IN THE HIGH COURT OF KARNATAKA AT BENGALURU

S.R.KRISHNA KUMAR, J.

M/s. ABB India Limited - Appellant

Vs.

Joint Commissioner Of Commercial Taxes - Respondent

Writ Petition No. 17442 of 2025 (T-RES)

Decided On : 14-11-2025

S.R.KRISHNA KUMAR, J.

In this petition, petitioner seeks for the following reliefs:-

a. To issue order(s), directions, writ(s) in the nature of Certiorari quashing the Order No. GST/AP-10/2022- 23 dated 21.10.2023 for the period of February 2020 annexed at Annexure-A as being passed without any legal basis;

b. To issue order(s), directions, writ(s) in the nature of Certiorari quashing the Order No.:JCCT/DGSTO- 06/RFD/186/LGSTO-075/2021-22 dated 28.01.2022 along with Endorsement dated 14.02.2022 for the period of February 2020 annexed at Annexure-B as being passed without any legal basis;

c. To issue order(s), directions, writ(s) in the nature of Mandamus holding that the Petitioner is eligible to claim refund in terms of Section 54 of the CGST Act and Rule 89 of the CGST Rules;

d. To issue order(s), directions, writ(s) in the nature of Mandamus holding that the Petitioner has rightly claimed refund in terms of Section 54 while submitting its refund application for excess payment of tax in Form GST RFD-01;

e. To issue order(s), directions, writ(s) or any other relief as this Hon'ble Court deems it fit and proper in the facts and circumstance of the case in the interest of justice.”

2. Heard learned Senior counsel on behalf of the learned counsel for the petitioner and learned HCGP for the respondents and perused the material on record.

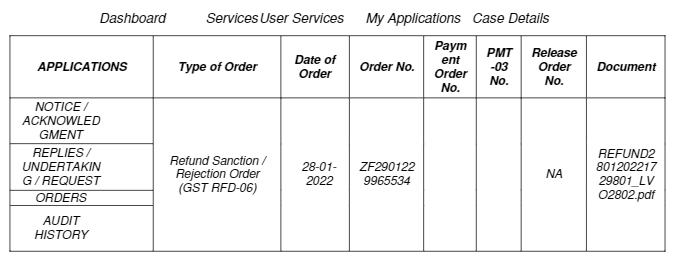

3. In addition to reiterating the various contentions urged in the memorandum of petition and referring to the material on record, learned Senior counsel for the petitioner invited my attention to the impugned refund rejection order at Annexure-B dated 28.01.2022 along with the screenshot of the status of refund application, which was rejected and accompanying by the endorsement dated 14.02.2022 contending reasons and details as to why refund claim of the petitioner was being rejected by the respondents. Aggrieved by the aforesaid refund rejection order comprising of the order, screenshot and the endorsement, the petitioner filed an appeal before the Appellate Authority, which proceeded to dismiss the appeal as not maintainable since the same was filed against the endorsement and as such, the petitioner is before this Court by way of the present petition.

4. It is submitted that both respondent Nos.1 and 2 i.e., the Original Authority and the Appellate Authority, respectively, committed an error in rejecting the refund applications of the petitioner, without taking into account the relevant provisions of KGST Act as well as the following judgments:

(i) Nam Estates Pvt. Ltd. Vs. Joint Commissioner of Commercial Taxes (Appeals-I), Bengaluru – 2024 (87) G.S.T.L. 398 (Kar.).

(ii) Joint Commissioner of Commercial Taxes (Appeals-1)Vs. Nam Estates Pvt. Ltd. – 2025 (96) G.S.T.L. 579 (Kar).

(iii) Commr. Of C.Ex. (Appeals), Bangalore Vs. KVR Construction – 2012 (26) S.T.R. 195 (Kar.).

(iv) Parijat Construction Vs. Commissioner of Central Excise, Nashik reported at 2018 (359) E.L.T. 113(Bom)

(v) 3E Infortech vs. CESTAT Chennai – 2018 (18) G.S.T.L.410 (Mad.).

(vi) Siemens Ltd. Vs. Joint Commissioner of State Tax –(2024) 22 Centax 513 (Bom.).

It is therefore submitted that the impugned order deserves to be set aside and the refund application filed by the petitioner, deserves to be allowed.

5. Per contra, learned HCGP would reiterate the various contentions urged in the Statement of Objections as well as in the written submissions and submits that there is no merit in the petition and that the same is liable to be dismissed.

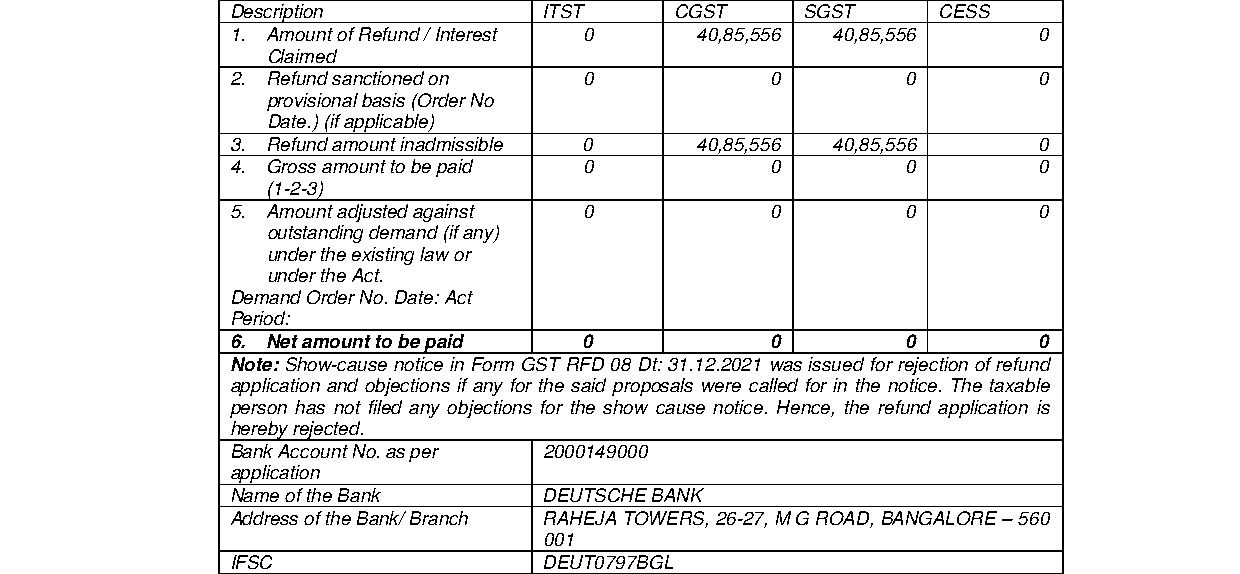

6. Before adverting the rival submissions, it is necessary to extract the refund rejection order, the screenshot showing refund rejection and the endorsement, which are hereunder:

“GOVERNMENT OF KARNATAKA

(DEPARTMENT OF COMMERCIAL TAXES)

The Karnataka Goods and service Tax Act, 2017 and

Central Goods and Service Tax Act, 2017

No.JCCT/DGSTO-06/RFD/186/LGSTO-075/2021-22

OFFICE OF THE

Assistant Commissioner of Commercial Taxes,

LVO-075, KIADB Building, Peenya

Industrial Area, 2nd stage, Bangalore – 560058

The court emphasized adherence to procedural due process in rejecting a refund application and allowing for appeal rights under the Karnataka Goods and Services Tax Act, 2017.

The court ruled that the denial of a tax refund on grounds of limitation was wrong, emphasizing the principle of unjust enrichment, and clarified that the time limit of two years for refund applicati....

The court held that a refund application filed within the statutory period cannot be rejected on grounds of limitation, and the applicant must be afforded an opportunity to be heard before any reject....

The court established that the limitation period for refund applications under the CGST Act is determined by the original filing date, not subsequent deficiencies.

The rejection of refund claims without providing an opportunity of being heard was a violation of the proviso to sub-rule (3) of rule 92 of the CGST Rules and the principles of natural justice, rende....

The court emphasized that orders passed by administrative or quasi-judicial authorities are required to stand or fall on their own and subsequent explanations by way of affidavit(s) cannot be permitt....

The rejection of a refund claim without a hearing violates principles of natural justice, necessitating remand for proper proceedings.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :