IN THE HIGH COURT OF JUDICATURE AT MADRAS

C. SARAVANAN, J.

S. Palani – Appellant

Versus

The Additional/Joint/Deputy/Assistant Commissioner of Income Tax – Respondent

W.P. No. 15325 of 2023, W.M.P. Nos. 14834, 14835, 14837 of 2023

Decided On : 20-04-2026

| Table of Content |

|---|

| 1. challenges section 148 notice and assessment order (Para 1 , 2) |

ORDER :

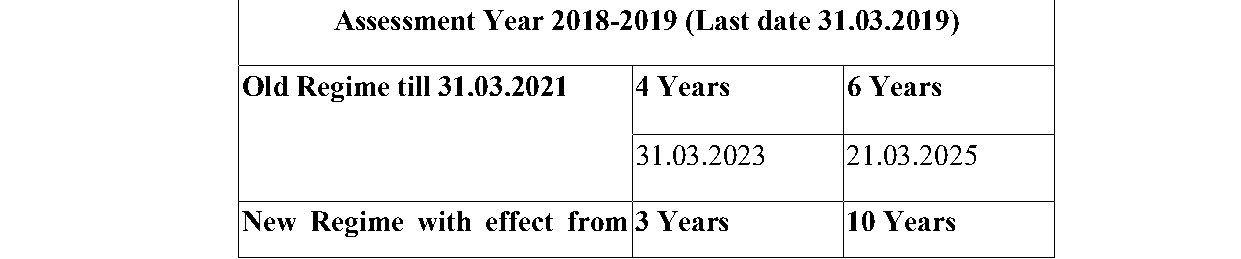

1. In this Writ Petition, the Petitioner has challenged the impugned Notice dated 31.03.2022 issued under Section 148 Notice to the petitioner by the 2nd Respondent and consequential impugned Assessment Order dated 06.03.2023 passed under Section 147 read with Section 144 and B of the Income Tax Act, 1961 for the Assessment Year 2018-2019.

2. The facts of the case reveal that the impugned proceedings was preceded with a Notice dated 21.03.2022 issued under Section 148A(b) of the Income Tax Act, 1961 followed by an Order dated 31.03.2022 under A(d) of the and issuance of a Notice also dated 31.03.2022.

3. The Petitioner had earlier filed a Return of Income under Section 139(1) of the Income Tax Act, 1961 on 29.03.2019. In the said Return of Income, the Petitioner had declared a taxable income of Rs.30,09,400/- Pursuant to the Notice dated 31.03.2022 issued under Section 148 of the , the Petitioner filed a fresh Return of Income on 25.04.2022 whereby the Petitioner reiterated the declaration in the Return of Income filed under Section 139(1) of the on 29.03.2019.

4. Subsequently, the assessment was transferred to the Faceless Unit. Thus, Notices were issued to the Petitioner under Section 142(1) and Section 143(2) of the Income Tax Act, 1961 by the 1st respondent. The contention of the Petitioner is that all the communications were addressed to the Petitioner’s email ID namely absesoscm@yahoo.com, which the Petitioner had long ceased to operate.

5. It is further case of the Petitioner that subsequent to Section 148 Notice dated 31.03.2022, Return of Income was filed from the Petitioner’s new email ID namely, aura.banu1@gmail.com and the Petitioner failed to check the Notices as they were posted in the web portal, and that, the Petitioner overlooked these Notices that preceded the impugned Assessment Order dated 06.03.2023.

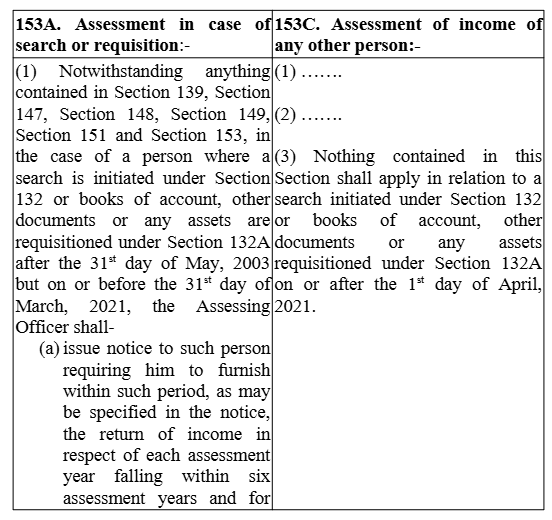

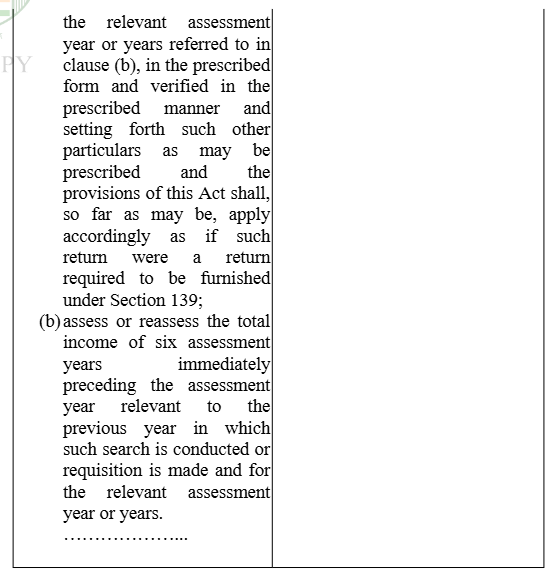

6. It is the contention of the Petitioner that the entire proceeding emanates from a search conducted under Section 132 of the Income Tax Act, 1961on the searched person namely M/s. G Squareand M/s. Saravana Stores Bramandamai and therefore proceedings can be initiated only under Section 153Cof the and not under Section 148 of the Income Tax Act, 1961. The affidavit is silent on the date of such search.

7. That apart, learned counsel for the Petitioner submits that addition of a sum ofRs.4,87,50,000/-to the income of the Petitioner as undisclosed income of the Petitioner under Section 69A of the Income Tax Act, 1961as well as in the hands of the Petitioner’s brother namely Mr. Shanmugasundaram Subramanian was unjustified.

8. It is submitted that the said income was added to the latters income vide similar proceeding dated 24.03.2023 for the same Assessment Year under Section 144 and B of the Income Tax Act, 1961 in the hands of the Petitioner’s brother namely Mr.Shanmugasundaram Subramanian.

9. Alternatively, the learned counsel for the Petitioner submits that the Petitioner will be satisfied if the case is remitted back to the Respondents to pass fresh orders in lieu of the impugned Assessment Order dated 06.03.2023.

10. The learned Senior Standing Counsel for the Respondents on the other hand would submit that the impugned Assessment Order is well- reasoned and does not merit any interference in the hands of this Court under Article 226 of the Constitution of India.

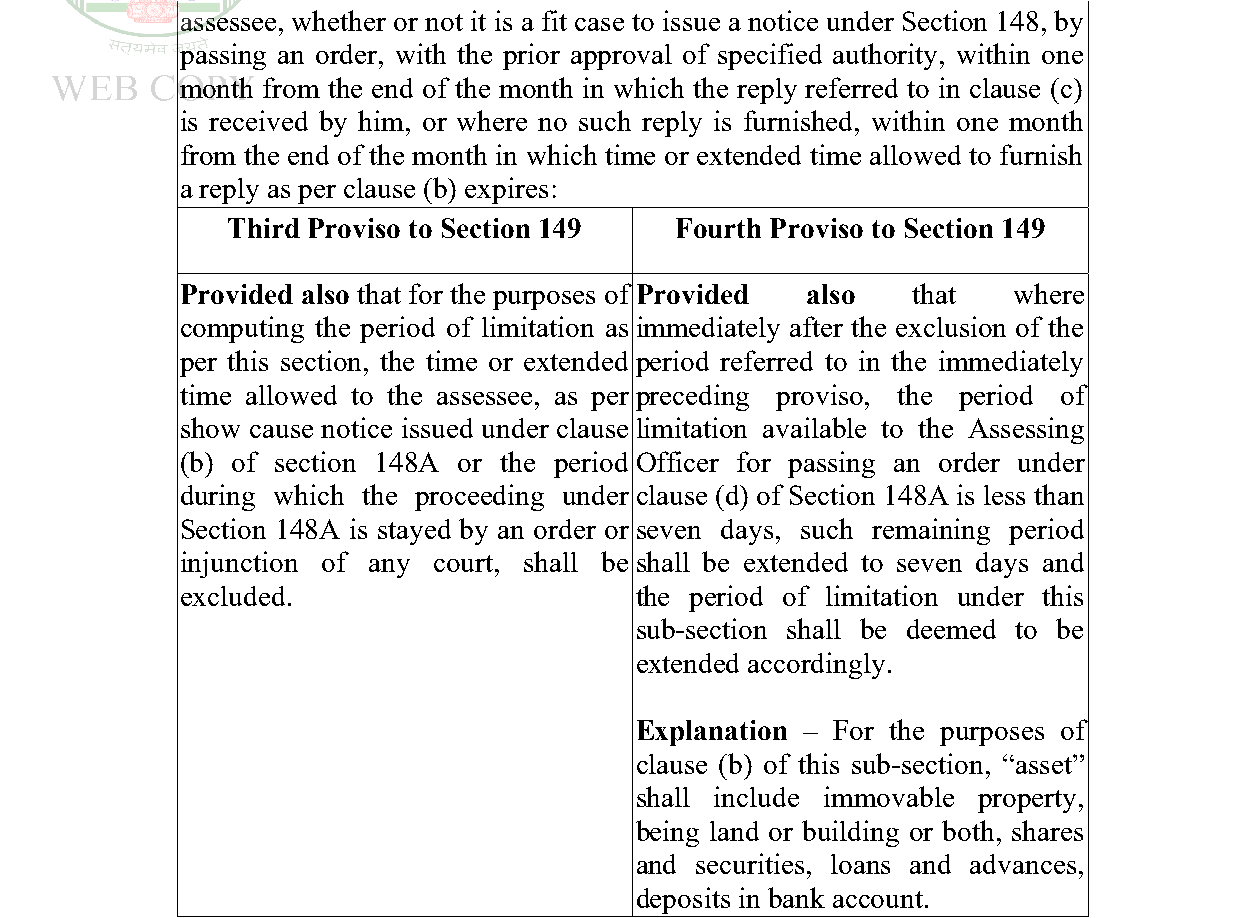

11. It is submitted that after the amendment to the provisions of the Income Tax Act, 1961 vide Finance Act, 2021, new set of provisions were incorporated in the and therefore the argument that the proceedings were without jurisdiction has to be rejected.

12. It is submitted that with effect from 01.04.2021, Section 153A to Section 153C of the Income Tax Act, 1961 stood deleted and assessment under Section 143(3) of the including reassessment in the case of escape assessment could be only under the machinery under Section 148 of the as in force with effect from the sai

Post Finance Act 2021, s.148 reassessment valid even for search-derived info if search after 01.04.2021; presume recent searches post-date; quash assessment for natural justice violation if reasonabl....

The main legal point established in the judgment is the significance of adhering to the procedure prescribed under Section 148A of the Income Tax Act, 1961 before initiating reassessment proceedings.....

The court ruled that proceedings under Section 148 of the Income Tax Act are improper when material seized relates to a person other than the one searched, necessitating the application of Section 15....

The issuance of notice under Section 148A(b) was barred by limitation, violating the requirement for a reasonable opportunity to respond.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :