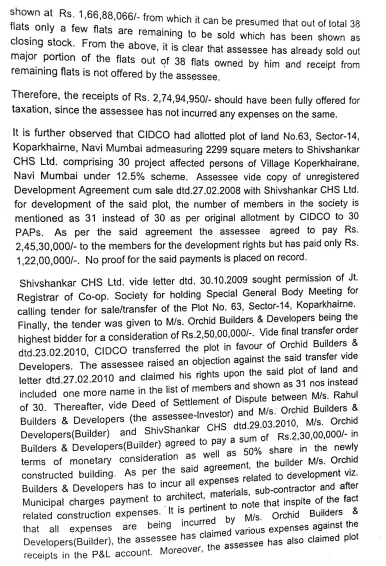

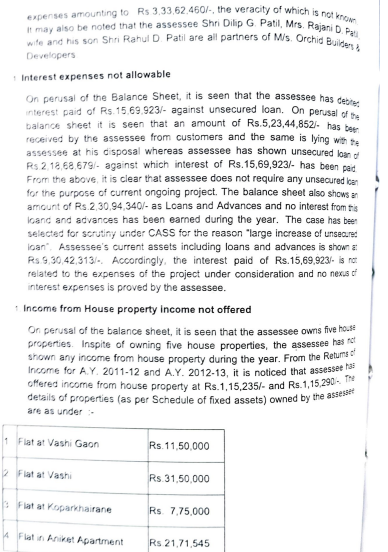

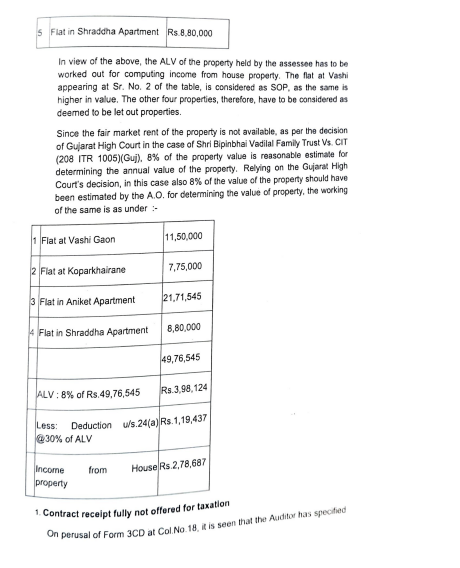

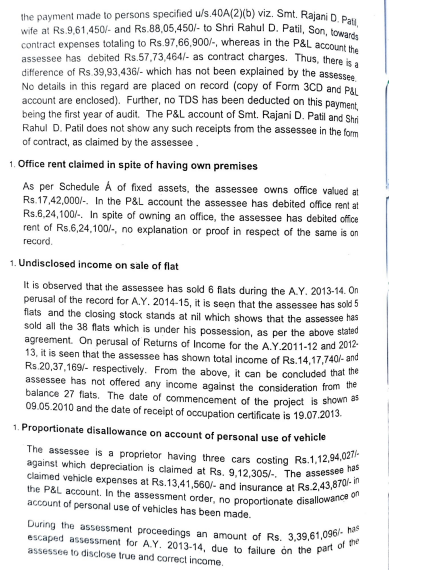

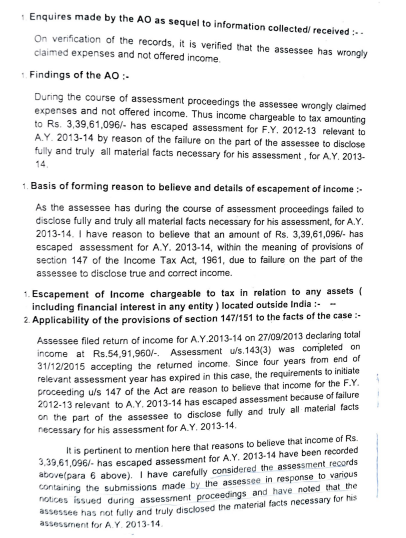

4. On 29 November 2017, a notice under Section 263 of the Act came to be issued by the Commissioner of Income Tax on the ground that M/s. Orchid Builders and Developers has sold 6 flats on behalf of the petitioner for Rs.2,74,94,950/-. However, the same is not reflected in the profit and loss account for the year ending 31 March 2013. The notice further seeks to examine disallowance on account of interest payment and proposes to examine income from house property which was not offered for tax. The petitioner filed his reply to the said show cause notice vide letter dated 1 March 2018. On 16 March 2018, an order under Section 263 was passed by the Commissioner of Income-tax setting aside the assessment order with a direction to conduct proper inquiries, investigation and examine all the issues raised in 263 notice and pass a fresh order. Pursuant to the said direction, Assessing Officer on, 14 December 2018, passed an assessment order under Section 143 (3) read with Section 263 assessing income of the petitioner at Rs.57,06,250/- by making additions on account of notional rent under the head ‘income from house property.’

Proceedings u/s 148 :

5. On 25 March 2021, a notice under Section 148 of the Act was issued to the petitioner calling upon the petitioner to file his return of income for assessment year 2013-14 since the respondents proposed to reassess the income under Section 147 of the Act. The petitioner on 4 January 2022 filed his return of income in compliance with the said impugned notice. On a request being made by the petitioner, the reasons recorded for reopening the case were furnished on 22 March 2021. The petitioner vide letter dated 2 March 2022 objected to the reasons for reopening on the ground that the issue for which the reopening is sought was subject matter of 263 proceedings and, therefore, reopening is bad- in-law. The petitioner also raised objection with respect to there being no failure to disclose fully and truly all material facts and further challenged the sanction obtained from the Commissioner of Income Tax under Section 151 of the Act. On 11 March 2022, an order rejecting the objections came to be passed. In the said order, the reopening was justified on the grounds that, if in the original assessment, the income liable to tax has escaped assessment due to oversight, inadvertence or a mistake committed by the Assessing Officer, the assessment can be reopened on the basis of information obtained from the original assessment. In the said order, reliance was placed on the decision of the Supreme Court in the case of Kalyanji Mavji & Co. Vs. CIT, [(1976) 102 ITR 287 (SC)].

6. It is on the above backdrop that the petitioner is before us challenging the order rejecting the objections dated 11

Reopening of income assessment under Section 148 is impermissible without fresh material and cannot be based on previously examined issues under Section 263.

Reopening of assessment under Section 148 is impermissible if the issues were previously examined under Section 263 without fresh material.

Re-assessment under the Income-tax Act cannot be initiated after four years without specific allegations of failure to disclose material facts necessary for assessment.

Reassessment notices under Section 148 of the Income-tax Act cannot be issued after four years unless there is a failure to disclose material facts, which was not established in this case.

Re-assessment under the Income Tax Act cannot occur after 4 years without specific allegations of non-disclosure of material facts.

Reopening of assessment under Section 148 requires valid reasons; mere incorrect information cannot justify such action.

Reopening of assessment under Section 148 is invalid if based on materials already available during the original assessment, constituting a mere change of opinion without fresh evidence.

The judgment established the importance of tangible material and the prohibition of a mere change of opinion in the exercise of power under section 147 of the Income Tax Act.

Reopening of assessment beyond four years without fresh tangible material or proper disposal of objections is illegal under the Income Tax Act.

Reopening of assessment under Section 148 is valid based on audit objections if the taxpayer fails to provide timely responses or necessary documentation.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :