IN THE HIGH COURT OF JUDICATURE AT MADRAS

K.MURALI SHANKAR

Tamilnadu Mercantile Bank Ltd. – Appellant

Versus

Venkatrama Subbiah – Respondent

JUDGMENT :

K. Murali Shankar, J.

The Second Appeal is directed against the judgment and decree made in A.S.No.10 of 2018, dated 14.08.2019, on the file of the Principal District Court, Tuticorin, modifying the judgment and decree, passed in O.S.No.23 of 2015, dated 10.08.2017, on the file of the Subordinate Court, Kovilpatti.

2. The appellant is the plaintiff. The plaintiff Bank filed a suit for recovery of mortgage debt due by the deceased first defendant.

3. For the sake of convenience and brevity, the parties will hereinafter be referred as per their status/ranking in their original suit.

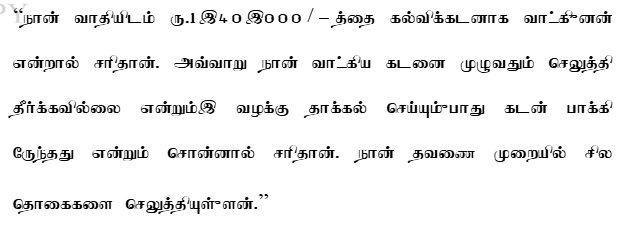

4. The case of the plaintiff Bank is that the defendant applied for a term loan of Rs.1,40,000/- to meet out educational expenses of his daughter V.Rohini to study B.E., Computer Course at Arulmigu Kalasalingam College of Engineering, that the plaintiff sanctioned the said loan on 19.09.2004, that the defendant agreed for the terms and conditions stated in the sanction letter and in thereof, signed in the letter, that the defendant availed the said loan of Rs.1,40,000/- on 24.09.2004 after accepting the terms and conditions of the loan, that the defendant executed a promissory note dated 24.09.2004

Educational loan agreements are enforceable and require documentation for any claims of repayment or entitlement to subsidy benefits; failure to prove eligibility renders claims unsustainable.

The court established that while a lender is entitled to recover loan amounts, the interest rate must be reasonable and within statutory limits, reflecting judicial discretion.

The court emphasized that mortgage interest rates must reflect contractual agreements and market conditions, allowing for discretion in determining reasonable rates beyond the statutory limit.

The court established that mortgage interest rates must reflect contractual agreements and economic realities, allowing for discretion in determining reasonable rates based on inflation and property ....

Borrowers cannot demand specific benefits under One Time Settlement schemes if they fail to properly engage in the process; such benefits are discretionary and not a right.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :