IN THE HIGH COURT OF JUDICATURE FOR RAJASTHAN AT JODHPUR

MUNNURI LAXMAN, PUSHPENDRA SINGH BHATI, JJ.

M/s Multani Tools Company, Loharpura, Nagaur - Petitioner

Versus

Union Of India, through the Secretary to the Government of India, Ministry of Finance, Department of Revenue and Anr. - Respondents

D.B. Civil Writ Petition No. 4552 Of 2002

Decided On : 17-12-2024

(A) Income Tax Act, 1961 - Section 148 - Writ petition challenging reassessment proceedings - Petitioner contended that no incriminating material was found during the survey to justify reopening assessments for prior years - The court held that the loose paper indicating undervalued sales provided sufficient grounds for reassessment, and the limitation period was not exceeded as the escaped income exceeded the threshold. (Paras 1, 3, 14, 17)

(B) Reassessment - Validity - The court emphasized that the existence of a valid reason to believe that income had escaped assessment is crucial for proceeding under Section 148, and the petitioner was allowed to present evidence to counter the findings. (Paras 8, 18)

JUDGMENT :

(Munnuri Laxman, J.)

1) The present writ petition has been filed with the following prayers:-

(ii) Hold that the reasons recorded u/s 148 as communicated vide impugned letter dated 26.8.2002 (Annexure-2) are illegal and cannot be sustained in the eyes of the law.

(iii) Restrain the respondents from taking further proceedings in pursuance of the impugned notices u/s 148 (Annexure-1).

(iv) Hold that the initiation of reassessment proceedings for all the assessment years in question, in the case of the petitioner is illegal and/or without jurisdiction.

(v) Any other appropriate relief/reliefs as may be considered just and necessary by the Hon’ble Court in the facts and circumstances of the case to do complete justice to the petitioner.

(vi) The cost of the writ petition may be kindly awarded”

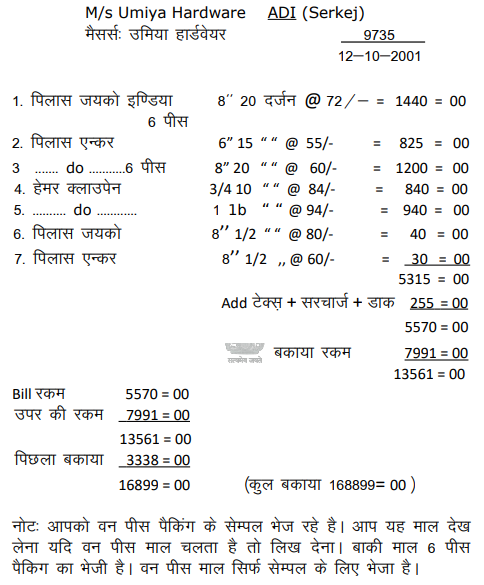

2) The petitioner is a partnership firm and it is a regular assessee with the Income Tax Department. A survey was conducted in the business premises of the petitioner under Section 133 of the Income Tax Act, 1961 (hereinafter referred to as, “the Act”) on 16.10.2001. During the course of survey, nothing incriminating material was found, except a loose paper bearing No.60 (which is filed as Annexure-I/9). The statement of the assessee was recorded under Section 131 of the Act on 24.10.2001 relating to the loose paper, which was recovered in the said search. Hindi version of the said statement reads as follows:

^^iz'u %& losZ{k.k ds nkSjku vki dh QeZ esa eqYrkuh VwYl d- dh fcØh ds fcy QkbZy esa fcy la[;k 9735 fnukad 12&10&2002 ds lkFk ,d ywt isij yxk gqvk feyk gS ftlds Annexure I/9 ist 60 ds vuqlkj mijksDr fcy dh jkf'k e; lsYl VSDl bR;knh ds 5570@& crkbZ x;h gS vkSj blds vykok 7991@& dh jkf'k mij dh jde n'kkZ;h x;h gS vkSj bl izdkj bl fcy dh dqy jkf'k 13561@& crkbZ x;h gS ,oe fiNyk cdk;k : 3338@& tksM dj dqy cdk;k 16899@& crk;k x;k gS bl ywt isij dk /;ku ls ns[kus ij izrhr gksrk gS fd fcy dh jde 5570@& vkSj mij dh jde 7991@& dqy jde Øe'k% 41 izfr'kr o 59 izfr'kr vkrh gS vkSj bl izdkj fcØh dks v.Mj fcfyax fd;k x;k gS d`i;k Li"V djsa fd vki dh nksuksa QeksZa dh dqy fcØh dks 60 izfr'kr ls v.Mj fcfyax eku dj D;ksa ugha v/kksf"kr fcØh ekuh tk;@vkSj bl izdkj dh iw.kZ jde dks vki dh vk; eS tksMh tkosA

mrj %& fcy ua- 9735 fnukad 12&10&2001 ds dh dksih ls bl fcy dh jkf'k : 5670@& : feyrh gSA rFkk fiNyk cdk;k : 3338@& fcy la- 9729 fnukad 26&9&2001 dh cdk;k jkf'k gSA blds vykok bl ikVhZ dks lsEiy ds fy, eky vi:oZy ds fy, Hkstk Fkk ftldk fcy ugha curk gS rFkk eky dh vi:oZy vkus ds ckn gh fcy cuk;k tkrk gSA : 7991@& dk lUnHkZ bl vi:oy ij Hksts eky dh vuqekfur dher dk gSA pwafd vi:oy vk;s fcuk eky dh fcØh ugha ekuh tkrh gSA vr% bls v/kksf"kr fcØh u ekuus dh d`ik djsaA^^

The translated English version of the said statement reads as follows:

Answer- From the copy of Bill No. 9735 dated 12-10-2001, the amount of this bill is Rs. 5570/- and the previous outstanding amount of Rs. 3338/- is the real outstanding amount of Bil

The court upheld the validity of reassessment proceedings under Section 148 based on found incriminating material, emphasizing the importance of valid grounds for reopening assessments.

Reopening of assessment under Section 148 is invalid if based on materials already available during the original assessment, constituting a mere change of opinion without fresh evidence.

A reassessment notice must be based on specific and valid information suggesting income has escaped assessment, and changing the basis for reassessment mid-proceeding is impermissible under the Incom....

Consistency in the reasons provided to the assessee and those existing on the record is crucial in reassessment proceedings under Section 148 of the Income Tax Act, 1961.

Under section 147 of the Act the proceedings for the reassessment can be initiated only if the Assessing Officer has reason to believe that any income chargeable to tax has escaped assessment for any....

The court established that under the amended Section 148A of the Income Tax Act, the requirement to record 'reason to believe' has been replaced with a subjective decision-making process, allowing fo....

Point of Law : Sufficiency of the evidence or material is not open to scrutiny by the Court but the existence of the belief is the sine qua non for a valid exercise of power.

Reassessment under Income Tax Act is impermissible on issues already addressed in a completed assessment, as it constitutes a change of opinion without new material evidence.

The 'reason to believe' for reassessment must be based on tangible material with a direct nexus to the formation of the belief, and reassessment cannot be made on a change of opinion.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :