BEFORE THE MADURAI BENCH OF MADRAS HIGH COURT

G.R.SWAMINATHAN, K.RAJASEKAR

Omega Traders – Appellant

Versus

Assistant Commissioner, Office of the Assistant Commissioner of GST & Central Excise – Respondent

| Table of Content |

|---|

| 1. this intra-court appeal is directed against the common order dismissing the writ petition. (Para 1) |

| 2. the appellant processes raw tobacco, seeking reclassification under gst following regulatory bans. (Para 2 , 3 , 4 , 5) |

| 3. legal representatives presented arguments based on historical classification and regulatory compliance. (Para 6 , 7) |

| 4. court reviewed procedural aspects concerning alternative remedies available to the appellant. (Para 8 , 9 , 10 , 11) |

| 5. court ruled on the absence of manufacturing, reaffirming unmanufactured tobacco classification. (Para 12 , 21) |

| 6. final judgment allowed the appeal and set aside previous orders. (Para 22) |

JUDGMENT :

G.R. SWAMINATHAN, J.

This intra-court appeal is directed against the common order dated 24.10.2024 dismissing WP(MD)No.5414 of 2021 filed by the appellant herein. The writ petition filed by the appellant was taken up for disposal along with a few more writ petitions and given a common disposal by the learned Single Judge.

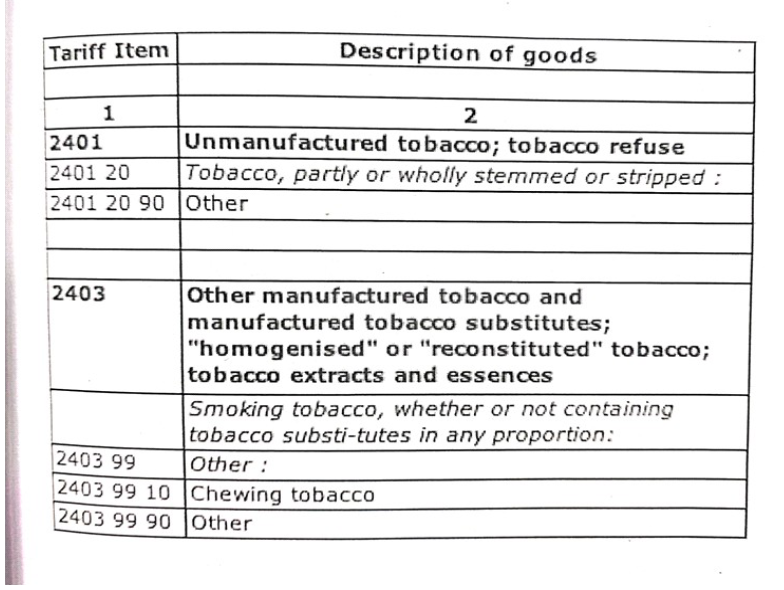

2.The appellant is engaged in the tobacco business. Their activity comprises the following : procuring raw tobacco from farmers, processing by drying, stripping and thereafter dipping it in jaggery wa

The court established that the classification of tobacco products relies on the presence of manufacturing activity; absence of such activity necessitates classification as unmanufactured tobacco unde....

The court established that the burden of proof on classification disputes lies with the Revenue, affirming that misclassification can lead to penalties, while reclassifications must reflect actual pr....

Where both the assessee and the excise department have consistently classified a product under a specific tariff heading for years in returns and official orders, the department is precluded from uni....

The main legal point established in the judgment is that the product in question is made from plastic granules and cannot be treated as textile articles, as uniformly adopted by the Appellate Authori....

In a classification dispute, the extended period of limitation cannot be invoked and the process of distillation does not amount to manufacture.

The process of roasting Rava does not amount to manufacture under Section 2(f) of the Central Excise Act, thus no excise duty is applicable.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :