IN THE HIGH COURT OF ALLAHABAD

KSHITIJ SHAILENDRA, J.

Deepesh Agarwal and Another – Petitioners

Versus

State of U.P. and Another – Respondents

Civil Misc. Writ Petition No. 38110 of 2017

Decided On : 11-05-2023

Stamp Duty - Agricultural Land Purchase - Indian Stamp Act, 1899 - Sections 33, 47-A - The court emphasized the necessity of adhering to the initial deficiency notice and the principles of natural justice, quashing excessive demands and remanding for proper assessment.

Fact of the Case:

The petitioners purchased agricultural land and were later informed of a deficiency in stamp duty. The Collector imposed a higher deficiency and penalty, which the petitioners challenged, leading to a series of legal proceedings.

Finding of the Court:

The court found that the authorities exceeded their mandate by imposing a deficiency beyond the initial notice and violated principles of natural justice, necessitating a remand for proper assessment.

Issues: Whether the authorities could impose a stamp duty deficiency beyond the amount specified in the initial notice and whether the subsequent notice was valid.

Ratio Decidendi: The court held that the authorities could not determine a deficiency greater than that specified in the show-cause notice, and any subsequent notice issued was contrary to prior court directions and barred by limitation.

Result: The impugned order was quashed, and the matter was remanded for a fresh determination of stamp duty deficiency.

JUDGMENT :

KSHITIJ SHAILENDRA, J.

1. Heard Shri Swapnil Kumar, learned counsel for the petitioners and learned Standing Counsel for the State-respondents.

2. An agricultural piece of land was purchased by the petitioners alongwith others by registered sale-deed dated 13.7.2005. A reference was made by the Sub-Registrar immediately after two days, i.e. on 15.7.2005 mentioning that deficient stamp duty has been paid by the petitioners considering the location of the land transferred and, after making calculations, the Sub Registrar made following request to the Collector:

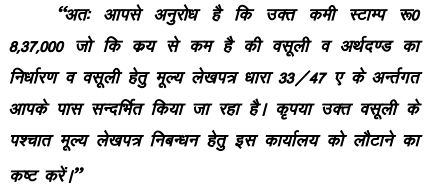

3. Therefore, the deficiency, which was worked out at the time of initiation of proceedings under the Indian Stamp Act, 1899 was Rs. 8,37,000/- (rupees eight lac thirty seven thousand).

4. The stamp case was registered against the petitioners being Case No. 137 of 2009, in which an order was passed by the Collector, Mahamaya Nagar on 24.12.2009 working out deficiency in payment of stamp duty to the tune of Rs. 30,11,160/- (rupees thirty lac eleven thousand one hundred sixty) alongwith penalty of Rs. 6,02,232/- (rupees six lac two thousand two hundred thirty two) total demand being Rs. 36,13,392/- (rupees thirty six lac thirteen thousand three hundred ninety two) alongwith interest at the rate of 1.5% per month from the date of execution of the instrument.

5. The petitioners challenged the aforesaid order before the revisional Court and in compliance of the statutory requirements of making 1/3rd deposit, the petitioners deposited a sum of Rs. 11,17,000/- (rupees eleven lac seventeen thousand) before the revisional Court and, consequently, the impugned order dated 24.12.2009 was stayed.

6. Thereafter, the revision was dismissed by the order dated 20.4.2011, against which the petitioners alongwith other purchasers of the aforesaid sale-deed, filed Writ C No. 30971 of 2011 (Mohan Kumar Varshney and others v. State of U.P. and others), in which an interim order was passed on 25.5.2011 taking into consideration that a sum of over Rs. 11,17,000/- (rupees eleven lac seventeen thousand) had already been deposited by the petitioners and, therefore, the operation of the order impugned dated 24.12.2009 passed by Collector, Mahamaya Nagar in Case No. 137 of 2009 (State v. Smt. Vinesh Gutpa and others), as well as order dated 20.4.2011 passed by the Chief Controlling Revenue Authority, was stayed.

7. Later on, the said writ petition was allowed by this Court by order dated 15.5.2012, which is reproduced herein-below:

Pleadings exchanged between the parties have been perused and with the consent of the parties the writ petition is being finally decided.

The challenge made in the writ petition is to the order dated 24.12.2009 passed by the Collector Mahamaya Nagar and the appellate order thereto dated 20.4.2011 passed by the Chief Controlling Revenue Authority.

The argument advanced by the learned counsel for the petitioner is that the authorities could not have determined the deficiency in stamp duty in excess of the amount shown in the show-cause notice.

The show-cause notice is on record. It requires the petitioner to submit explanation as to why deficiency in stamp duty of Rs. 8,37,000/- may not be determined in connection with the instrument dated 13.7.2005. It means that the authorities were themselves satisfied that there was deficiency of Rs. 8,37,000/- and not more. The petitioner as such was given opportunity only in that regard. There was no notice to the petitioner to submit reply as to why penalty of Rs. 30,11,160/- may not be imposed.

The show-cause notice was never modified and no corrigendum in that regard was issued.

In view of the above, determination of deficiency in excess of the amount mentioned in the notice is clearly in violation of the principles of the natural justice and cannot be sustained in law. The authorities could not have travelled beyond the show-cause

Authorities must adhere to the initial deficiency notice and cannot impose additional charges without proper notice and justification.

Notices lacking specific details regarding deficiencies in Stamp Duty violate principles of natural justice, rendering recovery orders invalid.

Recovery proceedings for deficit stamp duty must be initiated within three years from the date of registration of the instrument, and the person concerned must be given a reasonable opportunity of be....

The necessity of conducting a spot inspection before determining stamp duty to ensure assessments are based on factual evidence rather than presumptions.

Procedural non-compliance in property valuation hearings renders resulting orders invalid, necessitating fresh proceedings to ensure parties are duly notified and allowed to participate.

No revenue recovery proceedings can be initiated without a final order under Section 47 A of the Stamp Act.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :