IN THE HIGH COURT OF KARNATAKA, AT DHARWAD

M.NAGAPRASANNA, J.

M/s Rani Channamma University, Represented By Ms. Rajashree Jainapur, D/o. Sri. Husanappa Jainapur – Petitioner

Versus

Commercial Tax Officer, (Enforcement) North Zone Belagavi Falls Road, Gokak, Belgaum – Respondent

Writ Petition No. 100780 of 2024 (T-RES)

Decided On : 24-11-2025

| Table of Content |

|---|

| 1. petitioner's claims for writs. (Para 1 , 2) |

| 2. court's analysis of issues related to gst and university fees. (Para 3) |

ORDER :

M.NAGAPRASANNA, J.

The petitioner is before this Court seeking the following prayers:

“(A) Issue a writ of certiorari or any other writ or direction or order to quash the impugned order dated 30.12.2023 passed by then Respondent No.1, enclosed as Annexure A for the reasons stated in the grounds.

(B) Issue a writ of certiorari or any other writ or direction or order to quash the impugned show cause notice bearing number no. CTO(ENF)GKK/2023-24/B-228 for the period 2018- 19 issued by the Respondent No. 1 enclosed as Annexure B.

(C) Issue a writ of certiorari or any other writ or direction or order to declare Notification No. 13/2022-CT dated 5.07.2022, issued by Respondent No. 2, enclosed as Annexure C, as ultra-vires Section 168A of CGST Act, 2017 for the reasons stated in the grounds.

(D) Issue a writ of certiorari or any other writ or direction or order to declare Notification No. 9/2023-CT dated 31 March 2023, issued by Respondent No. 2, enclosed as Annexure C1, as ultra-vires Section 168A of CGST Act, 2017 for the reasons stated in the grounds.

(E) Issue a writ of certiorari or any other writ or direction or order to declare Notification No. 08/2022 dated 12.07.2022, issued by Respondent No. 3, enclosed as Annexure D, as ultra-vires Section 168A of KGST Act, 2017 for the reasons stated in the grounds.

(F) Issue a writ of certiorari or any other writ or direction or order to declare Notification No. 06/2023 dated 06.04.2023, issued by Respondent No. 3, enclosed as Annexure D1, as ultra-vires Section 168A of KGST Act, 2017 for the reasons stated in the grounds.

(G) Issue a writ or direction in the nature of a writ of certiorari or any other writ or direction to quash Impugned show cause notice bearing no. Show Cause dated Notice No. ACCT9ENF)/GKK/DC0123- 24/323 12.03.2024 issued by Respondent No.4, enclosed as Annexure S, for the reasons stated in the grounds.

(H) Issue a writ of certiorari or any other writ or direction or order to quash clarifications issued vide paragraph 4 (iii) of the CBIC circular No. 151/07/2021-GST dated 17.06.2021 issued by the 6th Respondent enclosed/as Annexure T, for the reasons stated in the grounds.

(I) Issue a writ of certiorari or any other writ or direction or Order to quash the Order No. impugned CTO/ENF/GKK/730Order/2024-25/8 dated 29.04.2024 passed by Respondent No. 1, enclosed as Annexure U.

(J) Issue a writ of certiorari or any other writ or direction or order to quash the impugned order bearing RFN: MA2908242 14563Q-461 along with summary orders issued under FORM GST DRC-07 bearing reference No. ZD290824094274W, ZD290824094299K and ZD290824094315Y dated on 27.08.2024 for the financial year 2019-20, 2020-21, 2021-22 passed by Respondent No. 5, enclosed as Annexure V.

(K) That this Hon'ble Court be pleased to issue a Writ of Mandamus or Certiorari, or Writ in the nature of Mandamus or Certiorari, or any other Writ or Order or Direction calling for the records of the Circular 234/28/2024-GST dated 11/10/2024, issued by the Respondent No. 6 enclosed as Annexure W and quash the clarifications relating to affiliation fee more particularly paragraph-2, along with consequential relief and pass any other writ, order or direction as this Hon'ble Court may deem fit and proper in the facts and circumstances of the case and in the interest of justice and equity.

(L) That this Hon'ble Court be pleased to issue a Writ of Mandamus or Certiorari, or Writ in the nature of Mandamus or Certiorari, or any other Writ or Order or Direction calling for the records of the Press note dated 09/09/2024 enclosed as Annexure X and quash the recommendation relating to the affiliation fees more particularly para 6(il) of the Press note along with consequential relief and pass any other writ, order or direction as this Hon'ble Court may deem fit and proper in the facts and circumstances of t

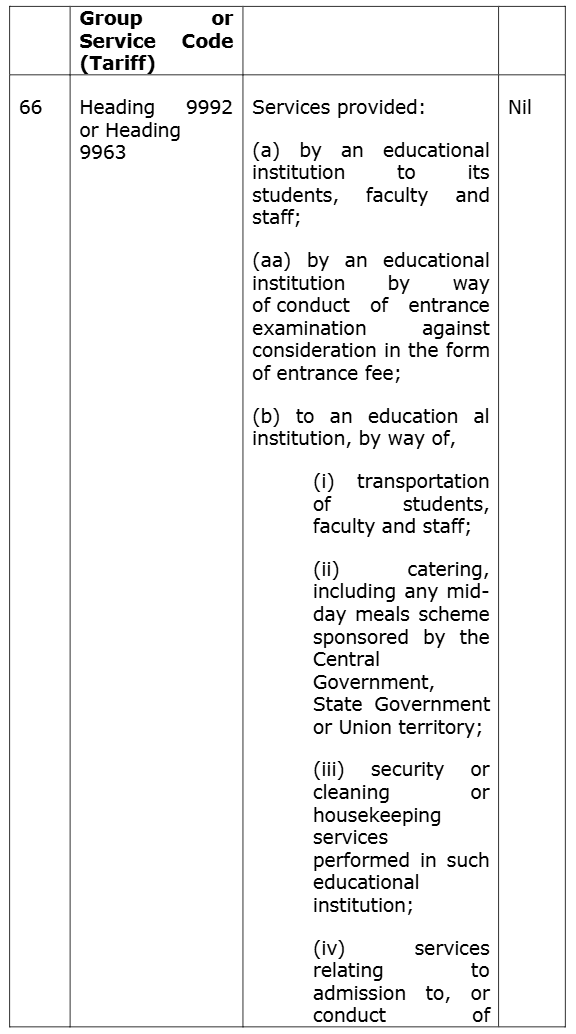

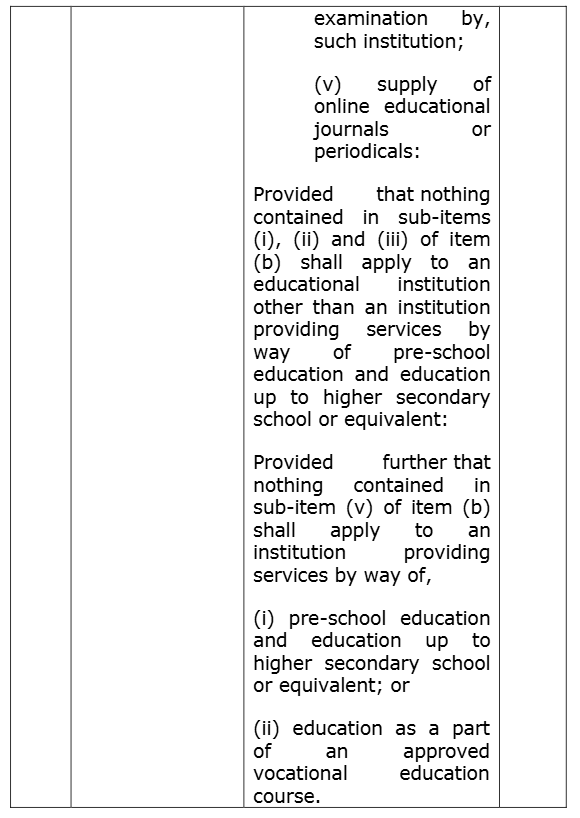

Educational institutions' activities are statutory and not commercial, thus exempt from GST under relevant provisions.

Educational activities, including affiliation fees, are not commercial in nature and thus exempt from GST under the Central Goods and Services Tax Act.

Affiliation fees by statutory universities are statutory/regulatory functions, not 'supply of service' in course/furtherance of business under CGST Act Section 7, hence not taxable under Section 9; e....

The court held that affiliation fees collected by universities from affiliated colleges are taxable under GST, as they do not qualify as exempt educational services related to admission or examinatio....

Educational institutions are exempt from service tax for educational services under the Finance Act, 1994, but not for income from non-educational activities.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :