BEFORE THE MADURAI BENCH OF MADRAS HIGH COURT

G. Jayachandran, K.K. Ramakrishnan, JJ.

Bharathidasan University, Rep. By its Registrar - Petitioner

Versus

The Joint Commissioner of GST (ST-Intelligence) Trichy Division - Respondent

W.P.(MD)Nos.27453, 27456 to 27458 of 2025 and W.M.P.(MD)Nos.21370, 21371, 21379, 21381, 21395, 21396, 21376

Decided On : 10-02-2026

| Table of Content |

|---|

| 1. tax exemption for university affiliation fees contested. (Para 1 , 2) |

| 2. court reviews previous conflicting judgments on gst applicability. (Para 3 , 4) |

| 3. exemption interpretations laid out in earlier judgments analyzed. (Para 5 , 6) |

| 4. other high court decisions impact gst on affiliation interpretation. (Para 7) |

| 5. affiliation process tied to student admission and exams. (Para 8) |

| 6. affiliation fee deemed taxable under gst. (Para 9) |

ORDER :

G.JAYACHANDRAN, J.

These four writ petitions are directed against the notices of intimation of liability under Section 74(5) of Tamil Nadu Goods and Services Tax Act, 2017 , issued by the Joint Commissioner (ST- Intelligence), Trichy Division calling upon the Bharathidasan University, writ petitioner herein to show cause to the Adjudicating Authority as to why tax due mentioned, together with 18% interest and penalty, should not be levied. Separate notices for the period 2019-2020, 2020-2021, 2021-22 and 2022 – 2023 were issued based on the defects found during the investigation followed by report of the Inspection Officer.

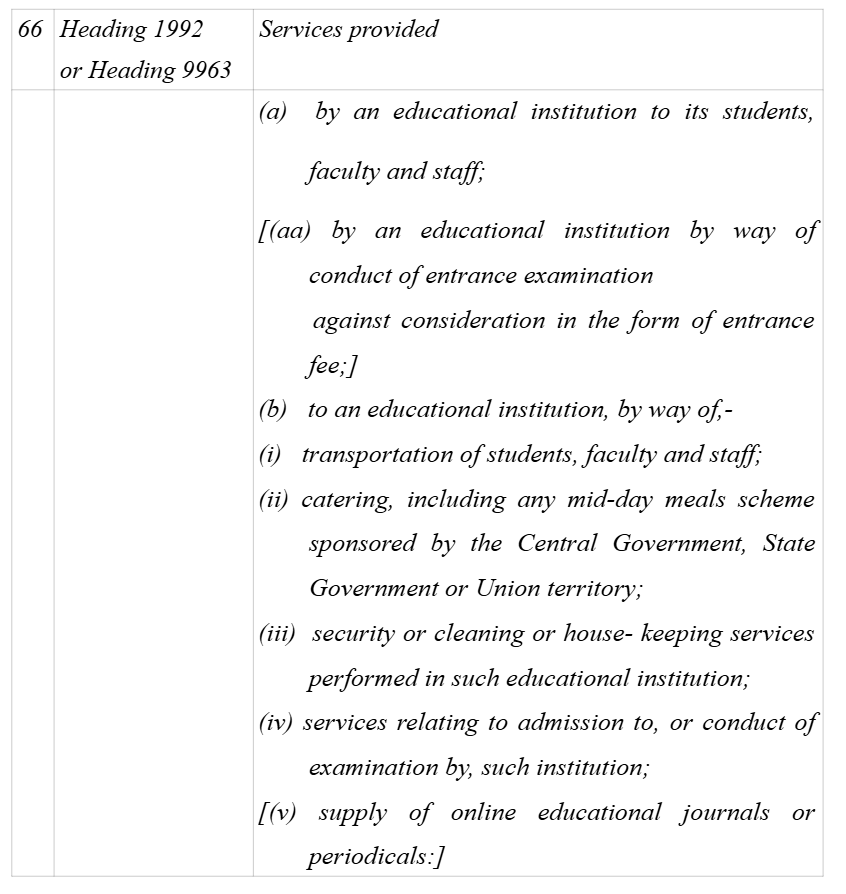

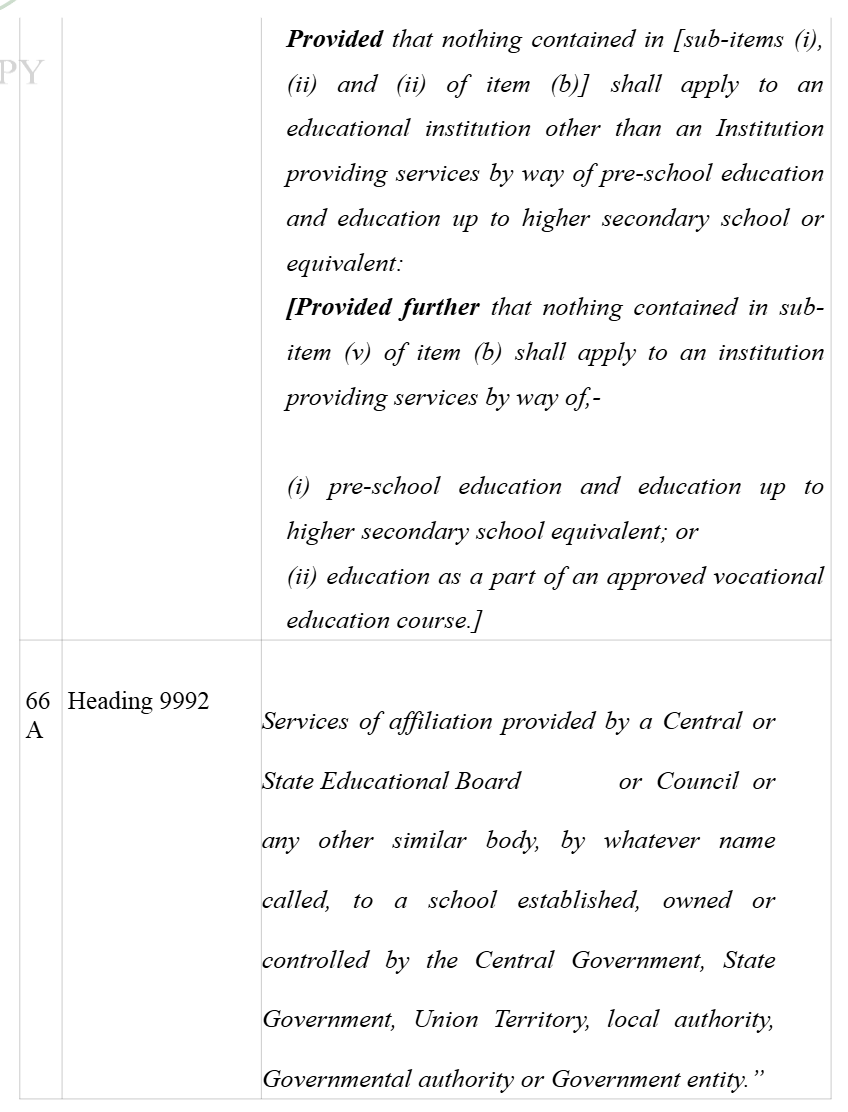

2.The contention of the respondent Department is that the affiliation fees collected by the University is not exempted from Goods and Service Tax (GST) as it is not a service provided to the Students in connection with admission or conduct of examinations. Whereas, the petitioner University contends that affiliation fee collected from the colleges affiliated to the University is for the service provided to the Educational Institutions, which admit students and conduct examination for courses recognised under Law. Therefore, the fees collected for affiliation are exempted from Tax as per notification No.12/2017 dated 28.06.2017.

3.When these writ petitions came up for consideration before the Learned Single Judge, he after noticing that there is cleavage of opinion between Hon'ble Judges of this Court, one Honourable Mr.Justice R.Sureshkumar, who authored W.P.(MD)No.20502 of 2019 in Madurai Kamaraj University –vs- Joint Commissioner vide order dated 16.08.2021 and in W.P.(MD)No.8353 of 2019 and Bharathidasan University –vs- Joint Commissioner of GST and Central Excise, vide order dated 21.09.2021 and another Honourable Mr.Justice C.Saravanan who authored W.P. (MD) No.19587 of 2021 (Manonmaniam Sundaranar University –vs- The Union of India and others), referred the matter to Division Bench for authoritative opinion for consideration of the following term of reference:

“Whether affiliation charges collected by an University from the affiliating Institution is amenable to levy of GST ?” .

4.We have the advantage of reading through the conflicting views expressed by the two Hon'ble Judges of this Court in their judgments cited above. The gist of their view is as under:

4.1.In Madurai Kamarajar Univesity's case, the Hon'ble Mr.Justice R.Sureshkumar, after tracing the history of GST Act qua the purpose of establishing the petitioner University, namely Madurai Kamarajar University, had held that the purposive interpretation of the Act is required while dealing with the provision of exemption for Educational Institutions. When the expression 'conduct of examination' is considered to be the service relating to educational Institutions and exempted from service tax, then the service of granting affiliation to the colleges, which conducts the examination, should also be considered as service relating to educational Institutions. A narrow and pedantic interpretation given by the Advance Ruling Authority would destroy the very concept of providing exemption to the services rendered by the educational Institutions. The word 'Educational Institutions' cannot denote only the college affiliated to the university alone, but it also includes the university which grants affiliation.

4.2.The Hon'ble Mr.Justice C.Saravnana has relied his earlier judgments in W.P.No.15333 of 2020 [Pondicherry University, rep by its Registrar (I/c) vs. The Joint Commissioner of GST, Central Excise, Pondi

The court held that affiliation fees collected by universities from affiliated colleges are taxable under GST, as they do not qualify as exempt educational services related to admission or examinatio....

Affiliation fees by statutory universities are statutory/regulatory functions, not 'supply of service' in course/furtherance of business under CGST Act Section 7, hence not taxable under Section 9; e....

Educational activities, including affiliation fees, are not commercial in nature and thus exempt from GST under the Central Goods and Services Tax Act.

Educational institutions' activities are statutory and not commercial, thus exempt from GST under relevant provisions.

Educational institutions are exempt from service tax for educational services under the Finance Act, 1994, but not for income from non-educational activities.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :