IN THE HIGH COURT OF JUDICATURE AT MADRAS

V. LAKSHMINARAYANAN, J.

M/s. VKSS & Co., Rep by its Working Partner, S.Kailai Eswaran (M/25), S/o.S.Sundararaj – Appellant

Versus

State of Tamilnadu, Rep by its Principal Secretary to Government – Respondent

W.P.No.19896 of 2025 and W.M.P.Nos.22444 & 22445 of 2025

Decided on : 15-09-2025

| Table of Content |

|---|

| 1. details of vehicle registration process and prior disputes. (Para 3 , 4 , 5) |

| 2. arguments regarding taxation options. (Para 9 , 11) |

| 3. court's initial examination of legislative framework. (Para 12 , 13 , 14 , 15 , 18) |

| 4. final ruling confirming lifetime tax requirement. (Para 30) |

ORDER :

V. LAKSHMINARAYANAN, J.

1. Heard Mr.S.Doraisamy for the petitioner, Mr.Haja Nazirudeen, Additional Advocate General assisted by Mr.M.Shajahan, Special Government Pleader and Mr.P.Hari Babu, Government Advocate for the respondents.

2.The petitioner seeks for the following relief:

“to issue a Writ of Certiorarified Mandamus calling for the records relating to the impugned order in Na.Ka.No.4930/A3/2024 dated 14.03.2025 on the file of the 2nd respondent quash the same and direct the 2nd respondent to register the vehicle of the petitioner viz., Construction Equipment Vehicle (T01241N5120A) under license for annual registration.”

3.The petitioner is a Class-I Contractor. It is a partnership firm. It purchased a Construction Equipment Vehicle Type of Body - (Motor Grader) for the purpose of its work. The purchase was made on 12.01.2024. It is not in dispute that the motor grader is covered by the definition of “Construction Equipment Vehicle”.

4.When the vehicle was sold, the vendor registered the vehicle temporarily. A temporary certificate of registration was issued by the Assistant Registering Authority, Salem Transport Department, Salem District. This registration was valid for a period of six months from 12.01.2024 to 11.07.2024. Since the petitioner proposed to use the vehicle in the State of Tamil Nadu, he submitted an application to the 2nd respondent seeking regular registration.

5.On the receipt of this application, the Regional Transport Officer, Attur, Salem District sought for the views of Assistant Audit Officer, Salem District / 3rd respondent on the issue whether the petitioner can pay registration tax annually, or life time tax at the rate of 8% of the total cost of the vehicle. The 3rd respondent answered the query stating that the petitioner would be liable to pay life time tax. On the basis of this opinion, the 2nd respondent issued an order on 14.03.2024, directing the petitioner to pay life time tax. Challenging the same, writ petition was filed before this Court in W.P.No.14824 of 2024.

6.This Court, after hearing the petitioner and the State, found that the proceedings of the Audit Officer to be unreasonable. This was because he had not examined Part I of the First Schedule, and the Tenth Schedule of the Tamil Nadu Motor Vehicle Taxation Act, 1974 , (hereinafter referred to as 'the 1974 Act'). Consequently, it set aside the order of the 2nd respondent and directed him to re-examine the entire issue in accordance with the schedule given in the Amended Act and thereafter, come to a conclusion whether annual tax is to be paid or life time tax is to be paid for a “Construction Equipment Vehicle”. A period of three months was granted for the exercise to be re-done.

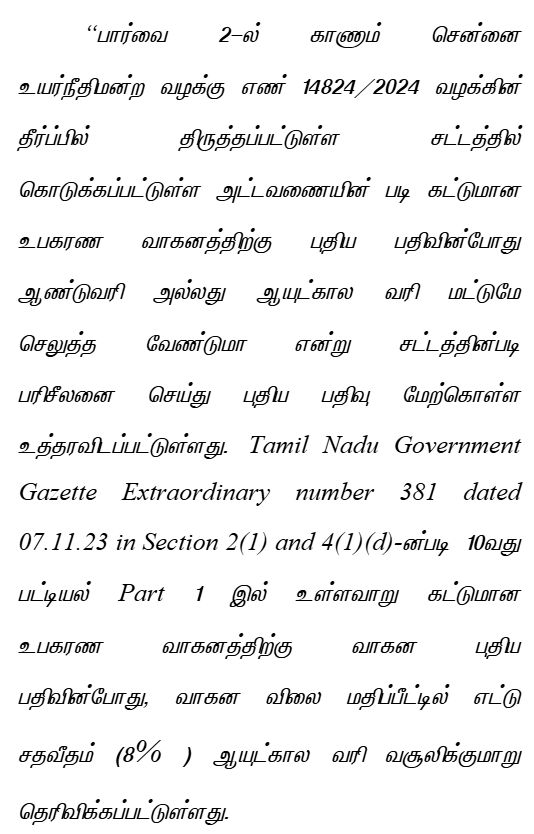

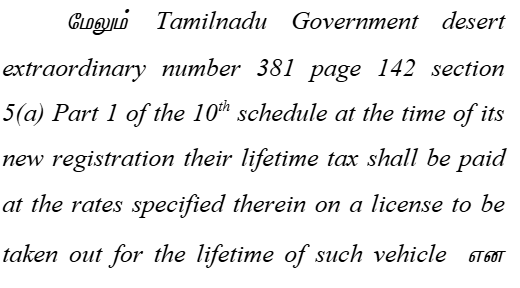

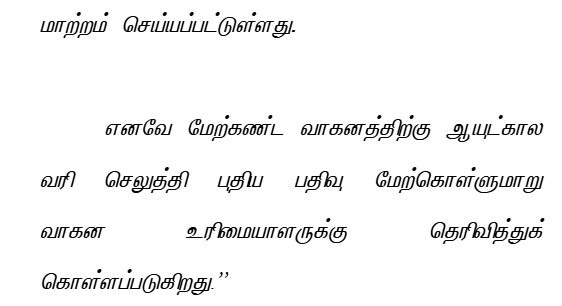

7.Pursuant to the directions given by this Court, the 2nd respondent passed the following order:

8.Aggrieved by the said order, the present writ petition.

9.Mr.S.Doraisamy argued that the petitioner is not interested in paying the life time tax for his vehicle. The petitioner wants to pay tax annually. He pleads that the 2nd respondent had wrongly interpreted the provisions of the 1974 Act and had passed the impugned order. He pointed out that the impugned order does not state anything with respect to Part-I of the First Schedule, or why the annual tax specified in Part-I of the First Schedule is not available to the petitioner. He relied upon Section 4 (1) of the 1974 Act, [wrongfully stated in the affidavit as 4(1)(a) – There is no clause (a) in Section 4 (1)] of the said Act to state when an option is given to the owner of the vehicle, it is for him to pay the annual tax or life time tax. The Registering Authority cannot insist upon the payment of life time tax

The court ruled that under the amended Tamil Nadu Motor Vehicle Taxation Act, new construction equipment vehicles must pay lifetime tax rather than having the option for annual tax.

Tax should be levied on the cost of the motor vehicle as per the Andhra Pradesh Motor Vehicles Taxation Act, 1963, and in compliance with constitutional provisions.

Temporary use of a vehicle registered in another state does not incur local lifetime tax liability unless kept for over twelve months.

Heavy Earth Moving Machinery, intended for off-road use only, do not qualify as 'motor vehicles' under the Motor Vehicles Act and are not subject to taxation, as confirmed by expert certifications.

The court affirmed that tax paid by petitioners for transport vehicles up to 31.03.2015 in one successor state is valid in both states, prohibiting double taxation thereafter.

A vehicle officially classified and registered as a 'goods carriage' cannot be unilaterally reclassified by tax authorities as a 'construction equipment vehicle' to demand lifetime lump-sum tax inste....

The liability for motor vehicle tax persists regardless of usage location, provided vehicles are not reported as non-functional per statutory requirements.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :