IN THE HIGH COURT OF JUDICATURE AT MADRAS

C.SARAVANAN, J.

Radiant Cash Management Services Ltd, Represented by it Chairman & Managing Director – Petitioner

Versus

The Commercial Tax Officer, Office of the Assistant Commissioner (ST), Pondy Bazaar Assessment Circle, Chennai – Respondent

WP No. 49092 of 2025 and W.M.P.Nos.54840 & 54843 of 2025

Decided On : 18-12-2025

| Table of Content |

|---|

| 1. jurisdiction of tax notices. (Para 1 , 2 , 3 , 6 , 8) |

| 2. procedural history of tax assessments. (Para 4 , 5 , 7) |

| 3. details and issues raised in the show cause notices. (Para 9 , 10 , 12 , 13 , 14 , 20) |

| 4. arguments against multiple assessments. (Para 17 , 18 , 19 , 33 , 39) |

| 5. judicial interpretation on assessment overlap. (Para 22 , 23 , 24 , 28 , 29) |

| 6. limits of legal precedent in tax matters. (Para 30 , 31 , 32) |

| 7. finality of proceedings under gst. (Para 34 , 48) |

| 8. conclusion of the writ petition. (Para 49 , 50 , 51) |

ORDER :

C.SARAVANAN, J.

The Petitioner is before this Court against the impugned Show Cause Notice in FORM GST DRC 01 dated 23.09.2025 issued under Section 73 of the respective GST Enactments by the Respondent for the tax period 2021-2022.

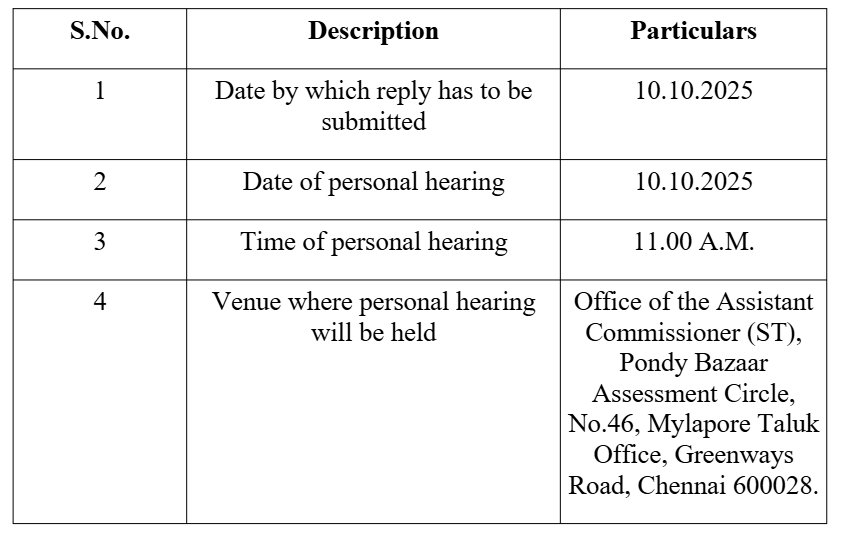

2.In the impugned Show Cause Notice in DRC 01 dated 23.09.2025, the timeline prescribed for personal hearing and due date to file reply are as follows:-

3.The impugned Show Cause Notice in DRC 01 dated 23.09.2025 is pursuant to an intimation in Form GST ASMT 10 dated 22.08.2025 issued by the Respondent for the tax period 2021-2022, wherein the Petitioner was called upon by the Respondent to file a reply on or before 21.09.2025. The Petitioner filed a Reply on 19.09.2025 to the aforesaid Intimation dated 22.08.2025.

4.The challenge to impugned Show Cause Notice in DRC 01 dated 23.09.2025 is primarily on the ground that earlier an Intimation in FORM GST DRC 01A dated 06.05.2025 was issued for the same tax period i.e., 2021-2022 to the Petitioner.

5.Before the Petitioner could respond to the aforesaid Intimation in FORM GST DRC 1A dated 06.05.2025, a Show Cause Notice in FORM GST DRC 01 dated 29.05.2025 was issued to the Petitioner for the same tax period viz., 2021-2022.

6.The Petitioner therefore approached this Court in W.P.No.23660 of 2025 against the said Show Cause Notice in FORM GST DRC 01 dated 29.05.2025. Taking note of the facts and circumstances of the case, this Court vide its Order dated 31.07.2025 ordered as under:-

“(i) The summary of show cause notice in DRC-01 dated 29.05.2025 is hereby set aside.

(ii) The petitioner is granted liberty to file reply to DRC-01A dated 06.05.2025, within a period of three weeks from the date of receipt of a copy of this order.

(iii) On filing of such reply/objection by the petitioner, the respondent shall consider the same and provide an opportunity of personal hearing and thereafter, decide the matter on merits and in accordance with law.”

7.It is the case of the Petitioner that the certified copy of the order dated 31.07.2025 in W.P.No.23660 of 2025 was received by the Petitioner only on 28.10.2025 and a Reply to Intimation in FORM GST DRC 1A dated 06.05.2025 was filed only on 09.12.2025. However, during the interregnum, the impugned Show Cause Notice in DRC 01 has been issued on 23.09.2025. Therefore, the present Writ Petition has been filed on 23.11.2025 on the ground that the impugned Show Cause Notice in DRC 01 dated 23.09.2025 was without jurisdiction.

8.It is submitted that the impugned Show Cause Notice in DRC 01 dated 23.09.2025 could not have been issued in violation of Principles of Natural Justice and in violation of the order dated 31.07.2025 passed by this Court in W.P.No.23660 of 2025.

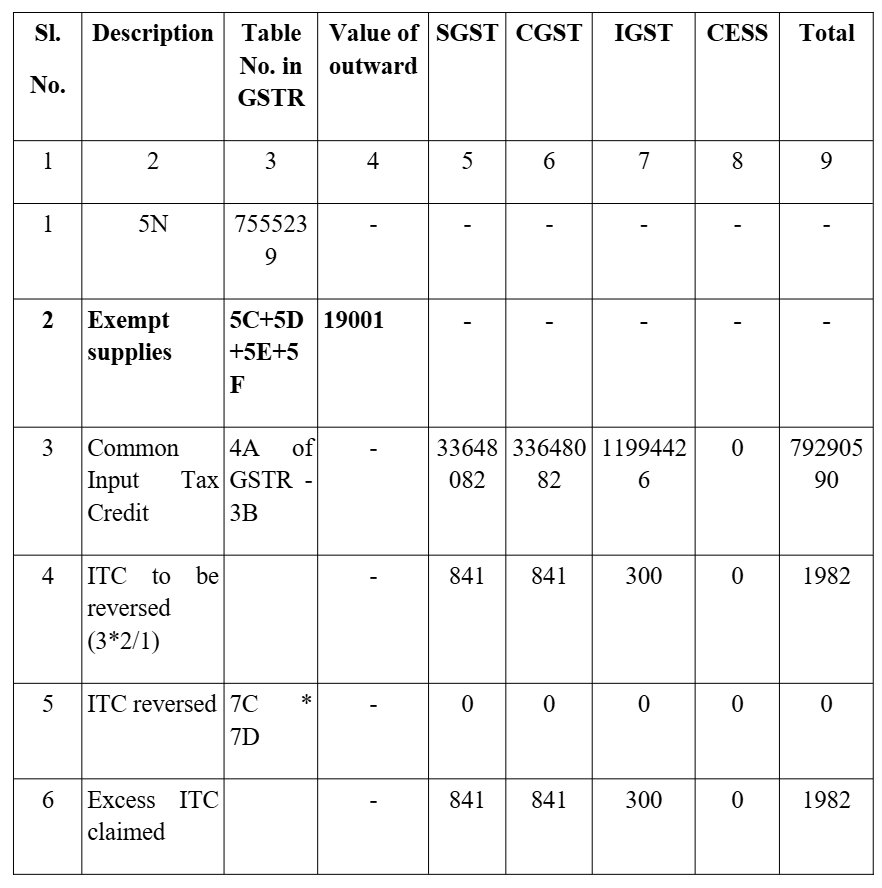

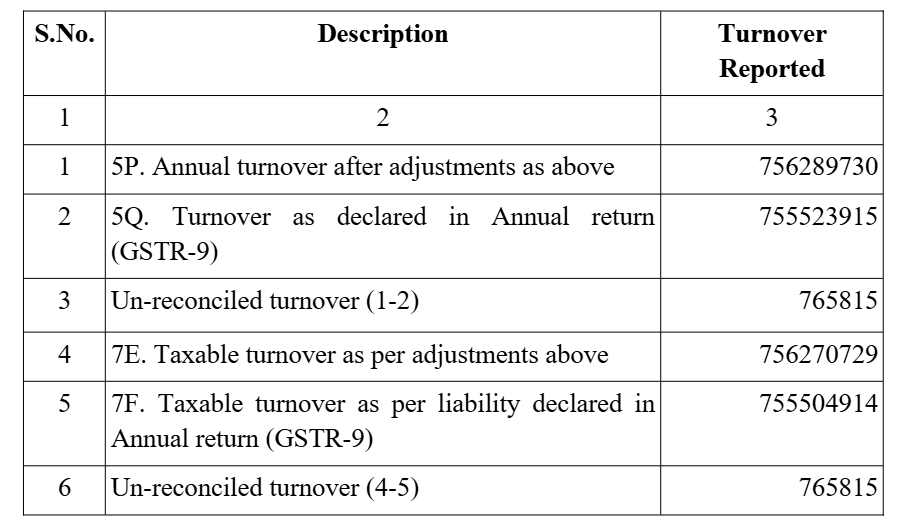

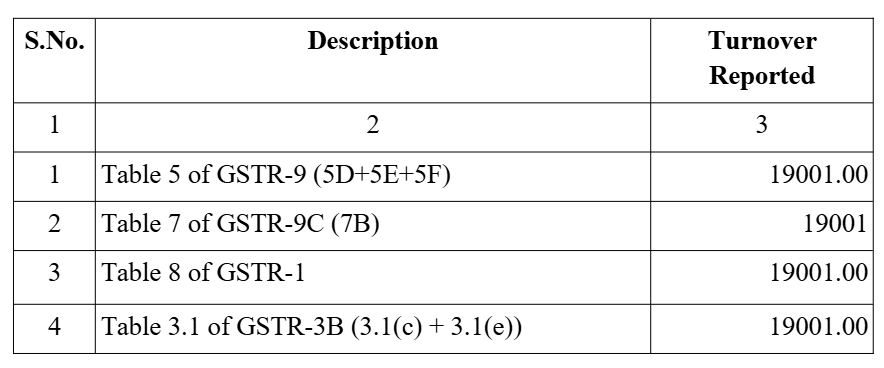

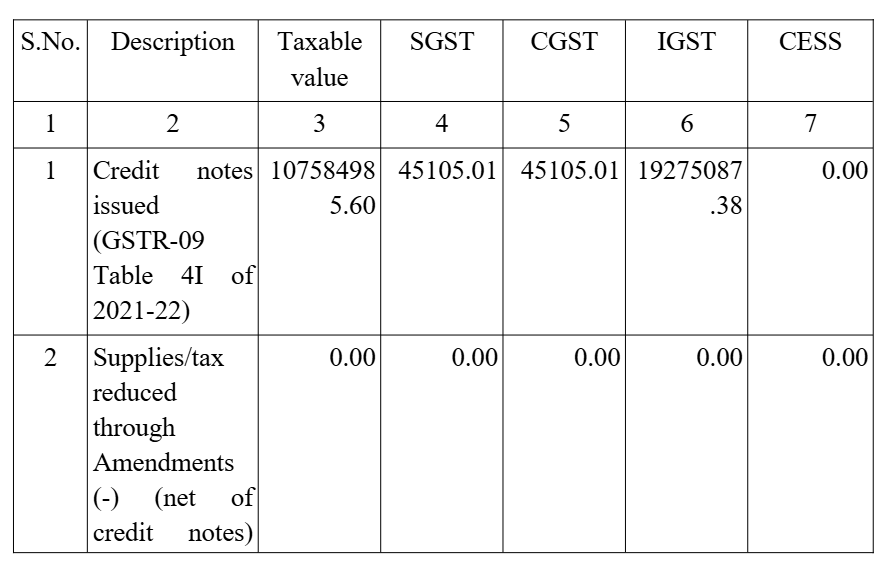

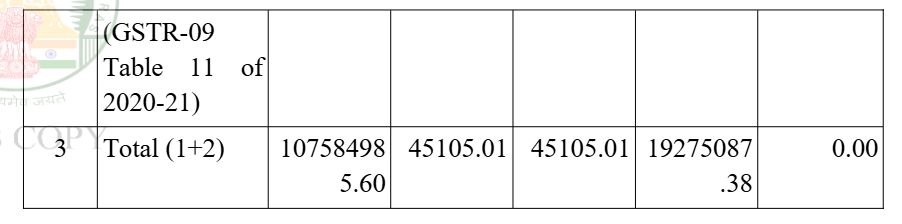

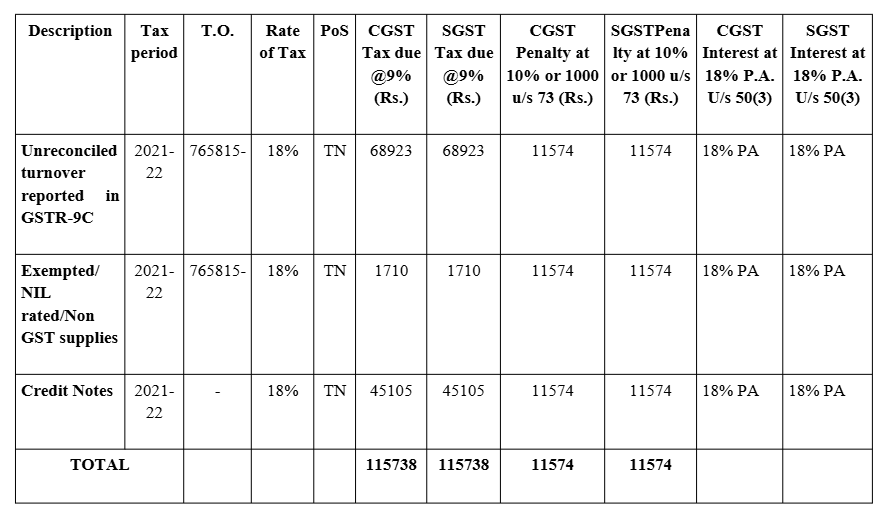

9.On comparing the content of the Show Cause Notice in FORM GST DRC 01 dated 29.05.2025 which preceded intimation in Form GST ASMT 10 dated 22.08.2025, which was quashed by this Writ Court vide order dated 31.07.2025 in W.P.No.23660 of 2025 with the impugned Show Cause Notice in FORM GST DRC 01 dated 23.09.2025 in the present Writ Petition, it is noticed that only in respect of one of the item, namely the value of outward supplies for a sum of Rs.19,001/-, there is commonality.

10.The demand/proposals in the Intimation in FORM GST DRC 01A dated 06.05.2025 which preceded the Show Cause Notice in FORM GST DRC 01 dated 29.05.2025 for the tax period 2021-2022 which was quashed by this Writ Court vide order dated 31.07.2025 in W.P.No.2366

Multiple Show Cause Notices can exist for the same tax period under GST if they pertain to different subjects, reinforcing the absence of a bar under the GST regulations.

Natural justice is upheld when multiple opportunities to be heard are provided; consolidated orders across tax periods are permissible under CGST law without causing prejudice unless demonstrable har....

Composite show-cause notices covering multiple financial years under CGST/KGST Act are illegal as assessments must pertain to individual years, respecting statutory limitations and ensuring natural j....

The court established that the issuance of a consolidated show cause notice covering multiple financial years is impermissible under the GST Act, requiring separate notices for each year to respect j....

The main legal point established in the judgment is the mandatory and imperative nature of the show cause notice requirement under Section 74(1) of the JGST Act and the need for specific charges in t....

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :