HIGH COURT OF BOMBAY

M.S. SONAK, JITENDRA SHANTILAL JAIN

ICICI BANK LTD - Appellant

Versus

Deputy Commissioner of Income Tax- - Respondent

WP/1172/2022

Decided On : 11-02-2025

(A) Income-tax Act, 1961 - Section 147 and Section 148 - Re-assessment proceedings - Notice issued after 4 years from the end of the assessment year - No allegation of failure to disclose material facts - Impugned notice quashed as it amounted to change of opinion and lacked necessary allegations. (Paras 5, 7, 11, 12)

(B) Legal principles - Re-assessment cannot be initiated after 4 years unless there is a failure to disclose material facts - The reasons for re-opening must specify undisclosed material facts. (Paras 7, 11)

Facts of the case:

The petitioner challenged a notice under Section 148 issued for the assessment year 2014-15, arguing it was barred by the first proviso to Section 147 due to the absence of allegations of non-disclosure of material facts.

Findings of Court:

The court found no allegations of failure to disclose material facts in the reasons recorded for re-opening, thus quashing the notice.

Issues: The main issues were whether the notice was valid given the time elapsed and the absence of allegations of non-disclosure of material facts.

Ratio Decidendi: The court ruled that re-assessment proceedings cannot be initiated after 4 years without allegations of non-disclosure of material facts, and the reasons recorded must specify such facts.

Result: Rule made absolute, notice quashed.

JUDGMENT :

(Jitendra Jain, J.) :

1. Heard learned counsel for the parties.

2. Rule. Rule is made returnable immediately at the request of and with the consent of learned counsel for the parties.

3. This petition challenges notice under Section 148 of the Income-tax Act, 1961 (hereinafter referred to as ‘the Act’) issued by the respondent No.1 for the assessment year 2014-15.

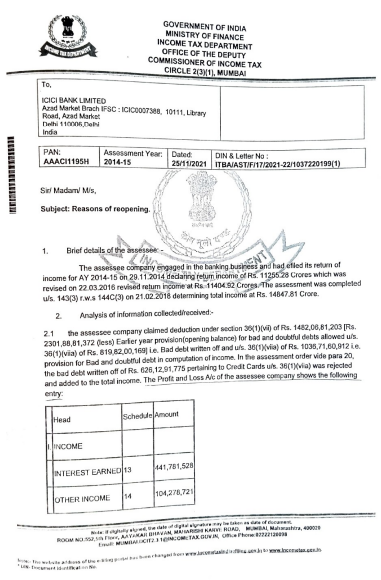

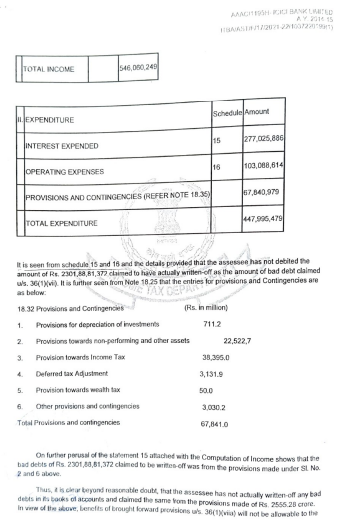

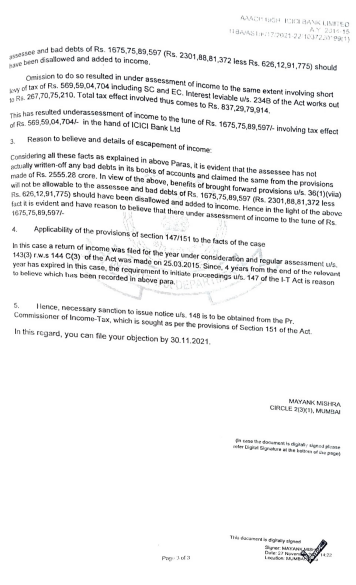

4. The reasons for re-opening were furnished to the petitioner on 25 November 2011 and the same reads as under :-

5. Ms. Vissanji, learned counsel for the petitioner submits that the impugned notice is issued after a period of 4 years from the end of the relevant assessment year and in the absence of any allegation of any failure to disclose fully and truly all material facts necessary for the assessment, impugned notice is barred by the first proviso to Section 147 of the Act. She further submits that the issue for which the re- opening is sought was raised in the course of the assessment proceedings and a reply was filed by the petitioner and same was considered in the assessment order. Therefore, based on this ground also the impugned proceedings would amount to change of opinion. She relied upon the decision in the case of Hindustan Unilever Limited Vs R.B. Wadkar, (2004) 268 ITR 332and decision of the co-ordinate bench of this Court in the petitioner’s own case in Writ Petition No.3108 of 2022 dated 31 October 2022 in support of her submission and prayed that the impugned notice be quashed. She further submits that all the details were furnished alongwith the return of income in the assessment proceeding and the same is evident from the reasons recorded itself.

6. Mr. Mishra learned counsel for the respondent defends the impugned proceedings and submits that the petitioner has mis- represented in so far as the issue of deduction under Section 36(1)(vii) is concerned. He therefore submits that there is a failure on the part of the petitioner to disclose fully and truly all material facts and therefore the proceedings are valid and same is not hit by the first proviso of Section 147 of the Act.

7. We have heard learned counsel for the petitioner and respondent and perused the documents brought to our attention. There is no dispute that the notice under Section 148 is issued after the expiry of period of 4 years from the end of the relevant assessment order. As per the first proviso of Section 147 of the Act, re-assessment proceedings cannot be initiated after period of 4 years from the end of the relevant assessment year unless there is a failure on the part of the assessee to disclose fully and truly all material facts necessary for the assessment. The co-ordinate bench of this Court in the case of Hindustan Unilever Limited (Supra) has held that there has to be not only the allegation that there is a failure on the part of the assessee to disclose fully and truly all material facts but the reasons should also state what are the material facts which were not disclosed. On a perusal of the reasons recorded in the present case, we do not find any allegation of any failure to disclosure fully and truly of material facts necessary in the assessment. But on the contrary on a perusal of the reasons recorded, it shows that the information on the basis of which re-opening is sought was based on the documents filed by the petitioner alongwith the return of income and in the assessment proceeding. Therefore, on this short ground itself the impugned proceedings are required to be quashed and set aside.

8. The learned counsel for the petitioner is justified in relying upon the decision in its own case in Writ Petition No.3108 of 2022 where on very similar ground the notice under Section 148 of the Act was quashed.

9. In any case the assessing officer in the course of the assessment proceedings had raised a query vide letter dated 1 July 2016 which reads as under:

Please give details of rural advances --- Please give details of claims of deduction towards advances given by ru

Re-assessment under the Income-tax Act cannot be initiated after four years without specific allegations of failure to disclose material facts necessary for assessment.

Re-assessment under the Income Tax Act cannot occur after 4 years without specific allegations of non-disclosure of material facts.

Reopening of assessment under Section 148 is impermissible if the issues were previously examined under Section 263 without fresh material.

Reopening of income assessment under Section 148 is impermissible without fresh material and cannot be based on previously examined issues under Section 263.

Reassessment notices under Section 148 of the Income-tax Act cannot be issued after four years unless there is a failure to disclose material facts, which was not established in this case.

Reassessment cannot be based on a change of opinion, and the duty of the assessee is to disclose fully and truly all primary relevant facts.

Re-opening of assessment under Section 148 requires failure to disclose material facts; absence of such allegation invalidates the notice.

Reopening of assessment under Section 148 requires valid reasons; mere incorrect information cannot justify such action.

A notice under Section 148 of the Income Tax Act is invalid if issued beyond the limitation period and based on previously available information, constituting a change of opinion.

The judgment established the importance of tangible material and the prohibition of a mere change of opinion in the exercise of power under section 147 of the Income Tax Act.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :