BEFORE THE MADURAI BENCH OF MADRAS HIGH COURT

C.Saravanan, J.

M/s.Devi Traders, Represented by its Proprietor - Petitioner

Versus

The State Tax Officer (Inspection) 5, - Respondent

W.P.(MD) Nos.22371, 22372, 22933, 23473, 23474, 23475, 23927, 23928, 23929, 22955, 22956, 22935, 22934, 22957, 23489, 23490, 23491, 23476, 23477 and 23478 of 2023 and W.M.P.(MD) Nos.18649, 18650, 20100, 20101, 20103, 20102, 19161, 19163, 19176, 19178, 19180, 19691, 19692, 19694, 19681, 19685, 19684, 19682, 19683 and 19687 of 2023

Decided On : 24-01-2025

| Table of Content |

|---|

| 1. identification of writ petitions and challenged orders. (Para 1) |

| 2. evidence pertaining to statements and assessments. (Para 2 , 3) |

| 3. claims of denial of cross-examination and taxation principles. (Para 4 , 5 , 6 , 7) |

| 4. burden of proof and implications of tax credit. (Para 8 , 9 , 10 , 11 , 12 , 13) |

| 5. overview of legal arguments presented. (Para 14) |

| 6. details surrounding previous litigation outcomes. (Para 15 , 16 , 17 , 18 , 19) |

| 7. analysis of issued summons and their outcomes. (Para 20 , 21 , 22 , 23) |

| 8. tax liability and eligibility for tax credit. (Para 24 , 25 , 26 , 27 , 28) |

| 9. conditions required to avail input tax credit. (Para 29 , 30 , 31 , 32) |

| 10. obligatory documents for proving tax claims. (Para 33 , 34 , 35 , 36) |

| 11. generated e-way bill regulations. (Para 37 , 38 , 39 , 40) |

| 12. provisions regarding verification and compliance. (Para 41 , 42 , 43 , 44 , 45) |

| 13. regulations of e-way bill generation and its necessity. (Para 46 , 47 , 48 , 49) |

| 14. exemptions regarding e-way bill requirements. (Para 50 , 51 , 52) |

| 15. rules for carrying documents during goods transport. (Para 53 , 54) |

| 16. maintenance of accounts and documentation mandates. (Para 55 , 56 , 57 , 58) |

| 17. implications of insufficient documentation on credit claims. (Para 59 , 60 , 61 , 62) |

| 18. impact of non-allowance of cross-examination. (Para 63 , 64 , 65) |

| 19. confirmed decisions on recipient's burden of proof. (Para 66 , 67 , 68) |

| 20. final observations on the case outcome. (Para 69) |

| 21. court's final order and directions. (Para 70 , 71) |

ORDER :

C.Saravanan, J.

In these Writ Petitions, the respective petitioners have challenged the Impugned Assessment Orders passed on the dates mentioned below pursuant to Remand Orders passed by this Court in the earlier round of litigations. The details of the Writ Petitions filed by the respective petitioners are as under:-

| Sl. No | W.P.(MD) No. | Petitioner | Assessment Year | Date of Impugned Order | Tax * (In Rs.) | Penalty * (In Rs.) | Interest (In Rs.) |

| 1 | 22371/23 | Devi Traders | 2017-18 | 25.5.23 | 8179930 | 8179930 | - |

| 2 | 22372/23 | Devi Traders | 2018-19 | 25.5.23 | 136906 | 136906 | - |

| 3 | 22933/23 | Thapasi Rubbers | 2017-18 | 24.5.23 | 2035004 | 1017502 | - |

| 4 | 22934/23 | Thapasi Rubbers | 2018-19 | 24.5.23 | 3906326 | 1953163 | - |

| 5 | 22935/23 | Thapasi Rubbers | 2019-20 | 24.5.23 | 561126 | 280564 | - |

| 6 | 22955/23 | J.K.Global Traders | 2017-18 | 2.12.22 | 649750 | 649750 | - |

| 7 | 22956/23 | J.K.Global Traders | 2018-19 | 2.12.22 | 267000 | 267000 | - |

| 8 | 22957/23 | J.K.Global Traders | 2019-20 | 30.12.22 | 1257212 | 1257212 | - |

| 9 | 23473/23 | Alban Rubbers | 2017-18 | 10.5.23 | 12895762 | 12895762 | 12451179 |

| 10 | 23474/23 | Alban Rubbers | 2018-19 | 10.5.23 | 16669208 | 16669208 | 13498209 |

| 11 | 23475/23 | Alban Rubbers | 2019-20 | 10.5.23 | 6427918 | 6427918 | 4168042 |

| 12 | 23476/23 | Sree Maruthi Traders | 2017-18 | 31.5.23 | 2753654 | 2779596 | - |

| 13 | 23477/23 | Sree Maruthi Traders | 2018-19 | 31.5.23 | 5957218 | 5957218 | - |

| 14 | 23478/23 | Sree Maruthi Traders | 2019-20 | 31.5.23 | 2129226 | 2129226 | - |

| 15 | 23489/23 | Baby Trading Company | 2017-18 | 10.5.23 | 167114 | 167114 | 154122 |

| 16 | 23490/23 | Baby Trading Company | 2018-19 | 10.5.23 | 485236 | 485236 | 361796 |

| 17 | 23491/23 | Baby Trading Company | 2019-20 | 10.5.23 | 5143140 | 5143140 | 3401584 |

| 18 | 23927/23 | D.Y.Beathel Enterprises | 2017-18 | 13.9.22 | 605142 | 605142 | - |

| 19 | 23928/23 | D.Y.Beathel Enterprises | 2018-19 | 13.9.22 | 927280 | 927280 | - |

| 20 | 23929/23 | D.Y.Beathel Enterprises | 2019-20 | 13.9.22 | 343674 | 343674 | - |

* CGST + SGST

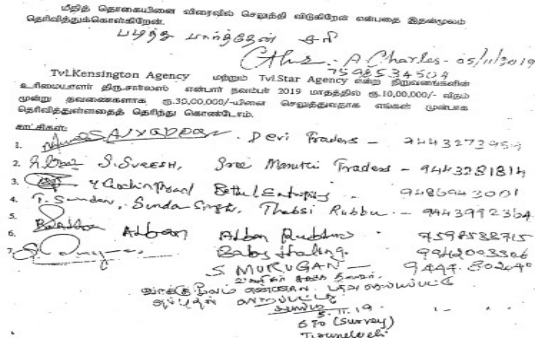

2. Pursuant to statement obtained from one Charles, the Proprietor of Tvl.Kensington Agency and Star Agency on 05.11.2019, the said supplier had undertaken to pay a sum of Rs.30,00,000/- on the dates mentioned therein. The said statement of Charles, Proprietor of Tvl.Kensington Agency reads as under:-

The above statement was recorded in the presence of the respective petitioners.

3. It is also noticed that the following orders have been passed against Tvl.Kensington Agency and Tvl.Vajra Agency of the husband and wife namely, Charles and Shanthi, for the following Assessment Years.

| Name | Assessment Year | Date | Amount (In Rs.) |

| Tvl.Kensington Agency | 2017-2018 | 27.10.2020 | 2,61,39,880 |

| 2018-2019 | 28.10.2020 | 2,53,76,534 | |

| Tvl.Vajra Agency | 2018-2019 | 28.10.2020 | 1,80,75,068 |

| 2019-2020 | 28.10.2020 | 1,07,70,740 |

4. The common ground of attack in these Writ Petitions is that the petitioners ha

The burden of proof lies on the recipient to establish the legitimacy of Input Tax Credit claims, necessitating evidence of actual goods received, which failed in this case.

Dealers claiming input tax credit must establish genuine transactions and physical movement of goods with adequate proof; failure to do so may result in disallowance and recovery proceedings under th....

A registered person is not entitled to input tax credit if the claimed supplies are from non-existent firms, regardless of the validity of the supplier's GST registration at the time of transaction.

Input Tax Credit requires valid documentation proving the physical movement of goods; the burden of proof lies with the assessee to substantiate claims, and penalties are subject to careful assessmen....

Denial of CENVAT credit based on third-party statements without granting the assessee an opportunity to cross-examine the witnesses constitutes a violation of the principles of natural justice, neces....

The taxpayer must substantiate claims for input tax credit with adequate proof of genuine transactions; failure to do so justifies the cancellation of GST registration.

Tax authorities must provide substantial evidence of fraud or suppression of facts before imposing penalties under Sections 74 and 50, especially when input tax credit has already been reversed volun....

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :