IN THE HIGH COURT OF KARNATAKA AT BENGALURU

M.NAGAPRASANNA, J.

M/s. Gunnam Infra Projects Private Limited – Appellant

Versus

The Union of India Rep. by the Secretary, Department of Revenue, New Delhi – Respondent

Writ Petition No. 17779 of 2025

Decided On : 07-11-2025

ORDER :

1. The petitioner - assessee is at the doors of this Court calling in question certain deficiency memos issued by the 6th respondent - Deputy Commissioner of Central Tax on two different dates i.e., on 20-05-2025 and 21-05-2025, rejecting the petitioner’s application for refund of the amount in DRC-03 forms.

2. Facts in brief, germane, are as follows:

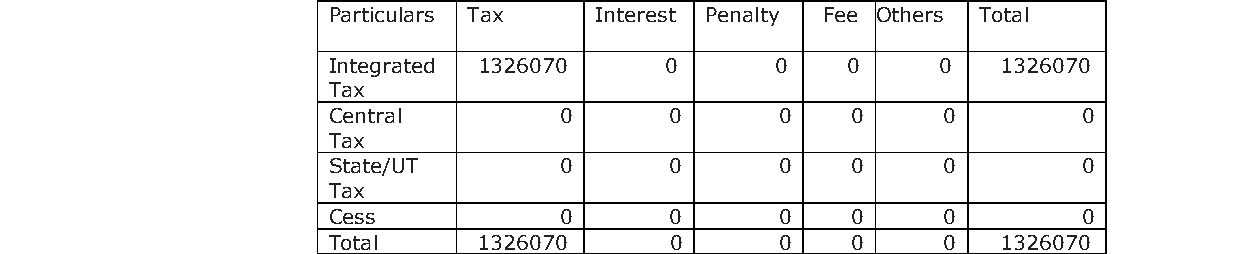

2.1. The petitioner - assessee is a private limited company, registered under the provisions of the Companies Act, 2013 and is said to be duly registered under the Goods and Services Tax enactment. On 08-06-2023, officers from the Director General of GST Intelligence and the Anti-Evasion Unit conduct simultaneous inspection at the registered office premises of the petitioner- Company purportedly under Section 67 (1) of the Central Goods and Services Tax Act, 2017 (‘CGST Act’). During the course of the proceedings, it is the case of the petitioner that he was compelled to make immediate payment of Rs.2,42,00,000/- in form DRC-03 as obtaining under Section 74 (5) of the CGST Act, to avoid threat of adverse consequences.

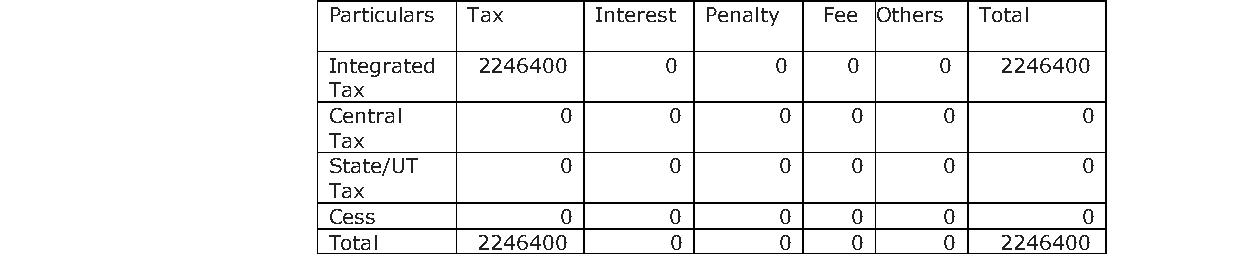

2.2. After the inspection conducted on 08-06-2023, summons was issued on 24-11-2023 directing the authorized representative of the petitioner to appear in person for conduct of an enquiry. The petitioner claims to have appeared before the concerned Officers, and during the proceedings, it is said that they once again demanded payment of Rs.22,46,400/- purportedly to cover the liability, without furnishing any determination or quantification of liability. The issuance of summons goes on this way. Between 05- 11-2024 and 06-02-2025, 4 more summons are issued directing the presence of the authorized representative of the petitioner. The assessee is said to have complied with all the summons and appears in person before the concerned authorities. Between the dates 08-06-2023 and 29-05-2024 the assessee makes four payments in DRC-03 under Section 74 (5) of the CGST Act, totally amounting to Rs.3,11,59,298/-.

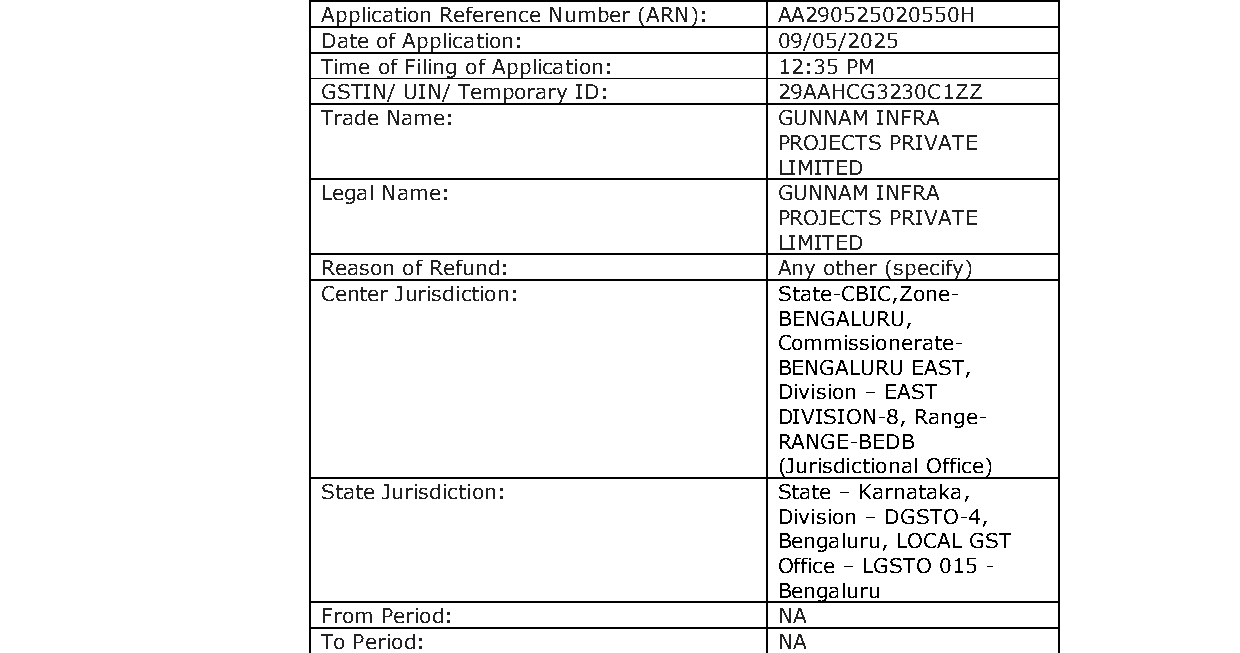

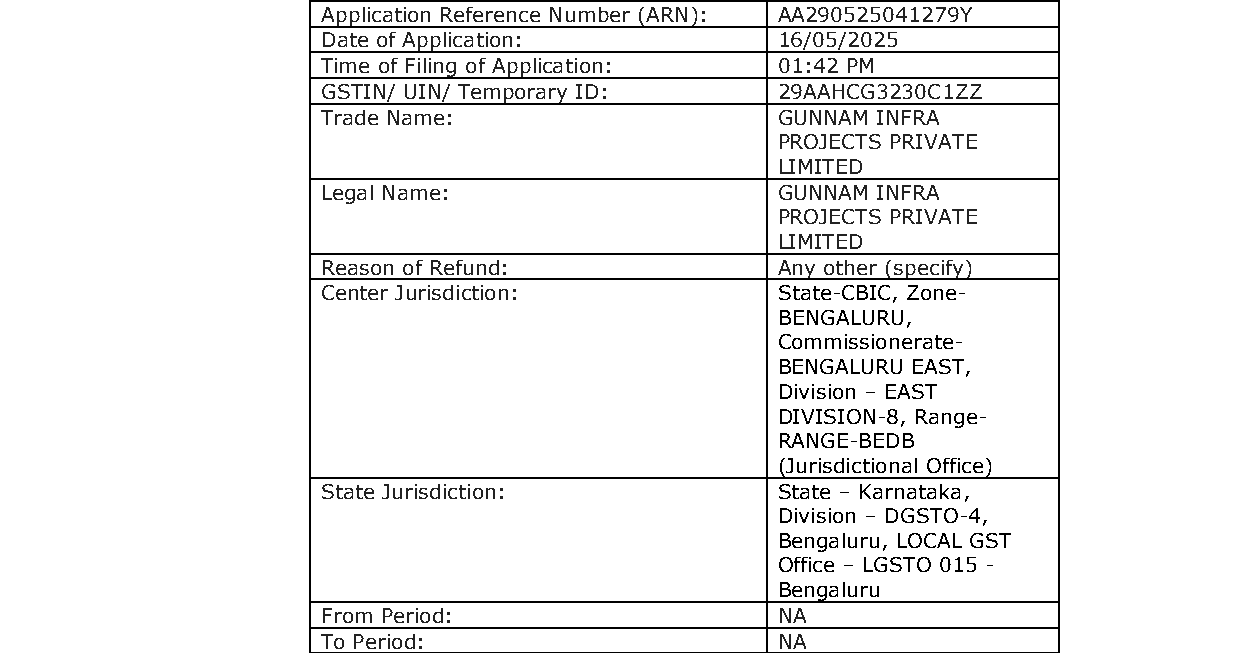

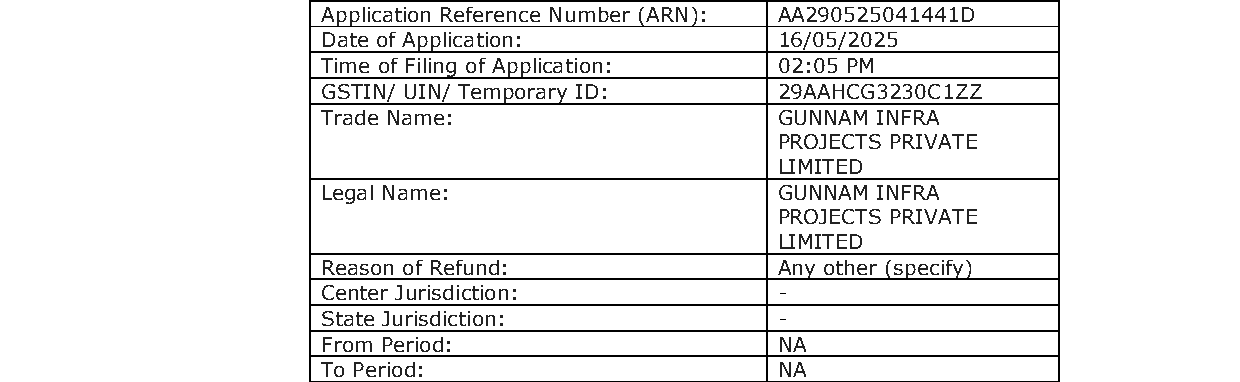

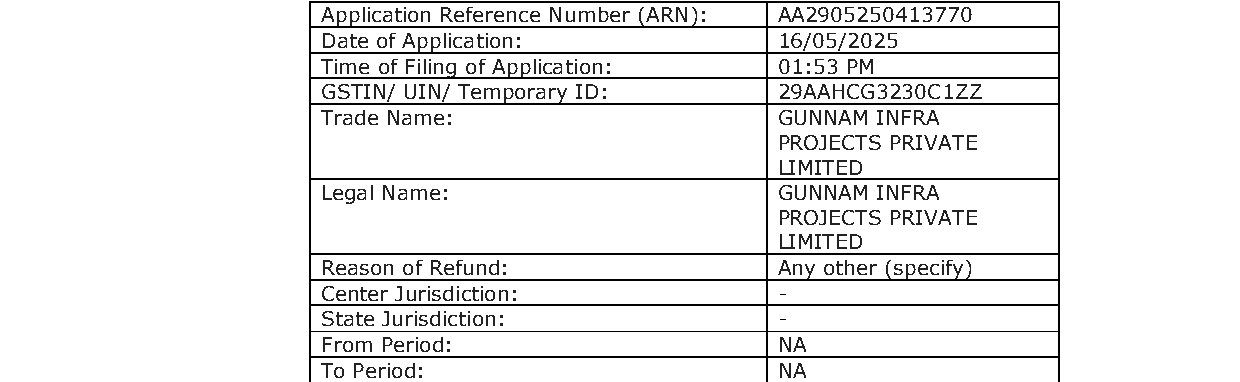

2.3. After due compliance with the summons issued by the respondent officials, on 09-05-2025 and 16-05-2025, the petitioner submits two applications seeking refund of the amount so deposited, under Section 54 of the CGST Act, through a form RFD- 01. The 6th respondent - Deputy Commissioner of Central Tax, on 20-05-2025 issues deficiency memos in form RFD-03 against the refund applications filed in the RFD-01 forms on the ground that relevant supporting documents were not appended to the application seeking refund.

2.4. It is the averment in the petition that the assessee had enclosed all the documents and therefore, there was nothing afresh to be submitted. However, the petitioner still submitted the RFD-01 forms afresh along with all the relevant documents, on 20-05-2025. The refund is once again rejected by the 6th respondent - Deputy Commissioner of Central Tax by deficiency memos on 21-05-2025, on the same ground. Therefore, the assessee is before this Court seeking quashment of the deficiency memos dated 20-05-2025 and 21-05-2025, and a direction to process the refund applications and the interest on delayed refund.

3. Heard Smt Lochana S Babu, learned counsel appearing for petitioner, Sri M N Kumar, learned Central Government Senior Panel Counsel appearing for respondent No.1, Sri Madhu N Rao, learned counsel appearing for respondents 4 and 5 and Sri M Unnikrishnan, learned counsel appearing for respondents 2, 3 and 6.

4.1. The learned counsel appearing for the petitioner would vehemently contend that refund applications ought to have been processed by the proper officer, as it was duly filled along with all necessary documents in place. The proper officer has no jurisdiction to adjudicate over the merit of a refund application and is required to process the refund application, if the application is complete and in conformity with the statutory requirements. The issuance of deficiency memos without any legally tenable or reasoned justification, amounts to co

Payments made under coercion during tax inspections cannot be construed as voluntary; proper procedures must be followed for valid refund claims.

The main legal point established in the judgment is the importance of voluntary tax payments and the consequences of non-compliance with the prescribed procedure, as well as the liability for interes....

Point Of Law: Determination of tax not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilised by reason of fraud or any wilfulmisstatement or suppression of facts.

Payments made under coercion during a search are not voluntary and must be refunded if proper acknowledgment is not provided.

Section 74(6) which states that the proper officer, on receipt of such information from the assessee, shall not serve any notice under Section 74(1) of the CGST Act to such assessee.

The court affirmed that a taxpayer's voluntary admission of dues and conditions related to cash seizure supersedes claims of coercion, leading to dismissal of the petition.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :