IN THE HIGH COURT OF KARNATAKA AT BENGALURU

S.R.KRISHNA KUMAR, J.

M/s Sunvik Steels Pvt. Ltd. - Appellant

Vs.

Deputy/Assistant Commissioner Of Income Tax, Circle 6(1)(1), Bangalore - Respondent

Writ Petition No. 17712 of 2022 (T-IT)

Decided On : 26-11-2025

| Table of Content |

|---|

| 1. petitioner's prayer to quash income tax notice (Para 1 , 3) |

| 2. court's analysis of procedural compliance and limitation (Para 2 , 5 , 7 , 8) |

| 3. contentions on limitation and invalidity of notices (Para 4 , 6) |

| 4. final order to quash notices and proceedings (Para 9) |

ORDER :

S.R.KRISHNA KUMAR, J.

In this petition, the petitioner seeks the following prayer:

"i. Quashing the impugned order dated 28.07.2022 bearing the 1st ITBA/COM/F/17/2022-23/1044244818(1) passed by the 1st Respondent under Section 148A(d) of the Income-tax Act, 1961, for the assessment year 2013-14 (Annexure 'A');

ii. Quashing the impugned notice dated 28.07.2022 and the accompanying document dated 29.07.2022 bearing ITBA/AST/S/91/2022-23/1044284519(1) issued by the 1st Respondent under Section 148 of the Income-tax Act, 1961, for the assessment year 2013-14 (Annexures 'B-1' and 'B-2'); iii. Declaring that the impugned proceedings initiated by the 1st Respondent under Section 147 read with Sections 148 and 148A of the Act are barred by limitation and opposed to the said provisions and are, therefore, without jurisdiction;

iv. Quashing the impugned Instruction bearing No.1/2022 dated 11.05.2022 issued by the 6th Respondent (Annexure C) to the extent that the same purports to direct that fresh notices under S.148 can be issued for AY 2013-14 so long as the quantum of income alleged to have escaped assessment is more than Rs.50 lakhs, without having regard to the express limitation prohibitions prescribed in S.149 of the Act as they stood before 01.04.2021 and with effect from the said date; and v. Pass such other or further order as this Hon'ble Court may deem fit in the facts and circumstances of the case, and in the interests of justice and equity."

2. Heard learned counsel for the petitioner and learned counsel for the respondents and perused the material on record.

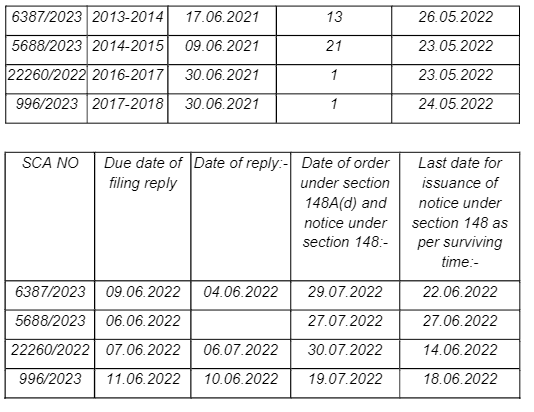

3. A perusal of the material on record will indicate that in relation to the assessment year 2013-14, respondent No.1 issued a notice dated 29.06.2021 under Section 148 of the Income Tax Act, 1961 prior to the said provisions being amended w.e.f., 01.04.2021. Subsequently, in the case of Union of India vs. Ashish Agarwal – [2022] 138 taxmann.com 64 (SC), the Apex Court while dealing with the aforesaid amendment and notices issued to the assessee under subsequent to the amendment, issued the following directions:

“10. In view of the above and for the reasons stated above, the present Appeals are ALLOWED IN PART. The impugned common judgments and orders passed by the High Court of Judicature at Allahabad in W.T. No. 524/2021 and other allied tax appeals/petitions, is/are hereby modified and substituted as under:

(i) The impugned section 148 notices issued to the respective assessees which were issued under unamended section 148 of the IT Act, which were the subject matter of writ petitions before the various respective High Courts shall be deemed to have been issued under section 148A of the IT Act as substituted by the Finance Act, 2021 and construed or treated to be showcause notices in terms of section 148A(b). The assessing officer shall, within thirty days from today provide to the respective assessees information and material relied upon by the Revenue, so that the assesees can reply to the showcause notices within two weeks thereafter;

(ii) The requirement of conducting any enquiry, if required, with the prior approval of specified authority under section 148A(a) is hereby dispensed with as a onetime measure visàvis those notices which have been issued under section 148 of the unamended Act from 01.04.2021 till date, including those which have been quashed by the High Courts. Even otherwise as observed hereinabove holding any enquiry with the prior approval of specified authority is not mandatory but it is for the concerned Assessing Officers to hold any enquiry, if required;

(iii) The assessing officers shall thereafter pass orders in terms of section 148A(d) in respect of each of the

Notices issued beyond the limitation period established by the Income-tax Act and relevant Supreme Court directives are deemed invalid.

Notices issued beyond the established statutory limitation are invalid and must be quashed, emphasizing compliance with timelines set by legal precedents in tax law.

Notices issued under the Income Tax Act beyond the statutory limitation set by Supreme Court precedents are invalid and must be quashed.

Notices and orders issued under the Income Tax Act were quashed as time-barred, adhering to Supreme Court mandates on limitation periods.

Notices under Section 148 of the Income Tax Act issued beyond prescribed limitation are invalid as per Supreme Court directives.

Notices issued under sections 148 and 148A(d) of the Income Tax Act beyond the specified limitation period are invalid and subject to quashing.

Notices issued under Section 148 of the Income Tax Act are invalid if they are issued beyond the stipulated 'surviving time' as established by the Apex Court, necessitating adherence to prescribed li....

Notices issued for reassessment under the Income Tax Act must adhere to statutory time limits; those issued beyond the time limit are considered invalid.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :