IN THE HIGH COURT OF JUDICATURE AT MADRAS

C.SARAVANAN, J.

Ms.Kandan Hardware Mart, Represented by its Proprietor E.P – Petitioner

Versus

The Assistant Commissioner (ST) (FAC) – Respondent

W.P.Nos.27029, 27032, 27036, 32599, 19967, 34352, 34357, 35186 of 2023, W.P.Nos.3540, 3567, 3570, 3572, 3902, 15690, 3915, 3916, 3966, 23356, 30854, 9867 of 2024 and W.P.Nos.9988, 28786, 38007, 42416, 46522, 47726 and 48941 of 2025 and W.M.P.Nos.26455, 26457, 26460, 26461,26469, 26471, 26473, 32182, 32183, 19319, 19321, 34255, 34256, 34257, 34258, 34263, 34264, 34265, 34266, 35170, 35173 of 2023, 3802, 3803, 3827, 3829, 3833, 3836, 3842, 3844, 4228, 4229, 10881, 10882, 10883, 17098, 17099, 4232, 4236, 4233, 4234, 4282, 4285, 25514, 33447 of 2024 and 11195, 32261, 42437, 42440, 47431, 47437, 47439, 51901, 51902, 53274, 53275, 54670 and 54673 of 2025

Decided On : 02-01-2026

| Table of Content |

|---|

| 1. factual background of writ petitions filed (Para 1 , 2 , 3 , 4 , 5 , 6) |

| 2. court observations on various penalties and fees (Para 14 , 18 , 20 , 23 , 86 , 127) |

| 3. petitioners argue against penalties and late fees imposed (Para 17 , 24 , 30 , 31 , 36 , 39) |

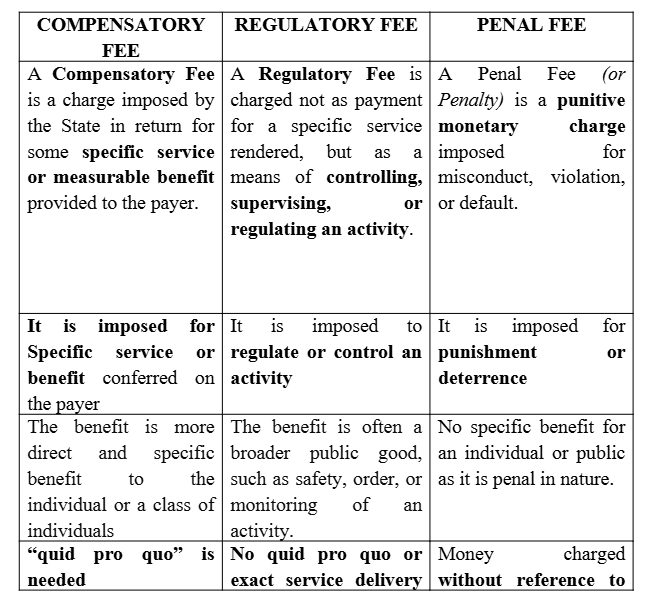

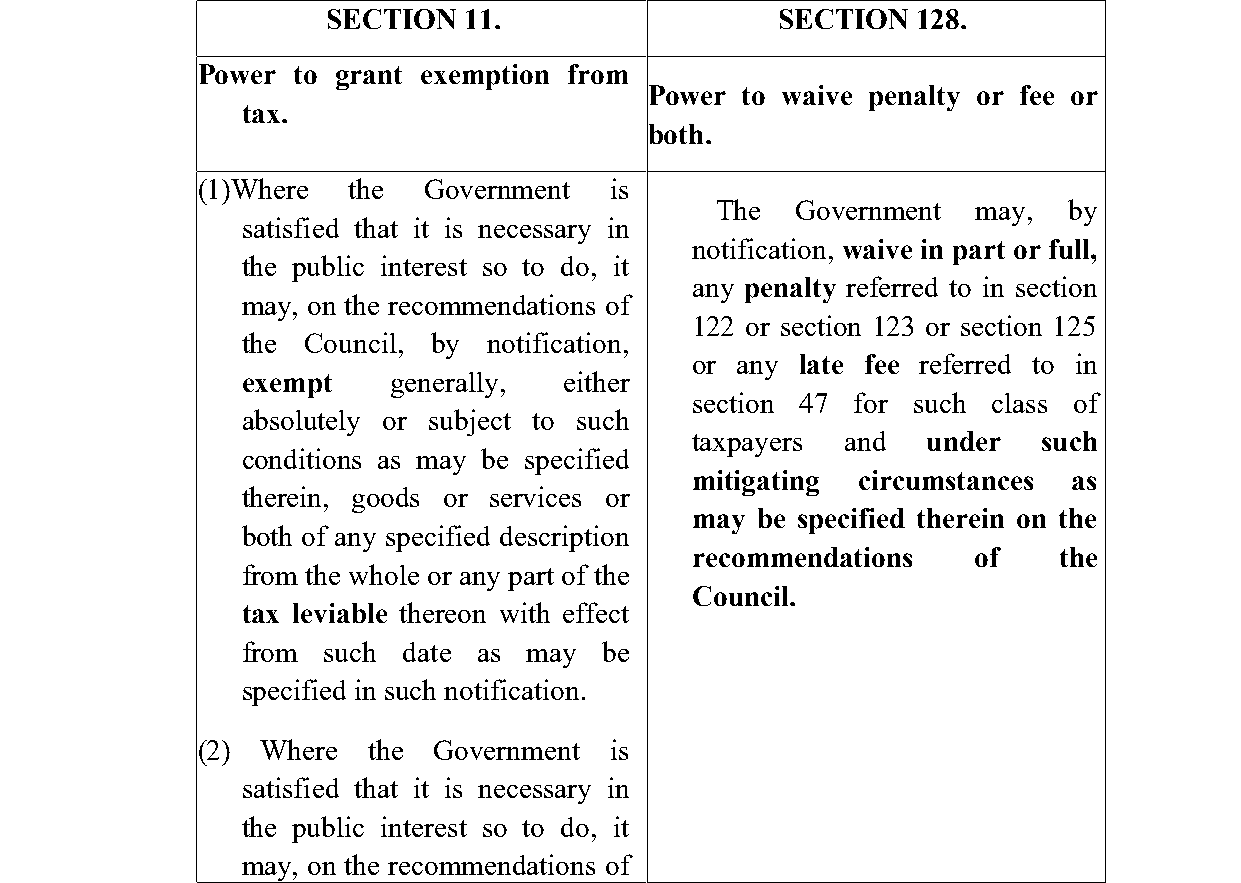

| 4. distinction between penalties and fees discussed (Para 37 , 57 , 63 , 124 , 150 , 174) |

| 5. final order on late fees and penalties (Para 199 , 210 , 212) |

ORDER :

C.SARAVANAN, J.

By this Common Order, all these Writ Petitions are being disposed of.

2. In these Writ Petitions, the respective Petitioners have challenged the levy of “Late Fee” under Section 47 of the respective GST Enactments and / or “Penalty” under Section 125 of the respective GST Enactments or both.

3. The details of the impugned Assessment Orders and Show Cause Notices impugned in these Writ Petitions are as follows:-

Table-1

| Sl. No. | W.P.No. | Tax Period | Show Cause Notice (DRC-01) | Impugned Order |

|---|---|---|---|---|

| 1 | 27029 of 2023 | 2017-2018 | 11.02.2022 | 26.12.2022 (Penalty) |

| 14.02.2023 | 12.05.2023 (Late Fee) | |||

| 2 | 34352 of 2023 | 2017-2018 | 10.12.2022 | 08.02.2023 |

| 3 | 15690 of 2024 | 2017-2018 | 30.08.2023 | 30.12.2023 |

| 4 | 23356 of 2024 | 2017-2018 | 20.01.2023 | 18.03.2024 |

| 5 | 30854 of 2024 | 2017-2018 | 14.02.2023 | 03.11.2023 |

| 6 | 46522 of 2025 | 2017-2018 | 29.09.2023 | 29.12.2023 |

| 7 | 47726 of 2025 | 2017-2018 | 24.03.2023 | 30.12.2023 |

| 8 | 27032 of 2023 | 2018-2019 | 02.11.2022 | 26.12.2022 |

| 9 | 3540 of 2024 | 2018-2019 | 25.01.2023 | 13.01.2024 |

| 10 | 3567 of 2024 | 2018-2019 | 25.01.2023 | 13.01.2024 |

| 11 | 3570 of 2024 | 2018-2019 | 25.01.2023 | 13.01.2024 |

| 12 | 3572 of 2024 | 2018-2019 | 25.01.2023 | 13.01.2024 |

| 13 | 3902 of 2024 | 2018-2019 | 25.01.2023 | 13.01.2024 |

| 14 | 3916 of 2024 | 2018-2019 | 25.01.2023 | 13.01.2024 |

| 15 | 3966 of 2024 | 2018-2019 | 25.01.2023 | 13.01.2024 |

| 16 | 9867 of 2024 | 2018-2019 | 28.03.2022 | 28.02.2023 |

| 2019-2020 | 28.03.2022 | 28.02.2023 | ||

| 17 | 27036 of 2023 | 2019-2020 | 08.11.2022 | 27.12.2022 |

| 18 | 32599 of 2023 | 2019-2020 | 02.01.2023 | 09.06.2023 |

| 19 | 19967 of 2023 | 2019-2020 | 19.01.2023 | 18.05.2023 |

| 20 | 34357 of 2023 | 2019-2020 | 10.12.2022 | 08.02.2023 |

| 21 | 35186 of 2023 | 2019-2020 | 08.11.2022 | 28.02.2023 |

| 22 | 9988 of 2025 | 2019-2020 | 27.04.2023 | 30.08.2024 |

| 23 | 28786 of 2025 | 2019-2020 | 27.02.2024 | 29.03.2025 |

| 24 | 38007 of 2025 | 2019-2020 | 27.05.2024 | 29.08.2024 |

| 25 | 42416 of 2025 | 2019-2020 | 11.05.2024 | 17.08.2024 |

| 26 | 48941 of 2025 | 2019-2020 | 22.11.2022 | 28.12.2022 |

| 27 | 3915 of 2024 | 2020-2021 | 09.12.2022 | 22.01.2024 |

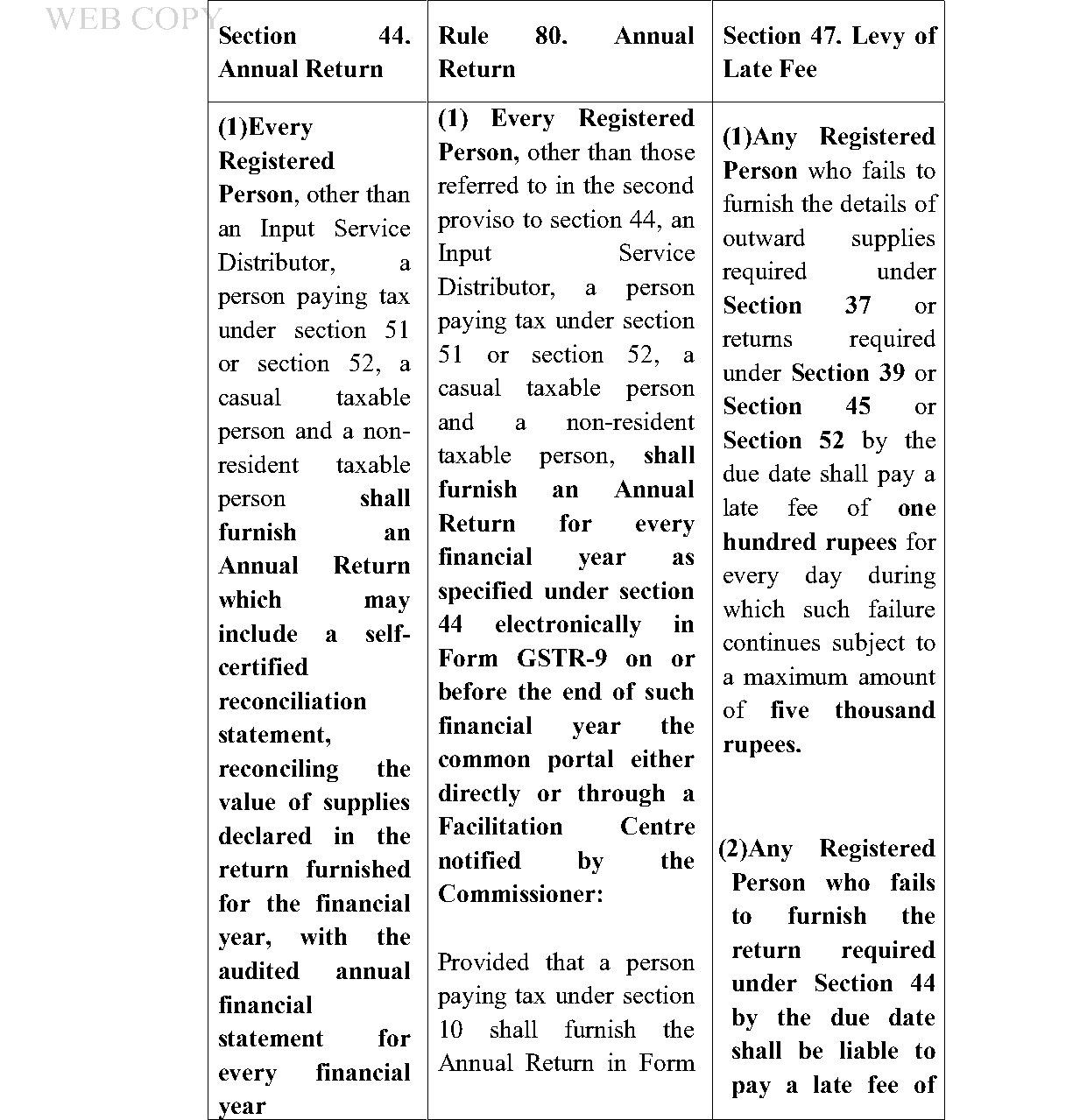

4. As per Section 47 (1) of the respective GST Enactments, a Registered Person who fails to furnish the details of outward supplies as is contemplated under Section 37 of the said Enactment i.e. GSTR-1 or returns required under Section 39 i.e. GSTR-3B or under Section 45 i.e., GSTR-10 or under Section 52 i.e., GSTR-8 of the said Enactment by the "due date", they are bound to pay a “Late Fee” of Rs.100/- for every date during which such failure continues subject to a maximum of Rs.5,000/-.

5. Under Section 47 (2) of the respective GST Enactments, a Registered Person who fails to furnish the "Annual Return" in GSTR-9 required under Section 44 by the "due date", is liable to pay a “Late Fee” of One Hundred Rupees (Rs.100/-) for every day during which such failure continues subject to a maximum of an amount calculated at a quarter percent of the turnover in the State or the Union Territory.

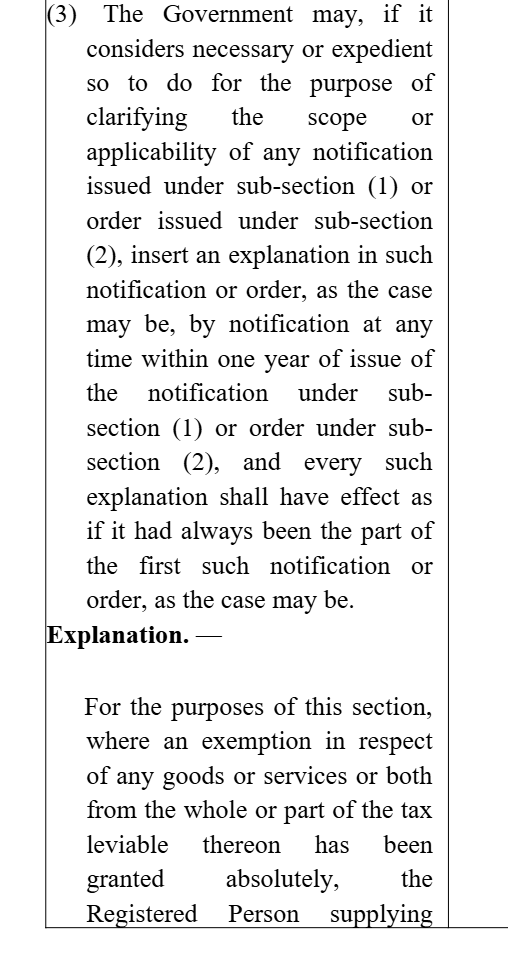

6. The “due date” for filing "Annual Return" in GSTR-9 is prescribed under Rule 80 of the respective GST Rules. For the sake of clarity, Rule 80 of the respective GST Rules which are pari-materia to each other is reproduced below:-

80. Annual return. –

(1) Every registered person, other than those referred to in the second proviso to section 44, an Input Service Distributor, a person paying tax under section 51 or section 52, a casual taxable person and a non-resident taxable person, shall furnish an annual return for every financial year as specified under section 44 electronically in Form GSTR-9 on or before the end of such financial year the common portal either directly or through a Facilitation Centre notified by the Commissioner:Provided that a person paying tax under section 10 shall furnish the annual return in Form GSTR-9-A.

(1-A) Notwithstanding anything contained in sub-rule (1), for the financial year 2020-202

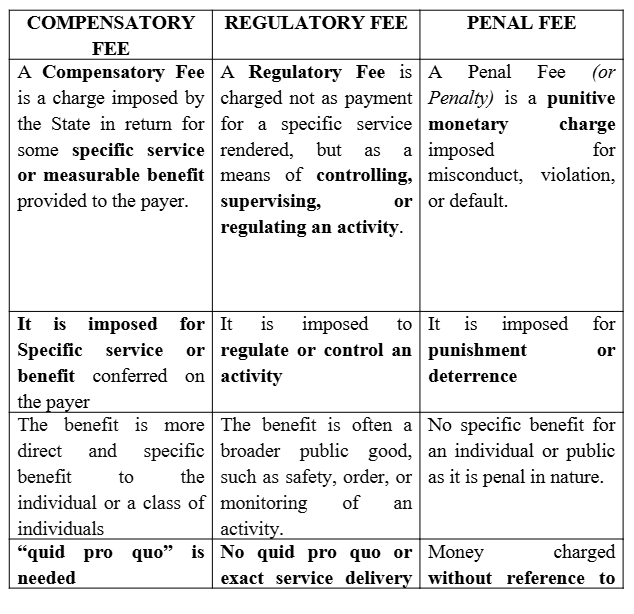

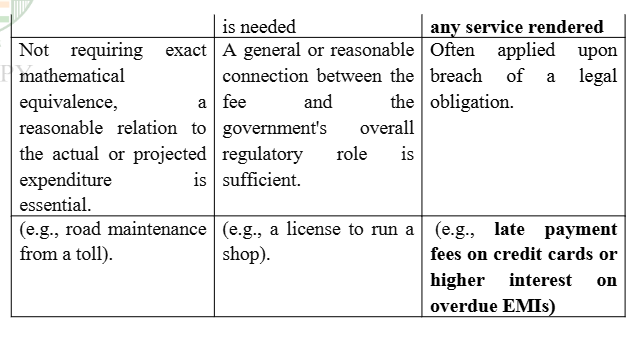

The court ruled that imposing both Late Fees and General Penalties for GST return delays is improper; Late Fee suffices under applicable rules, reflecting legislative intent for compliance, not punit....

Interest and penalty cannot be levied on late payment of duty that is exempted under the Central Excise Act, as no liability arises for such payments.

The Central Government is empowered under Section 211 of the Motor Vehicles Act to levy additional fees for delayed applications related to driving licenses and vehicle registrations, which are not p....

The court established that the imposition of delay fees by circular without statutory authority contradicts the principles of law, rendering such fees arbitrary and illegal.

No enabling provision under S.200A for levying S.234E late fees on TDS returns prior to 01.06.2015 amendment.

The notification issued by the State Government u/s 78 of the Registration Act, prescribing the registration fee on a graduated form on the basis of value of subject matter of the instrument is in ac....

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :