IN THE HIGH COURT OF KARNATAKA AT BENGALURU

S.R. KRISHNA KUMAR, J.

Haleyur Krishnegowda Madhuchandra - Petitioner

Versus

Income Tax Officer – Respondent

WRIT PETITION NO. 4188 OF 2025 (T-IT)

Decided On : 18-12-2025

| Table of Content |

|---|

| 1. petitioner seeks multiple writs against various notices. (Para 1) |

| 2. respondent issued notices under old and amended income tax act provisions. (Para 2 , 3) |

| 3. impugned orders and notices were barred by limitation as per supreme court rulings. (Para 4 , 6 , 7) |

| 4. respondents argue against the merits of the petition. (Para 5) |

| 5. court quashes invalid notices/orders based on supreme court's reasoning. (Para 8) |

ORDER :

S.R.KRISHNA KUMAR, J.

In this petition, petitioner seeks for the following reliefs:-

“ i) Issue a writ of Certiorari or direction in the nature of a writ of certiorari quashing the notice under Section 148 of the Act, dated 30/06/2021 bearing No. DIN ITBA/AST/S/148/2021-22/1033907067(1), issued by the Respondent No.1 for the assessment year 2013-14 herein marked as Annexure A

ii) Issue a writ of Certiorari or direction in the nature of a writ of certiorari quashing the notice under Section 148A(b) of dated 25/05/2022 bearing DIN No. ITBA/COM/F/17/2022-23/1043164568(1), issued by the Respondent No.1 for the assessment year 2013-14 herein marked as Annexure - A1.

iii) Issue a writ of Certiorari or direction in the nature of a writ of certiorari quashing the order under Section 148A(d) of the Act, dated 26/07/2022, bearing DIN No. ITBA/COM/F/17/2022-23/1044117203(1) issued by the Respondent No.1 for the assessment year 2013-14 herein marked as Annexure - A2.

iv) Issue a writ of Certiorari or direction in the nature of a writ of certiorari quashing the notice under Section 148 of the Act dated No. 28/07/2022 bearing DIN ITBA/COM/F/17/2022-23/1044253756(1) Issued by the Respondent No.1 for the assessment year 2013-14 herein marked as Annexure- АЗ.

v) Issue a writ of Certiorari or direction in the nature of a writ of certiorari quashing the intimation letter dated 28/07/2022 for notice under Section 148 of the Act bearing DIN No. ITBA/AST/S/91/2022-23/1044254037(1), Issued by the Respondent No.1 for the assessment year 2013-14 herein marked as Annexure - A4.

vi) Issue a writ of Certiorari or direction in the nature of a writ of certiorari quashing the order passed Under section 147 r.w.s 144 dated 19/05/2023 bearing DIN No. ITBA/AST/5/147/2023-24/1053001187(1) issued by the Respondent No. 1 for the assessment year 2013-14 herein marked as Annexure - A5.

vii) Issue a writ of Certiorari or direction in the nature of a writ of certiorari quashing the penalty order under section 271(1)(c) of the Act dated 21/08/2023 bearing DIN No. TBA/PNL/F/271(1)(c)/2023-24/1055529970(1), issued by the Respondent No.2 for the assessment year 2013-14 herein marked as Annexure - A6.

viii) And pass such other orders as this Hon'ble Court deems fit and proper in the interest of justice and equity.”

2. Heard learned counsel for the petitioner and learned counsel for the respondents and perused the material on record.

3. A perusal of the material on record will indicate that in relation to the assessment year 2013-14, the respondent No.1 issued a notice dated 30.06.2021 under Section 148 of the Income Tax Act, prior to the said provisions being amended w.e.f., 01.04.2021. Subsequently, in the case of Union of India vs. Ashish Agarwal [2022] 138 taxmann.com 64 (SC), the Apex Court while dealing with the aforesaid amendment and notices issued to the assessee under subsequent to the amendment, issued the following directions:

"10. In view of the above and for the reasons stated above, the present Appeals are ALLOWED IN PART. The impugned common judgments and orders passed by the High Court of Judicature at Allahabad in W.T. No. 524/2021 and other allied tax appeals/petitions, is/are hereby modified and substituted as under:

(i) The impugned section 148 notices issued to the respective assessees which were issued under unamended section 148 of the IT Act, which were the subject matter of writ petitions before the various respective High Courts shall be deemed to have been issued under section 148A of the IT Act as substituted by the Finance

Notices and orders issued under the Income Tax Act were quashed as time-barred, adhering to Supreme Court mandates on limitation periods.

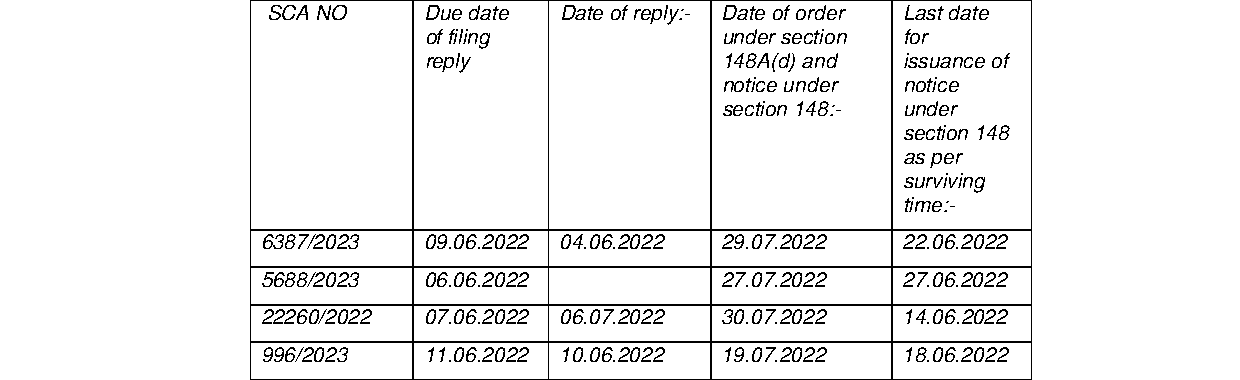

Notices under Section 148 of the Income Tax Act issued beyond prescribed limitation are invalid as per Supreme Court directives.

Notices issued beyond the established statutory limitation are invalid and must be quashed, emphasizing compliance with timelines set by legal precedents in tax law.

Notices issued under Section 148 of the Income Tax Act are invalid if they are issued beyond the stipulated 'surviving time' as established by the Apex Court, necessitating adherence to prescribed li....

Notices issued under the Income Tax Act beyond the statutory limitation set by Supreme Court precedents are invalid and must be quashed.

Notices issued beyond the limitation period established by the Income-tax Act and relevant Supreme Court directives are deemed invalid.

Notices issued under sections 148 and 148A(d) of the Income Tax Act beyond the specified limitation period are invalid and subject to quashing.

Notices issued for reassessment under the Income Tax Act must adhere to statutory time limits; those issued beyond the time limit are considered invalid.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :