IN THE HIGH COURT AT CALCUTTA

RAJA BASU CHOWDHURY, J.

M/s. Tata Steel Limited (formerly Tata Steel BSL Limited) – Appellant

versus

Union of India & Ors. – Respondent

WPA 20381 of 2024 with WPA 23654 of 2024 with WPA 23659 of 2024 With WPA 23656 of 2024

Decided On : 12-11-2025

| Table of Content |

|---|

| 1. initial filing of writ petitions (Para 1 , 2) |

| 2. details of the petitioner as a corporate entity (Para 3 , 4 , 5 , 6) |

| 3. cenvat credit claims and demands (Para 7 , 8 , 9 , 10 , 11) |

| 4. insolvency proceedings initiated (Para 12 , 14 , 15) |

| 5. resolution plan approval implications (Para 17 , 18 , 19 , 20 , 21) |

| 6. writ petitions addressed to jurisdictional issues (Para 22 , 23 , 24) |

| 7. reversal of cenvat credit as pre-deposit (Para 28 , 30) |

| 8. maintaining jurisdictional clarity in appeals (Para 31 , 32) |

| 9. specificity in legal interpretations and application (Para 33 , 34) |

| 10. determining nature of claims under ibc (Para 35 , 36 , 37 , 38 , 39) |

| 11. constructing claims within permissible legal frameworks (Para 40 , 41 , 42 , 43) |

| 12. ratified claims post-resolution process (Para 44 , 46) |

| 13. balance of repayment and legal proceedings (Para 49 , 51) |

| 14. conclusion of the case with costs implications (Para 52 , 53) |

Judgment :

Raja Basu Chowdhury, J.

1. Challenging the common final order dated 16th April, 2024 passed by the learned Customs, Excise and Service Tax Appellate Tribunal, Eastern Zonal Bench, Kolkata (hereinafter referred to as “CESTAT”) in Excise Appeal Nos.252 of 201, 704 of 2011, 652 of 2012 and 281 of 2011 thereby, holding the appeals to have abated consequent upon the corporate insolvency of the petitioner’s erstwhile entity, M/s. Bhusan Steel Ltd. (hereinafter referred to as the BSL), the instant writ petitions under Article 226/227 have been filed.

2. The writ petitions have since been assigned before this Court by the Hon’ble the Chief Justice vide order dated 7th February, 2025 and are accordingly, taken up for consideration together.

3. The facts giving rise to the instant writ petitions are common and are noted hereinbelow.

4. The petitioner is a company within the meaning of the Companies Act, 2013 (hereinafter referred to as the “Companies Act”) and as is apparent from the cause title of the writ petitions, the petitioner is represented through its Chief Legal counsel namely Mr. Vikash Mittal, a resident in the state of Jharkhand.

5. The petitioner also contends that its directors are citizens of India and thus, entitled to the protection of their fundamental/constitutional and statutory rights though no disclosure as regards the names of such directors have been made.

6. The directors have also not come forward to represent themselves as parties in the writ petitions.

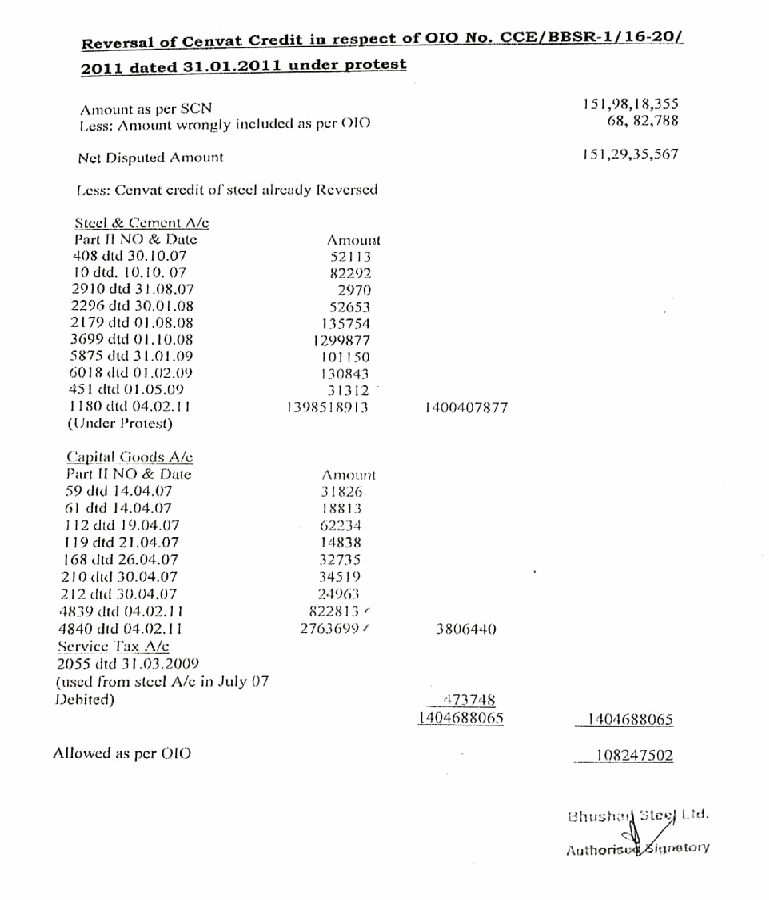

7. According to the petitioner, at all material times BSL had set up a 5.6 MTPA integrated steel plant which included a sponge iron plant having 10 kilns, coke oven plant, blast furnaces, steel making plants, hot rolling mill and cold rolling mill for manufacture and sale of long and flat rolled steel products. The said BSL procured steel structures, parts, accessories and cement to be used in the manufacture of steel structure, prefabricated RCC items, and for making foundations for installing machinery. Accordingly, by treating such items to be ‘capital goods’, the said BSL had taken credit of the duty paid thereon.

8. Subsequently, five several show-cause notices came to be issued on the said BSL covering the periods from August, 2005 to July, 2009, seeking to disallow the CENVAT credit on the aforementioned items for the above periods.

9. From the particulars of the show cause notices which are detailed in the writ petitions, it would demonstrate that a sum of Rs.151,98,18,355/-, Rs.5,01,82,810/-, Rs.4,78,91,060/- and Rs.3,04,17,110/- were claimed and demanded on account of disallowing CENVAT credit for the above period.

10. The show cause notices culminated in the orders in original dated 31st January, 2011, 29th April, 2011, 24th July, 2012 and 4th February, 2011 thereby disallowing CENVAT credit to the extent of Rs.140,46,88,065/-, Rs.2,74,86,476/-, Rs.2,09,40,479/- and Rs.15,46,214/- respectively, alleging that the CENVAT credit availed by the said BSL on the steel structures, parts and accessories as well as cement are “supporting structures” an

The court held that claims involving CENVAT credits were extinguished post-approval of the resolution plan under the Insolvency and Bankruptcy Code, reaffirming jurisdictional limits of the High Cour....

Claims not part of an approved resolution plan under the IBC are extinguished, and appeals cannot abate under Rule 22 when a resolution plan allows for business continuity.

CENVAT credit -As per the mandate of Section 35G of the Central Excise Act; appeals to the High Court can be admitted.

The appellate authority cannot revise its earlier determinations without new grounds, upholding the principle of functus officio in tax matters.

The doctrine of functus officio limits a quasi-judicial authority's ability to revisit final decisions, ensuring stability and judicial discipline in legal adjudications.

The approval of a resolution plan under the IBC extinguishes all claims not included in the plan, thereby entitling the petitioner to a refund of pre-deposits made during appeals against extinguished....

The court upheld the mandatory pre-deposit requirement under Section 35F of the Central Excise Act, 1944, emphasizing that financial hardship does not justify waiver of this requirement.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :