IN THE HIGH COURT OF JUDICATURE AT BOMBAY

M.S. SONAK, JITENDRA JAIN, JJ.

Prithvi Apartments Co-operative Housing Society Limited - Appellant

Versus

The Assistant Commissioner of Income Tax - Respondent

Writ Petition No. 3086 of 2022

Decided On : 21-04-2025

(A) Income Tax Act, 1961 - Sections 147, 148, and 143(3) - Notice for re-opening assessment - Notice dated 31.03.2021 challenged for assessment year 2014-15 - No failure to disclose material facts alleged - Re-opening based on change of opinion not permissible - Notice quashed. (Paras 6, 9)

(B) Re-opening of assessment - Precondition for re-opening after four years is failure to disclose material facts - No such allegation found in the reasons recorded. (Paras 6, 9)

Facts of the case:

The Petition challenges a notice under Section 148 for the assessment year 2014-15, issued after four years from the end of the relevant assessment year, following an assessment order under Section 143(3) dated 07.12.2016.

Findings of Court:

The notice under Section 148 was quashed as there was no allegation of failure to disclose material facts and the issues had already been examined during the original assessment proceedings.

Issues: The main issues were whether the precondition for re-opening the assessment was satisfied and whether the notice constituted a change of opinion.

Ratio Decidendi: The court held that the absence of an allegation of failure to disclose material facts and the examination of the issues during the original assessment proceedings rendered the re-opening notice invalid.

Result: Notice quashed and set aside.

JUDGMENT :

JITENDRA JAIN, J.

1. Heard learned Counsel for the parties.

2. Rule. Rule is made returnable forthwith. By consent, the Petition is taken up for final hearing, since the pleadings in this case are completed.

3. This Petition challenges notice under Section 148 of the Act dated 31.03.2021 for the assessment year 2014-15.

4. In this case, an assessment order under Section 143(3) of the Act was passed on 07.12.2016. The impugned notice under Section 148 is dated 31.03.2021 i. e. after a period of four years from the end of the relevant assessment year.

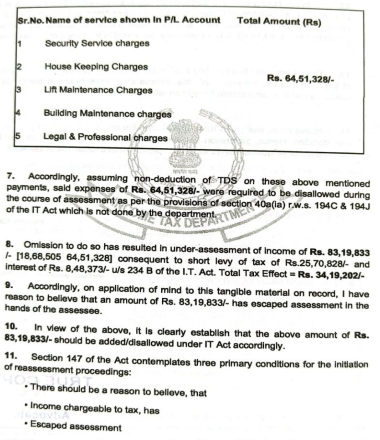

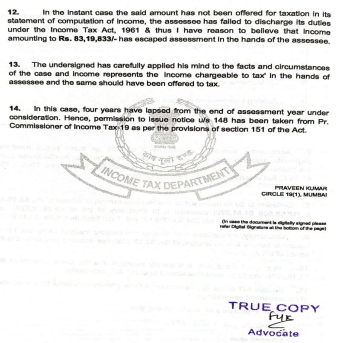

5. The reasons recorded for re-opening the concluded assessment which were furnished to the Petitioner on 18.11.2021 read as under :-

6. The precondition as per first proviso to Section 147 of the Act for re-opening the case, where an assessment order under Section 143(3) is passed and the case is to be re-opened after a period of four years is that there has to be failure to disclose fully and truly all material facts necessary for the assessment.

7. On a perusal of the reasons recorded which are reproduced above, there is no allegation of any failure on the part of the assessee to disclose fully and truly all material facts necessary for the assessment. Even on a perusal of the reasons recorded, the said pre-condition cannot be discerned with even in the absence of such allegation. Paragraph Nos. 2 to 6 categorically admit that the reasons are based on verification of the profit and loss account and the other relevant records. If that be so, we fail to understand how the pre-condition specified in first proviso to Section 147 of the Act is satisfied. Therefore, on this short ground itself, the re-opening notice under Section 148 dated 31.03.2021 for assessment year 2014 -15 is required to be quashed and set aside.

8. Even otherwise, the issue of eligibility of interest under Section 80P was a subject matter of investigation in the course of the regular assessment proceedings and same is evident from paragraph 3 of the original assessment order, wherein the issue of deduction under Section 80P is discussed. Insofar as the issue of disallowance under Section 40(a)(ia) is concerned, a query was raised by the Respondents in the course of the assessment proceedings vide notice dated 18.07.2016 and same was replied by the assessee vide letter dated 09.11.2016, wherein all the details with respect to the TDS were furnished. The details are also filed along with this Petition from page 125 to 135. Therefore, on both these grounds i. e. deduction under Section 80P and disallowance for non-deduction of TDS, the issue was examined during the course of the assessment proceedings and therefore, any attempt to re-open the case on these two issues would amount to re-opening on the basis of change of opinion and review of the earlier order passed under Section 143(3) of the Act. This is not permissible under the Act which confers the power to re-open the case under Section 147 of the Act.

9. In view of above, on both the grounds i. e. there being no allegation of failure to disclose fully and truly all material facts necessary for the assessment and the issues having examined during the course of the original assessment proceedings, the impugned notice under Section 148 of the Act dated 31.03.2021 seeking to re-open concluded assessment of assessment year2014-15 is quashed and set aside.

10. Rule is made absolute in the above terms.

11. Accordingly, the Petition stands disposed of.

Re-opening of assessment under Section 148 requires failure to disclose material facts; absence of such allegation invalidates the notice.

Re-assessment under the Income-tax Act cannot be initiated after four years without specific allegations of failure to disclose material facts necessary for assessment.

Reassessment notices under Section 148 of the Income-tax Act cannot be issued after four years unless there is a failure to disclose material facts, which was not established in this case.

Re-assessment under the Income Tax Act cannot occur after 4 years without specific allegations of non-disclosure of material facts.

Reopening of income assessment under Section 148 is impermissible without fresh material and cannot be based on previously examined issues under Section 263.

Reopening of assessment under Section 148 is impermissible if the issues were previously examined under Section 263 without fresh material.

The court emphasized the requirement for the AO to have a valid 'reason to believe' that income has escaped assessment due to failure to disclose fully and truly all material facts necessary for asse....

The power to reopen assessments under Section 147 of the IT Act is much wider post-1st April, 1989, but must be based on tangible material and have a live link with the formation of belief.

Reopening of assessment under the Income Tax Act requires tangible new material; mere change of opinion is insufficient.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :