IN THE HIGH COURT OF JUDICATURE AT MADRAS

C. Saravanan, J.

Ravi Constructions - Petitioner

Versus

The Assistant Commissioner of Income Tax Central Circle -3 - Respondent

W.P.No.11606 of 2023 and W.M.P.Nos.11511, 11512 & 11513 of 2023

Decided On : 23-02-2026

ORDER :

C. Saravanan, J.

In this Writ Petition, the petitioner has challenged the impugned order dated 28.04.2022 passed under Section 148A(d) of the Income Tax Act, 1961 (hereinafter referred to as the ‘Act’) and the consequential Notice dated 28.04.2022 issued under Section 148 of the Act under the new regime as in force with effect from 01.04.2021 for the Assessment Year 2015-2016.

2. The petitioner had filed its Return of Income on30.09.2015 for the Assessment Year 2015-2016 admitting a total income of Rs.22,83,270/-. The said Return of Income was processed under Section 143(1) of the Act on 01.12.2015.

3. The Petitioner was thereafter issued with a Notice dated 31.03.2022 under Section 148A(b) of the Act under the new regime as in force with effect from 01.04.2021. The said notice ultimately culminated in the impugned Section 148A(d) order dated 28.04.2022 and the consequential Section 148 Notice dated 28.04.2022

4. Meanwhile, the Hon’ble Supreme Court delivered its verdict in Union of India Vs. Ashish Agarwal., (2024) SCC Online SC 2693 on 04.05.2022, which was later further clarified by the Hon’ble Supreme Court in Union of India Vs. Rajeev Bansal, 2024 SCC Online SC 2993. I shall refer to the same in due course.

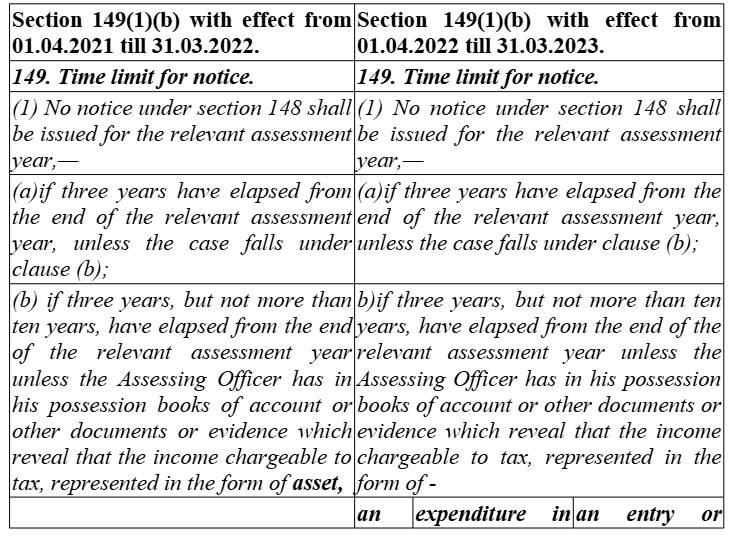

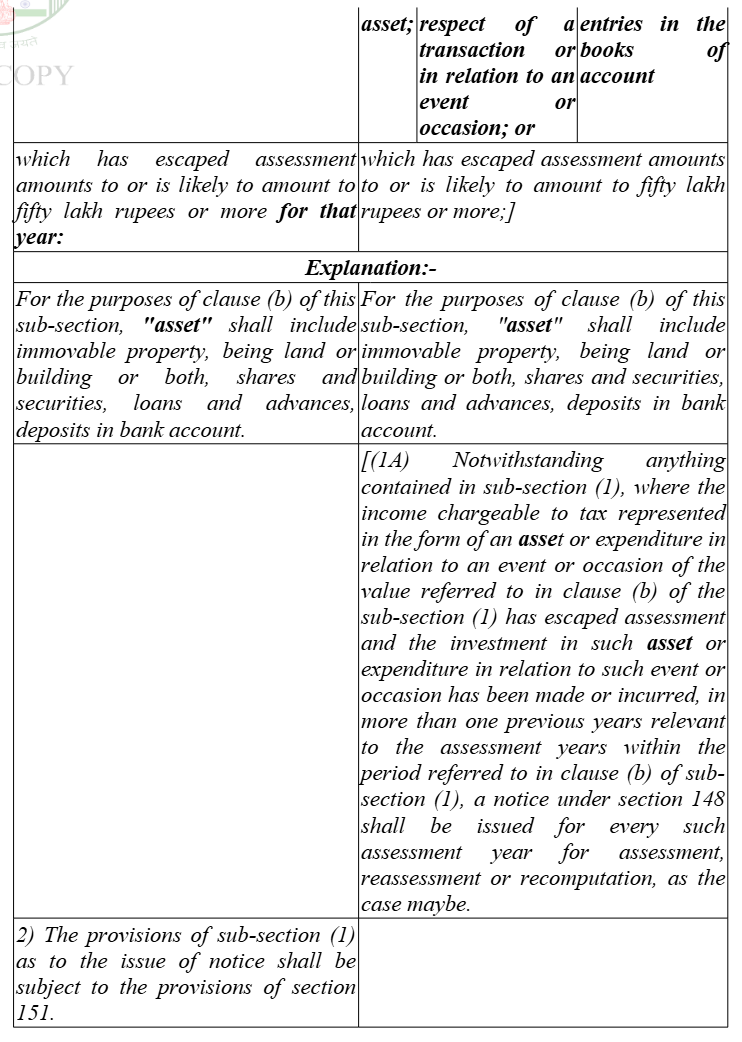

5. The challenge to the impugned order dated 28.04.2022 passed under Section 148A(d) of Act and the consequential Section 148 Notice dated 28.04.2022 is primarily on the ground that the limitation for issuance of Section 148 Notice. According to the Petitioner, the limitation had already expired on 31.03.2022 under the old regime and therefore in terms of 1st proviso to Section 149(1) of the Act as in force with effect from 01.04.2021 and therefore the reassessment proceedings were without jurisdiction.

6. That apart, it is submitted by the learned counsel for the petitioner that the Notice dated 31.03.2022 issued under Section 148A(b) of the Act under the new regime as in force with effect from 01.04.2021 was issued based on a survey conducted from 12.02.2021 under Section 133A of the Act.

7. It is therefore submitted by the learned counsel for the petitioner that the last date for issuance of Section 148 Notice expired on 31.03.2022 for the Assessment Year 2015-2016

8. It is therefore submitted that the initiation of reassessment proceedings by issuing a Notice dated 31.03.2022 under Section 148A(b) of the Act under the new regime as in force with effect from 01.04.2021 itself is barred by limitation.

9. The learned counsel for the petitioner has strongly placed reliance on the concession given on behalf of the Department by the Additional Solicitor General of India before the Hon’ble Supreme Court in in para 19(f) in Union of India Vs. Rajeev Bansalreferred to supra

10. For the sake of convenience, para19 from the said decision referred to supra is extracted below:-

“19. Mr. N Venkataraman, learned Additional Solicitor General of India, made the following submissions on behalf of the Revenue:

a. Parliament enacted TOLA as a free-standing legislation to provide relief and relaxation to both the assesses and the Revenue during the time of COVID-19. TOLA seeks to relax actions and proceedings that could not be completed or complied with within the original time limits specified under the Income-tax Act;

b. Section 149 of the new regime provides three crucial benefits to the assesses: (i) the four-year time limit for all situations has been reduced to three years; (ii) the first proviso to Section 149 ensures that re-assessment for previous assessment years cannot be undertaken beyond six years; and (iii) the monetary threshold of Rupees fifty lakhs will apply to the re assessment for previous assessment years;

c. The relaxations provided under section 3(1) of TOLA apply "notwithstanding anything contained in the specified Act." Section3(1), therefore, overrides the time limits for issuing a notice under Section 148 read with Section149 of the Income-tax Act;

d. TOLA does not extend the life of the old regime. It merely provide

Reassessment notice under Section 148 issued after Section 148A(b) on last day of old regime limitation held valid as response time excluded under Section 149 proviso; book entries qualify as 'assets....

The notices under the amended Income Tax Act are valid even if previously invalid notices existed, provided conditions of procedural compliance and limitation exclusions are met.

Reassessment notice u/s.148 for AY 2017-18 issued after 3 years with escaped income below Rs.50 lakhs held barred by limitation under first proviso to section 149(1)(b), quashing proceedings.

Reassessment notice for AY 2013-14 upheld as timely under new regime, with exclusions for TOLA, Covid periods, and Section 148A reply time; Director General's approval valid under Section 151(ii).

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :