THE GAUHATI HIGH COURT (HIGH COURT OF ASSAM, NAGALAND, MIZORAM AND ARUNACHAL PRADESH)

DEVASHIS BARUAH, J.

Smt. Protima Borah, W/o. Lt. Krishan Kumar Borah – Petitioner

Versus

Life Insurance Corporation. Of India, REP. By Its Chairman and ORS. – Respondent

WP(C) 2783 of 016

Decided On : 18-05-2026

| Table of Content |

|---|

| 1. establishing the factual matrix surrounding the insurance contract execution, death of the insured, and claim repudiation. (Para 1 , 3 , 4 , 5 , 6 , 7) |

| 2. interpretation of the burden of proof under section 45 of the insurance act and the test for material fact non-disclosure. (Para 2 , 12 , 13 , 14 , 15 , 18 , 19) |

| 3. parties' conflicting contentions regarding non-disclosure of medical history and materiality of alleged pre-existing conditions. (Para 8 , 9 , 10 , 11) |

| 4. application of law to facts resulting in the setting aside of the arbitrary repudiation of the insurance claim. (Para 16 , 17 , 20 , 21 , 22) |

JUDGMENT :

DEVASHIS BARUAH, J.

Heard Mr. D. P. Borah, the learned counsel appearing on behalf of the Petitioners and Mr. S. P. Choudhury, the learned Standing counsel appearing on behalf of the Respondent Nos. 1 to 4.

2. Taking into account the issue involved, it is the opinion of the Court that the presence of the Respondent Nos.5 & 6 are not necessary for the adjudication of the present dispute. Accordingly, the names of the Respondent Nos. 5 & 6 are struck off.

3. The Petitioners herein are the legal representatives of one Krishna Kumar Borah (since deceased) and are aggrieved by the repudiation of the claim in respect to Policy No.444061449 vide the communication dated 11.03.2015 and under such circumstances, the Petitioners have approached this Court by filing the present writ petition.

4. The brief facts which led to the filing of the instant petition are that on 23.12.2010, the predecessor-in-interest of the Petitioners, namely late Krishna Kumar Borah who was serving as an Executive Engineer (Drilling) in the Oil and Natural Gas Corporation Limited, Sivasagar took a policy of the Life Insurance Corporation of India (for short ‘LICI’) being Policy No. 444061449. The commencement of the policy was from 23.12.2010 and the yearly premium to be paid was Rs.18,425/- which was to be deducted from his salary. The sum assured of the policy was Rs.20,00,000/-.

5. On 13.02.2013, late Krishna Kumar Borah suffered from a cardio problem and immediately he was admitted to the Srimanta Sankardeva Hospital and Research Institute, Dibrugarh. He expired on 14.02.2013 on account of cardiorespiratory failure.

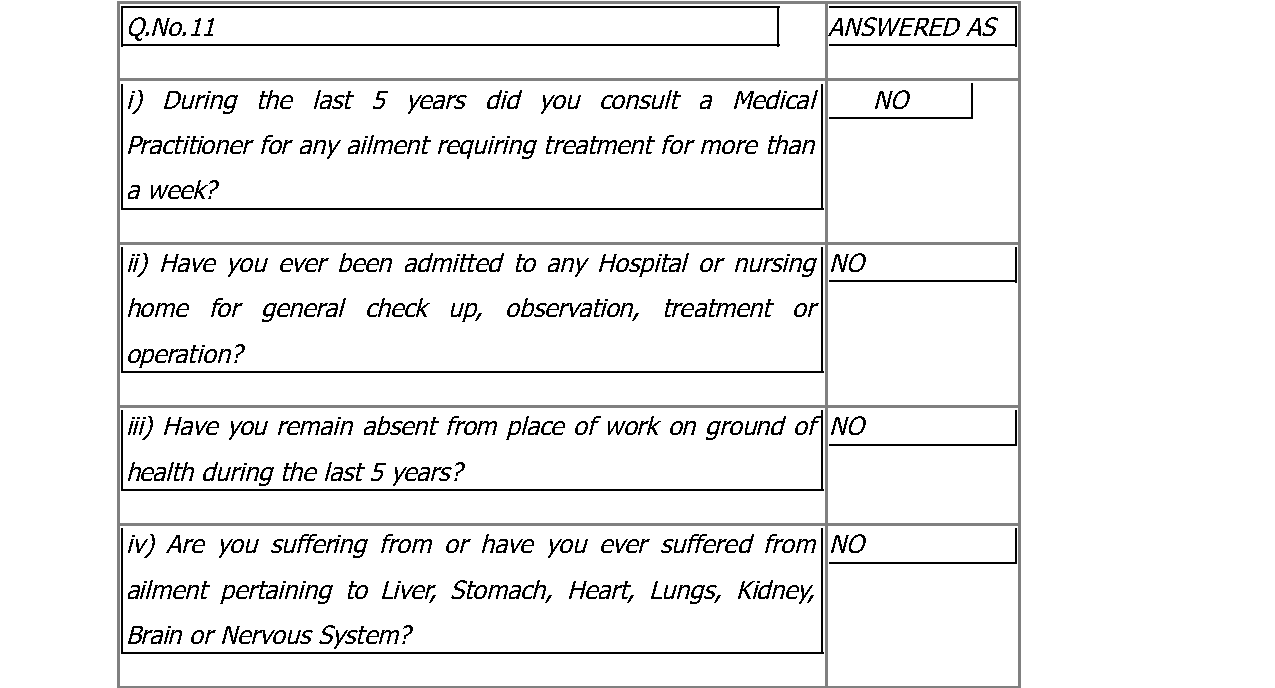

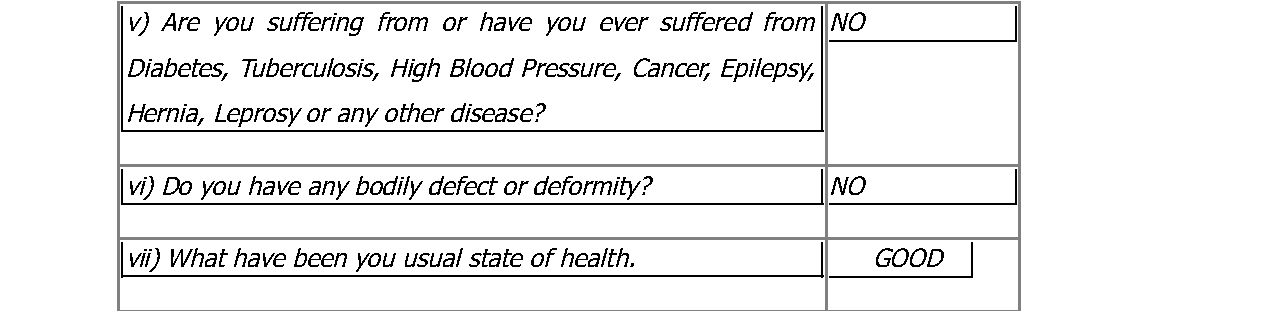

6. The wife of late Krishna Kumar Borah submitted the claim forms before the Life Insurance Corporation of India as nominee claiming the amount of Rs.20,00,000/- which was the assured sum. The said claim was rejected vide the communication dated 11.03.2015 by the LICI on the ground that the LICI had evidence and reasons to believe that late Krishna Kumar Borah was suffering from hypertension and for which he had taken EOL and HPL prior to the date of commencement of the policy and the said aspect was not disclosed at the time when the policy form was submitted. It was also alleged that late Krishna Kumar Borah had induced the LICI to issue the policy on a false statement made by him in the Proposal Statement of the health and had he disclosed the correct information, the LICI of India would not have accepted the proposal. It is on this ground the claims of the Petitioners were rejected.

7. The wife of late Krishna Kumar Borah thereupon issued a legal notice on 11.06.2015. But as there was no step taken for redressal, the wife of late Krishna Kumar Borah filed the present writ petition in the year 2016. In the meantime, the wife of late Krishna Kumar Borah expired and the Petitioner Nos. 1.1, 1.2, and 1.3 have been substituted.

8. Pursuant to the filing of the writ petition, Respondent Nos. 1 to 4 filed their affidavit-in-opposition, wherein there is no denial of the fact that the policy had been taken by Late Krishna Kumar Borah with effect from 23.12.2010 for a sum assured of Rs.20,00,000/-, and that the wife of Late Krishna Kumar Borah was the nominee under the said policy. At Paragraph No.7 of the said affidavit-in-opposition, further details have been provided as to why the claim in respect to the Policy No. 444061449 w

Insurers have the right to repudiate life insurance policies for suppression of material facts, emphasizing the duty of utmost good faith in insurance contracts.

A policy cannot be repudiated for non-disclosure of lapsed or terminated policies, especially when ambiguity exists in proposal forms; the insured must only disclose material facts that directly affe....

The duty of the proposer to disclose all material facts in the proposal form and the materiality of the non-disclosed information for the assessment of risk in insurance contracts.

The insured's obligation to disclose health status is limited to knowledge of such conditions, and unsubstantiated claims of suppression cannot invalidate a life insurance policy.

Law imposes duty of uberrima fides [utmost good faith], on Proposer to disclose material facts truthfully in order to enable Insurer to exercise discretion to enter into contract of insurance.

The duty of the insured to disclose all material facts at the time of obtaining an insurance policy, the significance of material facts in influencing the decision of a prudent insurer, and the conse....

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :