IN THE HIGH COURT OF KARNATAKA, DHARWAD BENCH

M.NAGAPRASANNA

Bagalkot Nirmithi Kendra, Represented By Its Project Director Shankarilnga, S/o. Late Nagappa Gogi – Appellant

Versus

Union Of India, Department Of Revenue Ministry Of Finance, Represented By Its Secretary – Respondent

| Table of Content |

|---|

| 1. petitioner's establishment and claims. (Para 1 , 3 , 4 , 5 , 11) |

| 2. arguments on government entity status. (Para 6 , 7) |

| 3. court's review of submissions and issues. (Para 9 , 10) |

| 4. interpretation of 'government entity' under law. (Para 12 , 13 , 14) |

| 5. final decision and order. (Para 15) |

ORDER :

M.NAGAPRASANNA, J.

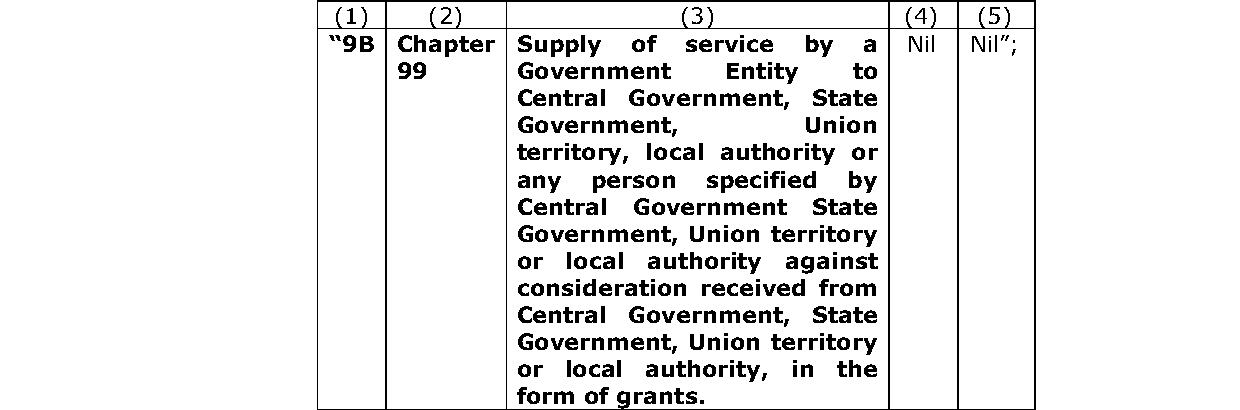

The petitioner – M/s. Bagalkot Nirmithi Kendra is at the doors of this Court seeking a direction to declare the petitioner to be a ‘Government Entity’ as defined under Clause (zfa) of the notification dated 13.10.2017 issued by the Government of Karnataka and consequently, declare that the petitioner is entitled to tax exemption under Entry No.9B of the said notification and has also called in question a communication dated 07.07.2021 issued by the fourth respondent.

2. Heard Sri Girish A. Yadawad, learned counsel for the petitioner, Sri M.B.Kanavi, learned Central Government Standing Counsel for respondent Nos.1 and 5, Sri Girish S. Hulmani, learned counsel for respondent Nos.2 to 4 and Smt. Kirtilata R. Patil, learned High Court Government Pleader for respondent Nos.6 and 7.

3. Facts in brief, germane, are as follows:

The petitioner is a Society registered und

The High Court ruled that the petitioner qualifies as a 'Government Entity,' thereby eligible for tax exemption under the Karnataka GST Act due to 100% government control and funding.

Nirmiti Kendra is a public authority under the RTI Act, subject to transparency requirements due to government control and funding.

(1) Employee of a co-operative society which is controlled or aided by Government is covered within comprehensive definition of word ‘public servant’ as defined under P.C. Act.(2) A public servant ne....

Interpretation of Statute – Punctuation, though a minor element, may be resorted to for the purpose of construction – A construction leading to an anomalous result has to be avoided.

Point of law :Prevention of corruption -Good laws alone would be not sufficient to make our country corruption free, hut there has to be effective enforcement of the same and efforts should be toward....

The Notified Area Authority, Vapi is not classified as a 'local authority' or 'governmental authority' under the GST Act, thus ineligible for GST exemption.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :