IN THE HIGH COURT OF JUDICATURE AT MADRAS

C. SARAVANAN, J.

United Capital Partners India Pvt. Ltd. - Petitioner

Versus

Principle Commissioner of Income Tax, Chennai - Respondent

W.P.No.25404 of 2021 and W.M.P.No.26825 of 2021

Decided On : 02-01-2025

| Table of Content |

|---|

| 1. factual background of taxation proceedings (Para 1 , 2 , 3 , 4 , 5 , 6) |

| 2. challenge to form-3 and tax liability. (Para 7) |

| 3. disputed tax liabilities and refund claims (Para 8 , 9 , 10 , 11 , 12 , 13 , 16 , 17) |

| 4. analysis of tax arrears and conditions (Para 18 , 19 , 20 , 21 , 22 , 23) |

| 5. court's interpretation on disputed tax liability. (Para 24) |

| 6. final decision on the writ petition (Para 25) |

ORDER :

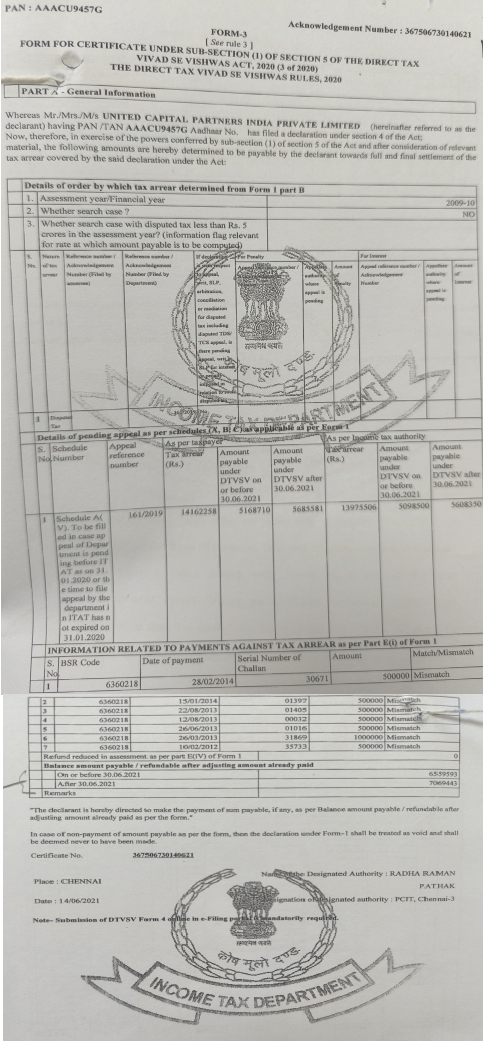

In this writ petition, the petitioner has challenged Form-3 issued by the respondent under Section 5 (1) of the Direct Tax Vivad Se Vishwas Act, 2020 read with the Direct Tax Vivad Se Vishwas Rules, 2020.

2. The petitioner had suffered originally an Assessment Order under Section 143(3) of the Income Tax, 1961 on 27.12.2011. The petitioner had filed an appeal before the Commissioner of Income Tax (Appeals)-III in ITA.No.1405/2013-2014.

3. The appeal was partly allowed on 14.02.2014. Therefore, the petitioner took further steps by filing an appeal before the Income Tax Appellate Tribunal (ITAT) in ITA.No.1058/Mds/2014 on 15.11.2020. The Department had also filed an appeal in ITA.No.1549/Mds/2014.

4. The Tribunal by its order dated 13.04.2016, had remitted the case back to the Assessing Officer, which ultimately culminated in an Assessment Order dated 30.03.2017.

5. The petitioner had filed further appeal before the Commissioner of Income Tax (Appeals)-11 in ITA.No.15/2017-2018. The Commissioner of Income Tax (Appeals)-11 by an order dated 15.11.2018, allowed the petitioner's appeal.

6. Aggrieved by the same, the Department filed a further appeal before the Income Tax Appellate Tribunal (for brevity, 'ITAT') in ITA.No.161/Chny/2019. Meanwhile, after the Commissioner of Income Tax (Appeals)-11 passed the order on 15.11.2018 in ITA.No.15/2017-2018 the Department purportedly refunded amounts to the petitioner on 25.02.2019. Primarily, a sum of Rs.40,00,000/- was refunded to the petitioner that was paid by the petitioner as tax. Apart from the above, a sum of Rs.15,47,040/- was refunded towards the aforesaid sum of Rs.40,00,000/- with interest. Thus, in all, a sum of Rs.55,47,040/- was refunded back to the petitioner. Meanwhile, the petitioner decided to settle the dispute under the Direct Tax Vivad Se Vishwas Act, 2020 read with the Direct Tax Vivad Se Vishwas Rules, 2020 by filing Form-I on 29.12.2020 The respondent had also issued Form-3 on 07.01.2021

7. It appears that there were certain mistakes in Form-I and therefore the petitioner was advised to file Revised Form-I which was also filed by the petitioner on 25.01.2021 pursuant to which, the Impugned Form-3 dated 14.06.2021 has been issued, wherein, the petitioner has been called upon to pay the following amount as detailed below:-

| Sl. No. | Date | Balance amount payable/refundable after adjusting the amount already paid |

| 1. | On or Before 30.06.2021 | Rs.65,59,593/- |

| 2. | After 30.06.2021 | Rs.70,69,443/- |

8. The case of the petitioner is that the total tax liability of the petitioner as per the respective Assessment Orders was only Rs.1,03,37,420/- and therefore, the petitioner was liable to pay only 50% of the amount as per Section 3 of the Vivad Se Vishwas Act, 2020.

9. It is further submitted that the amount that was to be paid by the petitioner would be therefore only 50% of Rs.1,03,37,420/- i.e., Rs.51,68,710/- and not the amounts specified in the impugned Form-3 dated 14.06.2021.

10. Learned counsel for the petitioner would rely on the decision of the Division Bench of the Bombay High Court in Mantelone Investment Limited Vs. Commissioner of Income Tax (International Taxation) & Ors. reported in (2022) 440 ITR 111. Specifically, the learned counsel would draw the attention of this Court to Paragraph No.11 of the said decision, wherein, it has been observed as under:-

11. Shri Vyas's reliance on Explanation to Section 7 of the Direct Tax Vivad se Vishwas Act, is misplaced inasmuch as the restriction on payment on interest under Section 2 44A of the Act is only when an assessee is eligible

The court affirmed the interpretation of 'disputed tax' and 'tax arrear' in the Direct Tax Vivad Se Vishwas Act, emphasizing that amounts including interest under Section 244A are recoverable if appe....

The amount deposited under the Income Declaration Scheme could not be forfeited and should be adjusted under the Direct Tax Vivad se Vishwas Act.

Taxation - Self-assessment tax - Assessment order - The ineligibility to file declaration relates to an assessment year in respect of which prosecution has been instituted on or before the date of de....

Income Tax - tax arrear - debarment must be in respect of tax arrear as defined - To hold that an assessee would not be eligible to file a declaration because there is a pending prosecution for asses....

Point of Law : Income Tax- Permanent establishment – Pending Appeal is a Revenue Appeal, the first proviso of Section 3 of the DTVSV Act would become applicable and, accordingly, the amount payable b....

In tax matters, entitlement to interest on delayed refunds, including on interest accrued, is affirmed, highlighting the principle that overdue amounts accrue additional interest.

The court ruled that minor delays in tax payments under the Direct Tax Vivad se Vishwas Act should not preclude benefits intended by the legislation, emphasizing a liberal interpretation of beneficia....

The Court rules that waivers and disputes concerning interest under the VSV Act can validly be treated as 'disputes', requiring the designated authority to address them despite the CIT's rejection on....

The obligation to refund tax amounts includes the right to interest for undue retention, as established in the Direct Tax Vivad se Vishwas Act, 2020.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :