IN THE HIGH COURT FOR THE STATE OF TELANGANA AT HYDERABAD

P.SAM KOSHY, SUDDALA CHALAPATHI RAO, JJ.

M/s. Modern Crane Services – Appellant

Versus

The Asst. Commissioner (CT), Hyderabad and Others – Respondents

Writ Petition Nos. 7858, 7860, 7876, 7879 of 2010, Writ Petition Nos. 6927, 6930 of 2014

Decided On : 05-01-2026

| Table of Content |

|---|

| 1. writ petitions challenging assessment orders. (Para 2 , 3 , 4) |

| 2. dispute over tax classification of services. (Para 5 , 6 , 7) |

| 3. need for examining contractual agreements. (Para 8 , 9 , 10 , 11) |

| 4. judicial precedents on transfer of right to use goods. (Para 12) |

| 5. judgment in favor of petitioner; assessment orders quashed. (Para 13 , 14) |

ORDER :

1. Heard Mr. S.S.R. Viswanath, learned counsel for the petitioner and Mr. Swaroop Oorilla, learned Special Government Pleader for State Tax appearing on behalf of the respondents.

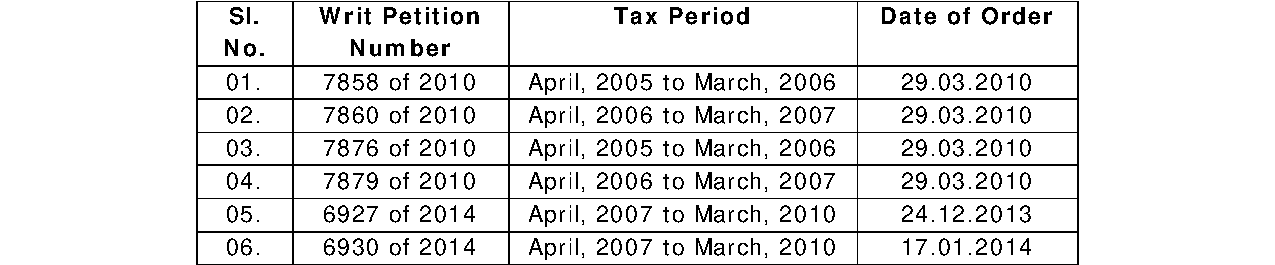

2. These are six writ petitions where the petitioner is the same firm. The challenge in all these writ petitions is to the assessment order passed by respondent No.1 for different assessment years. The details of each of the writ petitions like the writ petition number, tax period, and date of impugned order for convenience sake is reflected in the tabular form below.

3. The assessment orders passed by respondent No.1 are one which have been passed under the provisions of Andhra Pradesh Value Added Tax Act, 2005 (briefly ‘APVAT Act’ hereinafter).

4. The whole dispute is in respect of the nature of services being provided by the petitioner. Admittedly, as would be evident from the name of the petitioner firm itself, the petitioner firm renders crane services.

5. The question which came up for consideration in these writ petitions is “whether the crane services rendered by the petitioner firm would fall within the ambit of ‘a service’ under the Finance Act, 1994, or will it amount to ‘deemed service’ within the meaning of Section 4(8) of the APVAT Act?”

6. The stand of the State was that the nature of services provided by the petitioner technically amounted to transfer of right to use the cranes by the clients/customers of the petitioner firm and the cranes are always in possession and control of the clients/customers as long as they are being used by and for the clients/customers. Therefore, treating it to be a ‘deemed service’ would also bring it under the ambit of the broader term of ‘sale’ under the APVAT Act, by which the revenue generated from the said services becomes liable to VAT under the APVAT Act.

7. Whereas, the contention of the petitioner all along was that the petitioner firm is not in any manner transferring the right to use the cranes to the clients/customers. Rather, cranes are always in possession and control of the petitioner and under no circumstances the petitioner firm is parting any right over the said cranes to its customers. Hence, the fundamental requirement under Section 4(8) of the APVAT Act is not fulfilled.

8. There is no dispute so far as the fact that the aforementioned issue as to whether the services rendered by the petitioner would fall within the ambit of ‘a service’ or will it amount to ‘deemed service’ can be decided only upon scrutiny of terms and conditions of the contractual agreement entered into between the petitioner with their clients/customers. This aspect of the nature of contractual agreement being the relevant factor to ascertain the factual aspect as regards the transfer of right to use the goods is by now settled by the Hon’ble Supreme Court in the case of Bharat Sanchar Nigam Ltd. and Another vs. Union of India and Another , (2006) 3 SCC 1 . The learned Special Government for State Tax also does not dispute the said factual and legal position.

9. In the given factual circumstances, what is relevant at this juncture is to take note of the nature of contract entered into and the conditions of the said contract. A sample contract entered into between the petitioner and assignor i.e. the client is one which has been taken from lead case Writ Petition No.7858 of 2010. Some of the relevant conditions/clauses of the agreement for ready reference, are reproduced hereunder:

“The Executer agrees to execute, fulfill and discharge the work and obligations herein provided in the manner hereinafter agreed to the entire satisfaction of the Assignor.

The Executer will

Effective control over services rendered is the key factor in determining tax classification under VAT, reaffirming that possession retention by the service provider precludes deemed service status.

The transactions of leasing infrastructure equipment constitute services, not deemed sales, as effective control remains with the provider rather than transferring rights to the user.

Point of Law : Crane services provided by respondent-assessee do not constitute sale as provided under Section 2(35)(iv) of the Act of 2003 and hence, order of learned Tax Board does not call for any....

Sale of goods – A necessary ingredient of sale of goods is transfer of property in goods subject matter of sale from seller to buyer – Only because a person is allowed to use certain goods of owner, ....

The central legal point established in the judgment is that the determination of a 'sale' under the Maharashtra Value Added Tax Act, 2002 depends on the effective control and possession of the goods,....

Hiring of equipment with transfer of use is deemed a sale, exempting the transaction from service tax under the Finance Act.

The main legal point established is that the transfer of the right to use goods constitutes a deemed sale under the MVAT Act and is subject to VAT, while being excluded from the definition of 'servic....

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :