IN THE HIGH COURT OF JUDICATURE AT MADRAS

C. SARAVANAN, J.

M/s. Exemplarr Worldwide Limited – Appellant

Versus

The Central Board of Direct Taxes, Rep. by its Chairperson, New Delhi – Respondent

W.P. No. 15322 of 2023, W.M.P. Nos. 14824, 14826 of 2023

Decided On : 20-04-2026

| Table of Content |

|---|

| 1. factual background of inter-corporate loan and prior assessment (Para 1 , 2 , 3 , 4 , 5 , 6 , 8) |

| 2. parties' contentions on jurisdiction and limitation (Para 7 , 9 , 10 , 11) |

| 3. ashish agarwal directions on old regime notices (Para 12 , 13 , 14 , 15 , 16) |

| 4. rajeev bansal clarification on tola applicability (Para 17 , 18 , 19 , 20 , 21) |

| 5. section 148a(d) timeline and exclusions (Para 22 , 23 , 24 , 25 , 26 , 27 , 28) |

| 6. limitation analysis under new regime provisos (Para 29 , 30 , 31 , 32 , 33) |

| 7. covid-19 extension of limitation periods (Para 34 , 35 , 36 , 37) |

| 8. timely issuance of 148a(d) order and 148 notice (Para 38 , 39 , 40 , 41 , 42) |

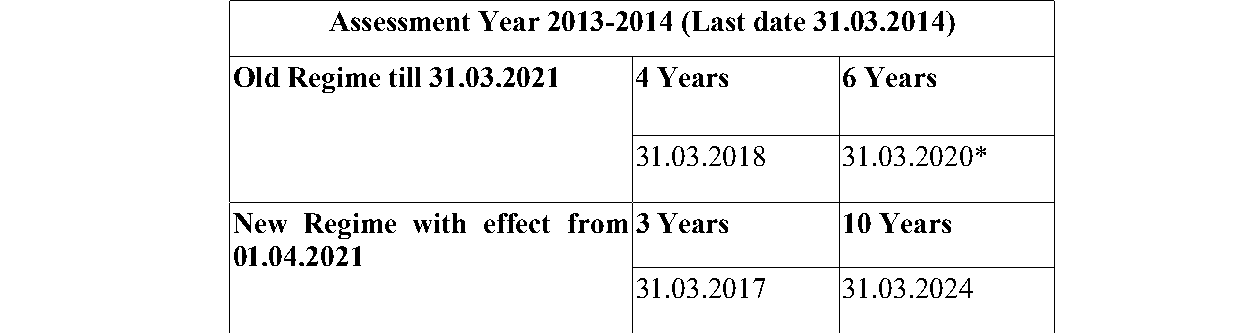

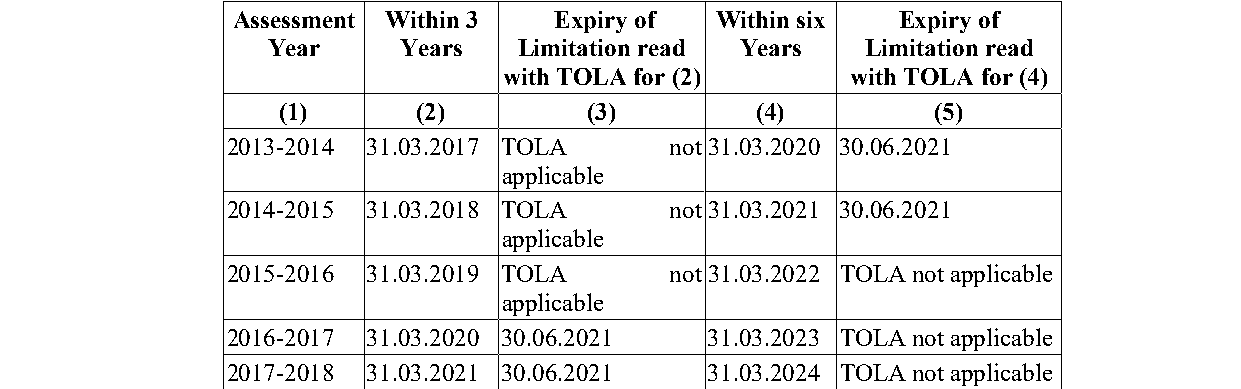

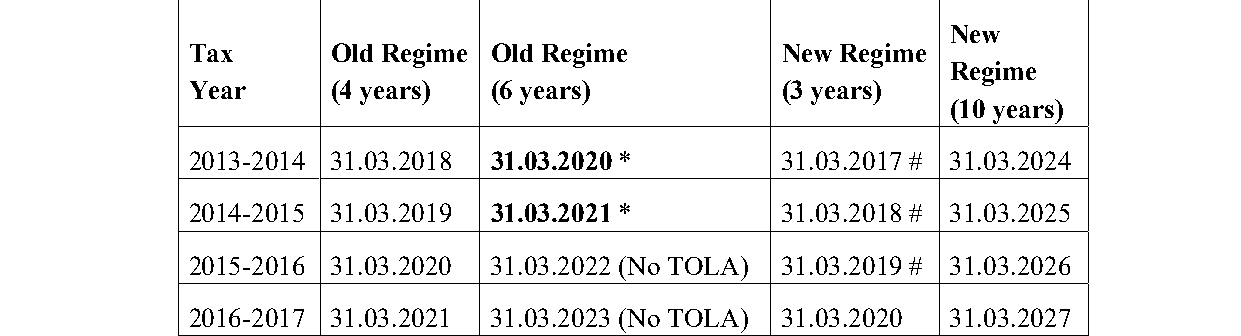

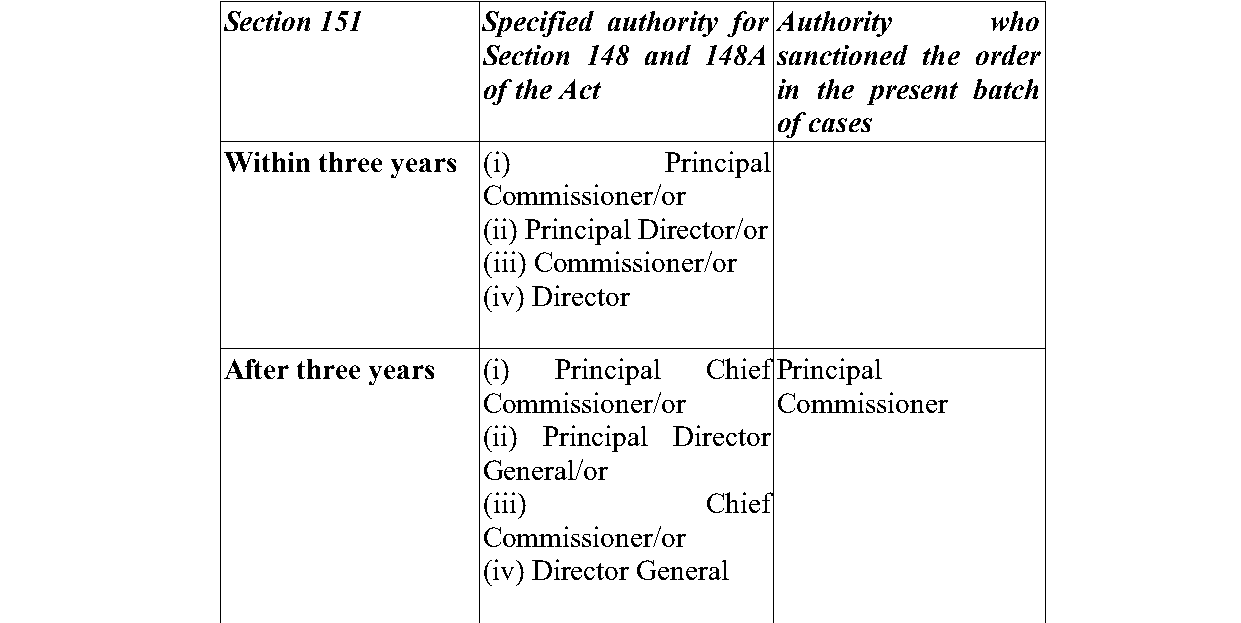

| 9. valid approval by specified authority under section 151 (Para 43 , 44 , 45 , 46 , 47 , 48) |

| 10. writ petition dismissed with appeal liberty (Para 49 , 50 , 51 , 52) |

ORDER :

1. In this Writ Petition, the Petitioner has challenged the impugned Section 148 Notice dated 30.07.2022 of the Income Tax Act, 1961 (hereinafter referred to as Act), which has culminated in the impugned Assessment Order dated 31.03.2023 passed by the 2nd Respondent under Section 147 read with Section 143(3) of the on the ground that they are without jurisdiction.

2. The case of the Petitioner is that the statutory approval required under Section 151 the Act ought to have been obtained from the Principal Chief Commissioner and not from the Director General under the new regime as in force from 01.04.2021. According to the Petitioner, the Return of Income originally filed culminated in an Assessment Order dated 31.03.2016 under Section 143(3) of the Act against which Appeal is pending before the Appellate Forum.

3. Dispute in the present case relates to an inter-corporate loan for a sum of Rs.10,18,80,000/- received by the Petitioner from M/s. Ananya Infrastructure Pvt. Ltd. It is submitted that the said inter-corporate loan was also reflected in the books of accounts. It is submitted that the explanation offered by the Petitioner was accepted in the said Assessment Order dated 31.03.2016.

4. It is stated that the Petitioner had furnished ledger extracts, bank statements, confirmation letters, PAN details, and financial statements of the creditor of Petitioner Company to establish the identity, genuineness, and creditworthiness of the lender. According to the Petitioner, once such materials were furnished, the burden stood discharged and it was for the Department to establish that the amount represented undisclosed income in the hands of the Petitioner.

5. The Petitioner further contends that though a statement was recorded from one of the Directors regarding the lending company, such person was not directly in charge of its affairs, and therefore any inability on his part to furnish further particulars could not be a ground to draw an adverse inference that income had escaped assessment for the Assessment Year 2013-2014. It is also submitted that the transactions were routed through regular banking channels, and both entities are corporate assesses who regularly file Returns of Income and statutory records.

6. In this case proceedings for reopening the assessment were initiated by issuance of Section 148 Notice dated 30.06.2021, followed by A (b) Notice dated 02.06.2022 after the Hon’ble Supreme Court rendered its decision in Union of India and others Vs. Ashish Agarwal, 2022 SCC Online SC 543 vide Order dated 04.05.2022, to which the Petitioner submitted a Reply dated 13.07.2022 under A (c) of the Act. Thereafter, the impugned Order dated 30.07.2022 came to be passed under A (d) of the Act and a consequential Notice also dated 30.07.2022 which has culminated in the impugned Assessment Order dated 31.03.2023.

7. The learned counsel for the Petitioner submitted that the issue relating to the receipt of Rs.10,18,80,000/- from M/s.Ananya Infrastructure Pvt. Ltd. had already been examined in the original assessment proceedings completed under Section 143(3) of the Act on 31.03.2016, and the explanation furnished by th

Reassessment notice for AY 2013-14 upheld as timely under new regime, with exclusions for TOLA, Covid periods, and Section 148A reply time; Director General's approval valid under Section 151(ii).

Reassessment notice under Section 148 issued after Section 148A(b) on last day of old regime limitation held valid as response time excluded under Section 149 proviso; book entries qualify as 'assets....

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :