THE GAUHATI HIGH COURT (HIGH COURT OF ASSAM, NAGALAND, MIZORAM AND ARUNACHAL PRADESH) KOHIMA BENCH

DEVASHIS BARUAH, J.

Mr. Thekrubizolie And Anr. - Petitioners

Versus

The Union Of India Represented By The Secretary To The Govt. Of India Ministry Of Finance Dept. Of Revenue And Ors. - Respondents

WP(C)/129 of 2024, WP(C)/130 of 2024

Decided On : 23-03-2026

| Table of Content |

|---|

| 1. factual and procedural background regarding two writ petitions challenging gst assessment orders. (Para 1 , 2 , 3 , 4 , 5 , 6 , 7 , 8 , 9 , 10 , 11 , 12 , 13 , 14 , 15 , 16 , 17) |

| 2. parties' contentions on validity of show cause notices and statutory compliance under ngst act. (Para 18 , 19 , 20 , 21 , 22 , 23 , 24 , 25 , 26) |

| 3. invalidity of assessment orders due to lack of jurisdictional foundation and absence of hearing. (Para 27 , 28 , 29 , 30 , 31 , 32 , 33 , 34) |

| 4. quashing of impugned orders with liberty to initiate fresh, legally compliant proceedings. (Para 35) |

ORDER :

DEVASHIS BARUAH, J.

Heard Ms. Arati Agarwal, learned counsel appearing on behalf of the Petitioner. Mr. Z. Kulnu, learned CGC appears on behalf of the Respondent No. 1/Union of India and Mr. Veto V. Zhimomi, learned Government Advocate appears on behalf of the Respondent Nos. 2 and 3, i.e. GST Authorities of the State of Nagaland.

2. The Respondent No. 4 is not represented when the matter is taken up

3. The issues involved in both the writ petitions being the same, they are taken up for disposal by this common Judgment and Order. However, for the sake of convenience and clarity in passing the directions, this Court finds it relevant to take note of the brief facts which led to the filing of both the writ petitions.

WP(C)/129/2024

4. The Petitioner No. 1 herein is the Proprietor of a Firm in the name and style of M/S Dimapur Diesels. The said Firm, namely M/S Dimapur Diesels is registered under the Central Goods & Services Tax Act, 2017 (for short ‘CGST’) and have been allocated a Registration No. being GSTIN13ABUPA6964C2ZO. The present writ petition so filed challenges the Order dated 18.07.2023, passed by the Respondent No. 3 under Section 74 (9) of the Nagaland Goods & Services Tax Act, 2017 (for short ‘NGST’).

5. The materials on record shows that the Petitioner No. 2 herein was issued a Notice in DRC01-A dated 14.11.2022 wherein the determined tax interest and penalty for the periods 2019-2020, 2020-2021 and 2021-2022 were mentioned.

6. The Petitioner No. 2upon receipt of the said Notice sought for time for complying with the same. Thereupon, the Respondent No. 2 issued another Notice under DRC01-A for the Financial Years 2019-2020, 2020- 2021 and 2021-2022. It is, however, pertinent to mention that a perusal of these Notices which were issued under DRC01-A categorically mention that these Notices were issued in the context of Section 74 of the NGST Act. The said aspect of the matter is further clear from the Notice itself wherein it is stated that non-compliance with the said Notice would attract Notice under Section 74 (1) of the NGST Act. The Petitioner, on 24.05.2023 submitted a Reply.

7. Be that as it may, it is alleged by the Petitioner No. 2 that as the Respondents indulged in coercive steps the Petitioner No. 2 under compelling circumstances had made certain payment under protest and uploaded the same under DRC03 on 27.06.2023.

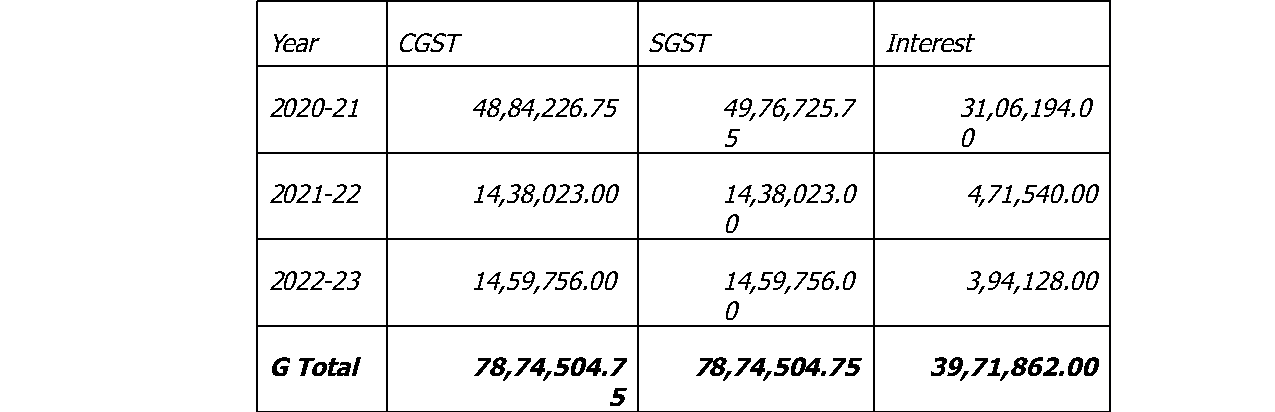

8. On 28.06.2023, the Respondent No. 1 issued a Show Cause Notice under Section 74 (1)&(7) thereby intimating the Petitioner No. 1 that for the period 2019-2020, 2020-2021, 2021-2022 and 2022-2023 the Petitioner had paid only the penalty portion of 15% amounting to Rs. 12,11,020/- (Rupees twelve lakhs eleven thousand and twenty) for the period 2019-2020, Rs. 68,95,004/- (Rupees sixty eight lakhs ninety five thousand and four) for the period 2020-2021, Rs. 4,31,406/- (Rupees four lakhs thirty one thousand four hundred and six) for the period from 2021- 2022 and Rs. 4,37,926/- (Rupees four lakhs thirty seven thousand nine hundred and twenty six) for the period 2022-2023. The Petitioner No. 1 was asked to show cause as to why the Payment Notice in DRC07 should not be issued to the Petitioner for the remaining amount of tax and interest as detailed therein.

9. It appears that the Petitioner did not file a Reply to the said Show Cause and this resulted in passing of an Order on 18.07.2023 wherein it was mentioned

Show cause notices must explicitly allege fraud or wilful misstatements under Section 74 of the Act to proceed legally; absence of such allegations renders orders invalid.

A Summary of Show Cause Notice cannot replace a proper Show Cause Notice, and failure to provide a hearing violates natural justice principles.

A summary of a show cause notice in electronic form cannot substitute the requirement for a formal show cause notice under the tax legislation. Issuance of a proper notice is a mandatory condition pr....

Show-cause notices under Sections 73 and 74 of the WBGST/CGST Act can coexist for the same tax period if based on distinct grounds, and petitioners must pursue available appellate remedies before see....

The main legal point established in the judgment is the mandatory and imperative nature of the show cause notice requirement under Section 74(1) of the JGST Act and the need for specific charges in t....

Proceedings under Section 74 of the CGST Act cannot be initiated without evidence of fraud or misstatement if prior proceedings under Section 73 have been concluded.

A proper Show Cause Notice is essential for valid proceedings under Section 73 of the Assam Goods and Services Tax Act, ensuring compliance with principles of natural justice.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :