IN THE HIGH COURT OF KARNATAKA AT BENGALURU

S.R.KRISHNA KUMAR

Ltd. Cemindia JV, Represented By Its Power Of Attorney Holder Sri. Thomas K.D., S/o. Sri. K.M. Devasia – Appellant

Versus

Joint Commissioner Of Commercial Taxes, Bengaluru – Respondent

| Table of Content |

|---|

| 1. petitioner seeks relief from tax refund rejections. (Para 1 , 2 , 3) |

| 2. respondent argues against petitioner's claims. (Para 4) |

| 3. previous favorable judgments support petitioner's claims. (Para 5 , 6) |

| 4. court discusses legal definitions and precedents. (Para 8) |

ORDER :

S.R.KRISHNA KUMAR, J.

In this petition, petitioner seeks for the following reliefs:-

“a) Issue a writ of Certiorari or direction in the nature of a writ or certiorari quashing the order passed by the Respondent No.1 in Form GST-APL-04 dated 14.08.2023 under section 107(11) of the Karnataka Goods and Services Tax Act, 2017 and Central Goods and Services Tax Act, 2017 herein marked as Annexure-A.

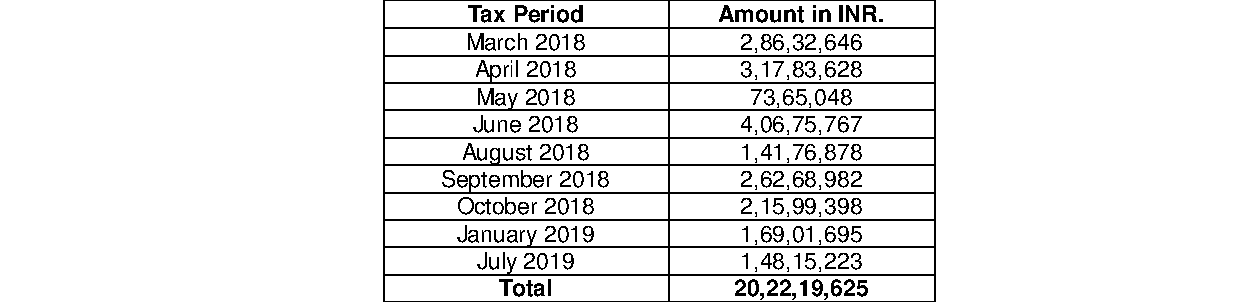

b) Issue a writ of Certiorari or direction in the nature of a writ or certiorari quashing the refund rejection order passed by the Respondent No.2 rejecting the refund claim of the petitioner in Form GST-RFD-06 for the tax period September 2019 dated 30.11.2022 herein marked as Annexure - B1.

c) Issue a writ of Certiorari or direction in the nature of a writ or certiorari quashing the refund rejection order passed by the Respondent No.2 rejecting the refund claim of the petitioner in Form GST-RFD-06 for the tax per

The court reaffirmed that construction services qualify as works contracts under the law, entitling the petitioner to refund despite previous rejections based on misinterpretation of statutory notifi....

Mandatory reimbursement of differential GST amounts by contracting authorities for works executed pre-GST, respecting established tax laws and prior contractual obligations.

Contractors are entitled to reimbursement of differential taxes arising from the transition from VAT to GST based on previous agreements, ensuring compliance with both existing guidelines and timelin....

The court emphasized adherence to procedural due process in rejecting a refund application and allowing for appeal rights under the Karnataka Goods and Services Tax Act, 2017.

The court ruled that the denial of a tax refund on grounds of limitation was wrong, emphasizing the principle of unjust enrichment, and clarified that the time limit of two years for refund applicati....

The court ruled that claims for reimbursement of GST, arising from contractual obligations, do not involve public law and should be addressed through alternative remedies such as arbitration.

The rejection of refund claims without providing an opportunity of being heard was a violation of the proviso to sub-rule (3) of rule 92 of the CGST Rules and the principles of natural justice, rende....

Refund of service tax on exempt services barred by unjust enrichment if contract inclusive of tax and incidence passed on; refund proceedings cannot modify self-assessments.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :