HIGH COURT OF JUDICATURE AT ALLAHABAD

SAUMITRA DAYAL SINGH, INDRAJEET SHUKLA, JJ.

M/s Bambino Agro Industries Ltd. - Petitioner

Versus

State of Uttar Pradesh And Another - Respondent

Writ Tax No. – 2707, 1286, 2399, 2722, 2783, 3098, 3101 of 2025

Decided On : 19-12-2025

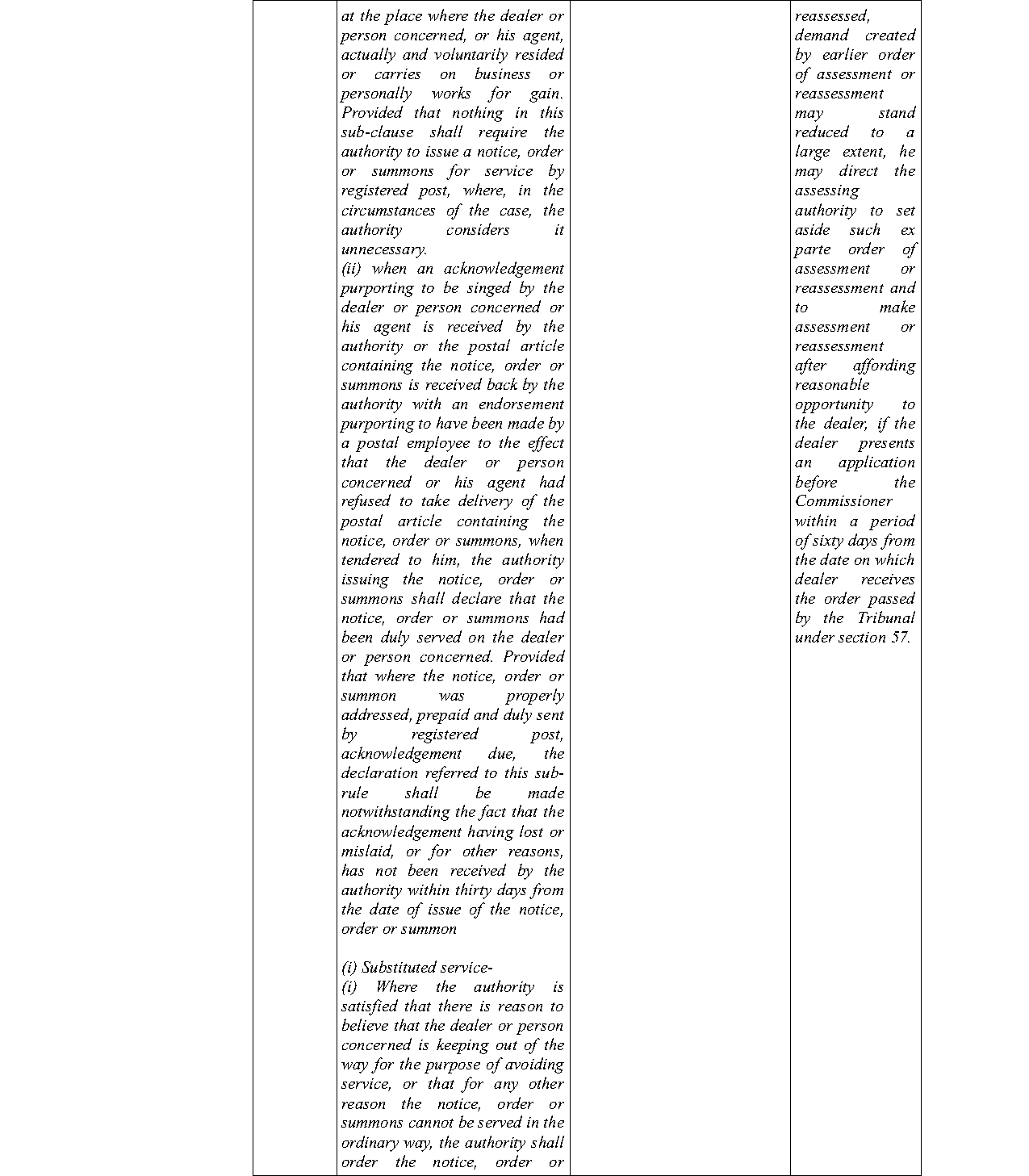

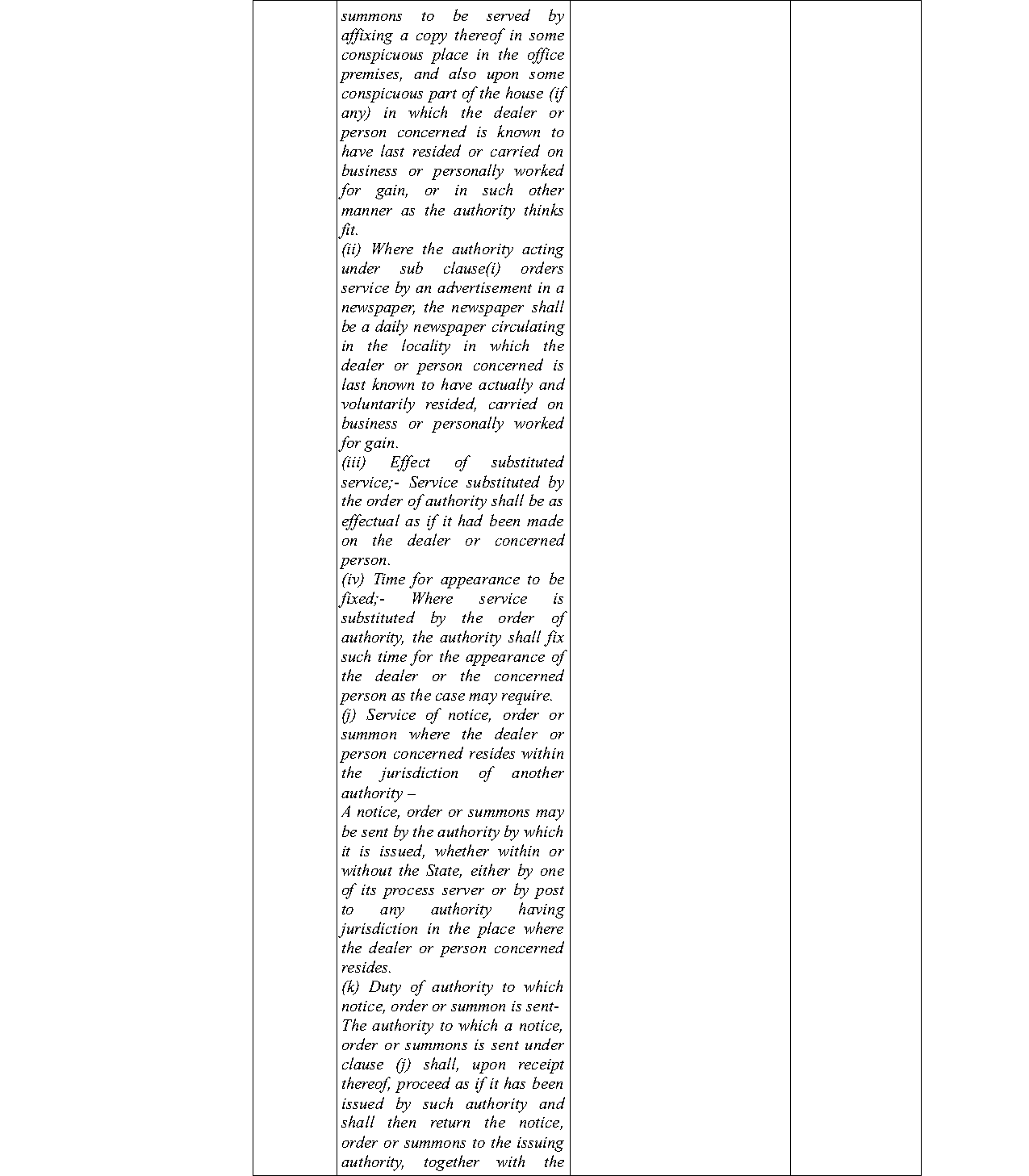

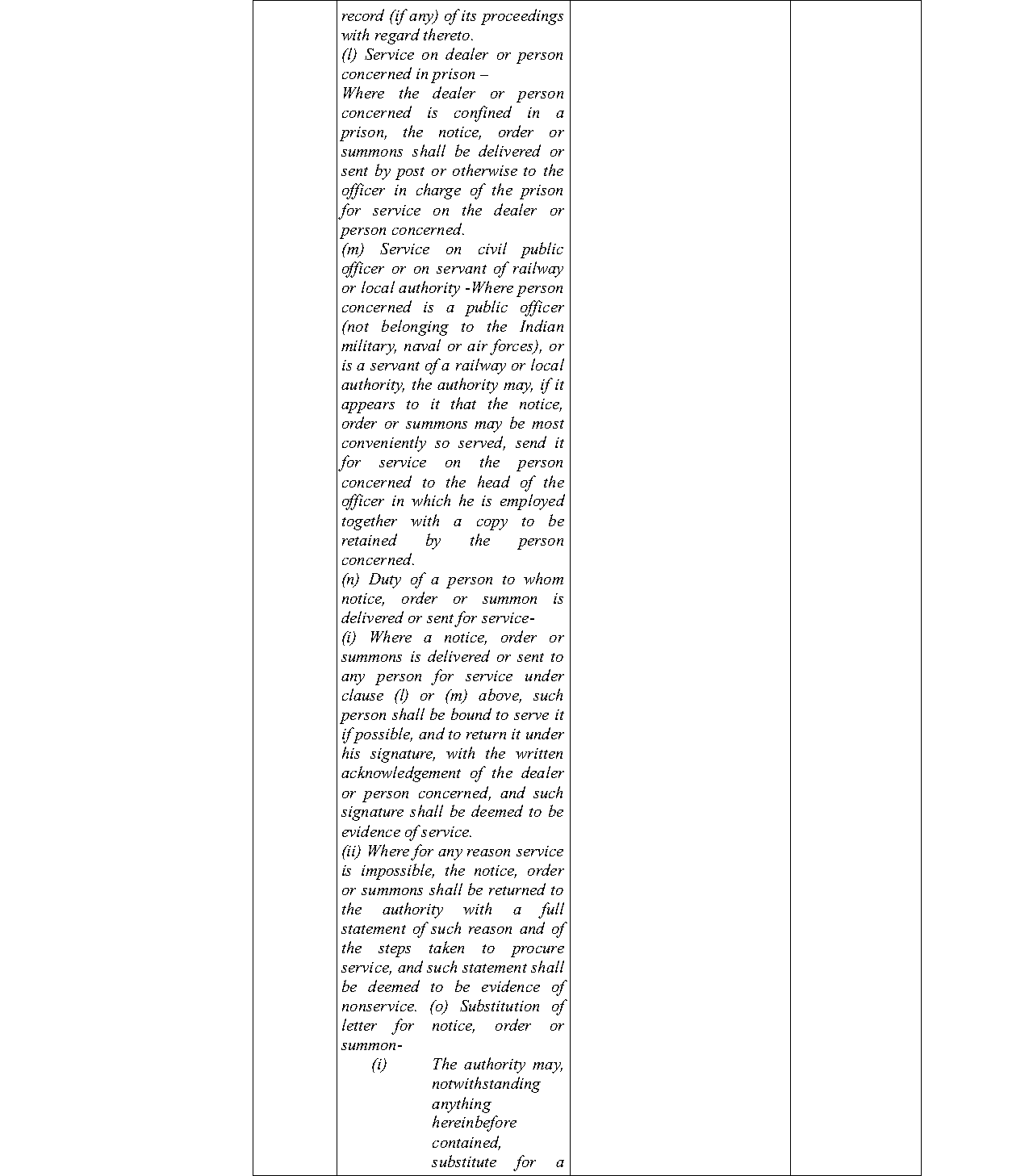

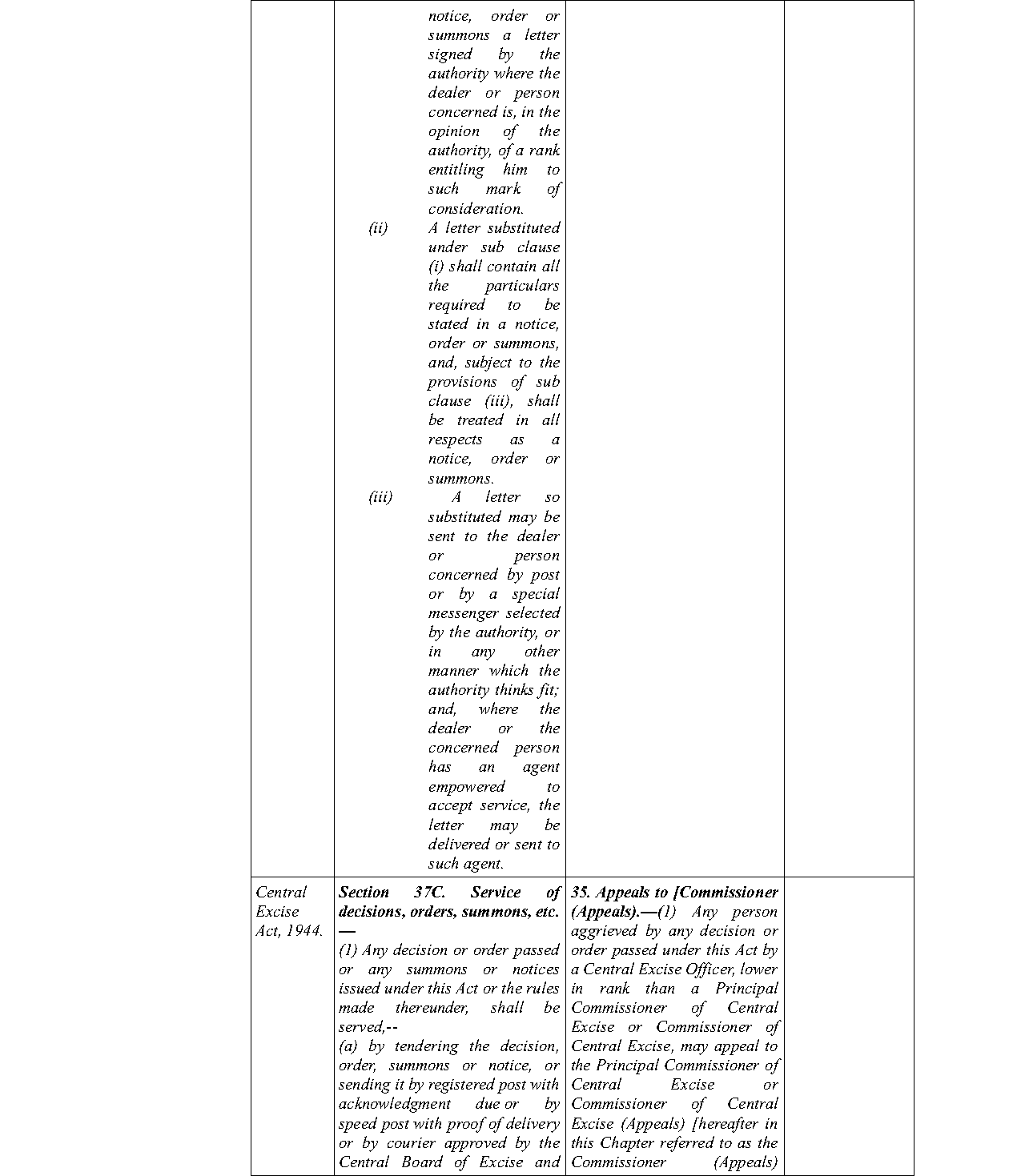

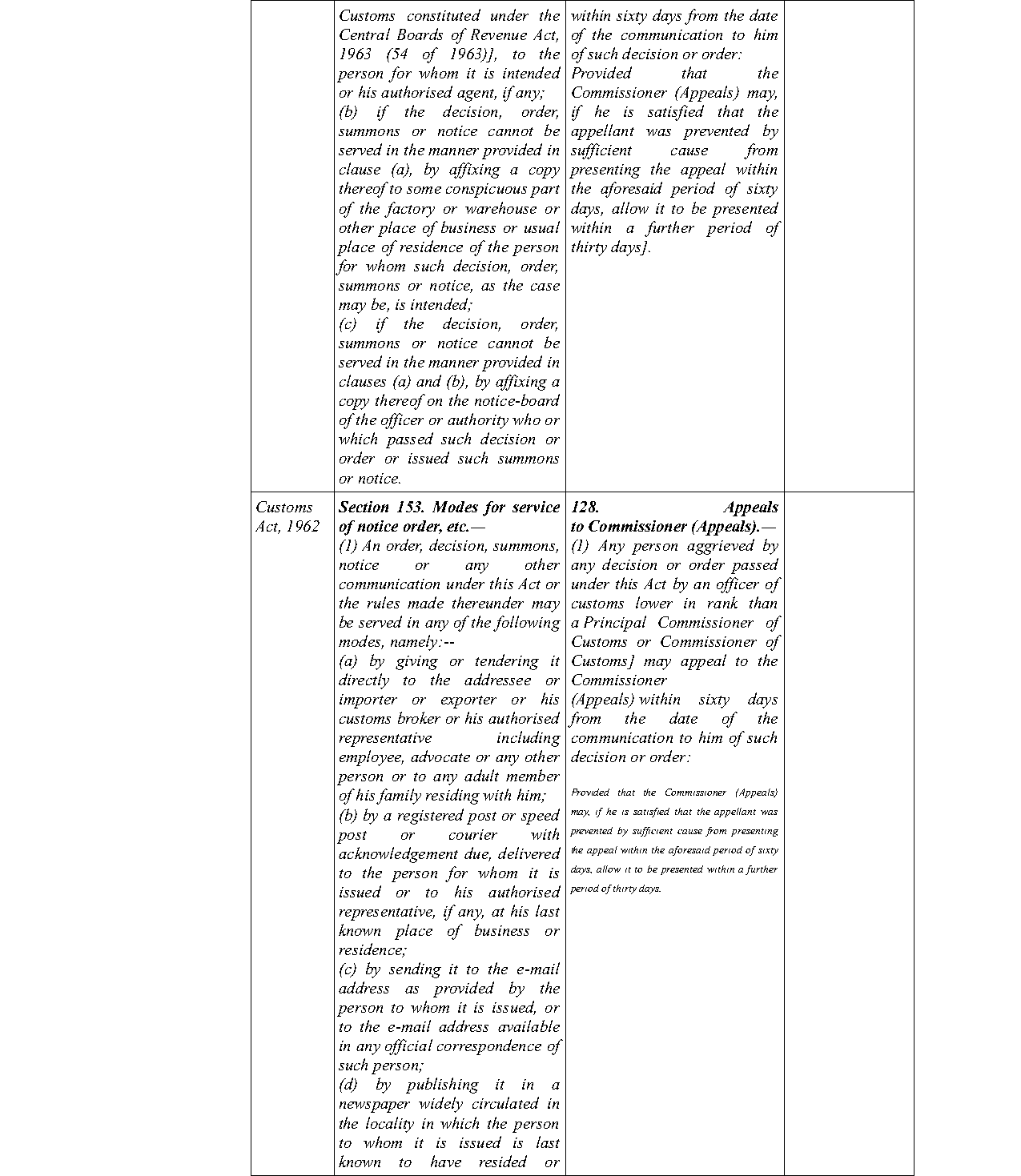

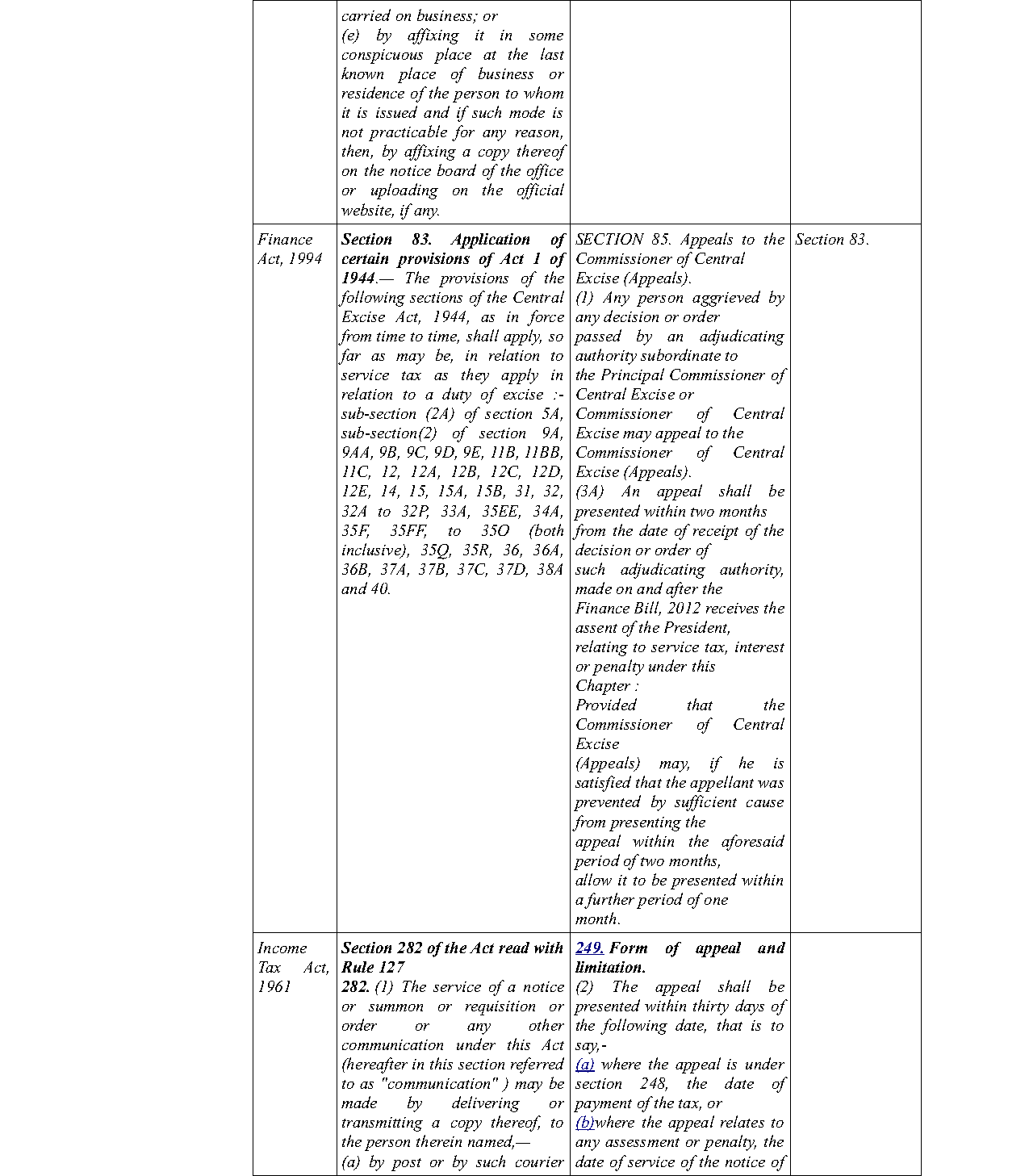

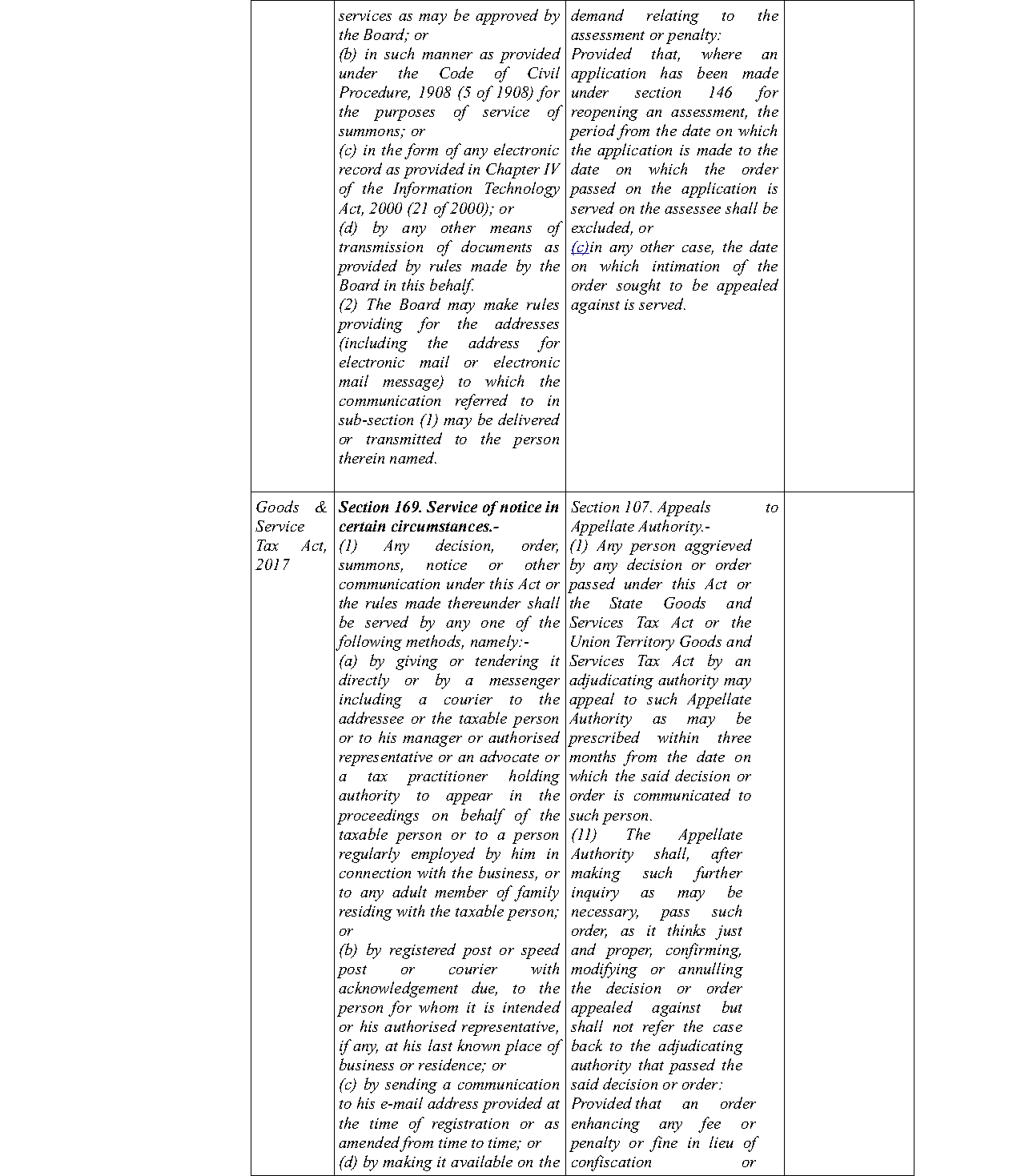

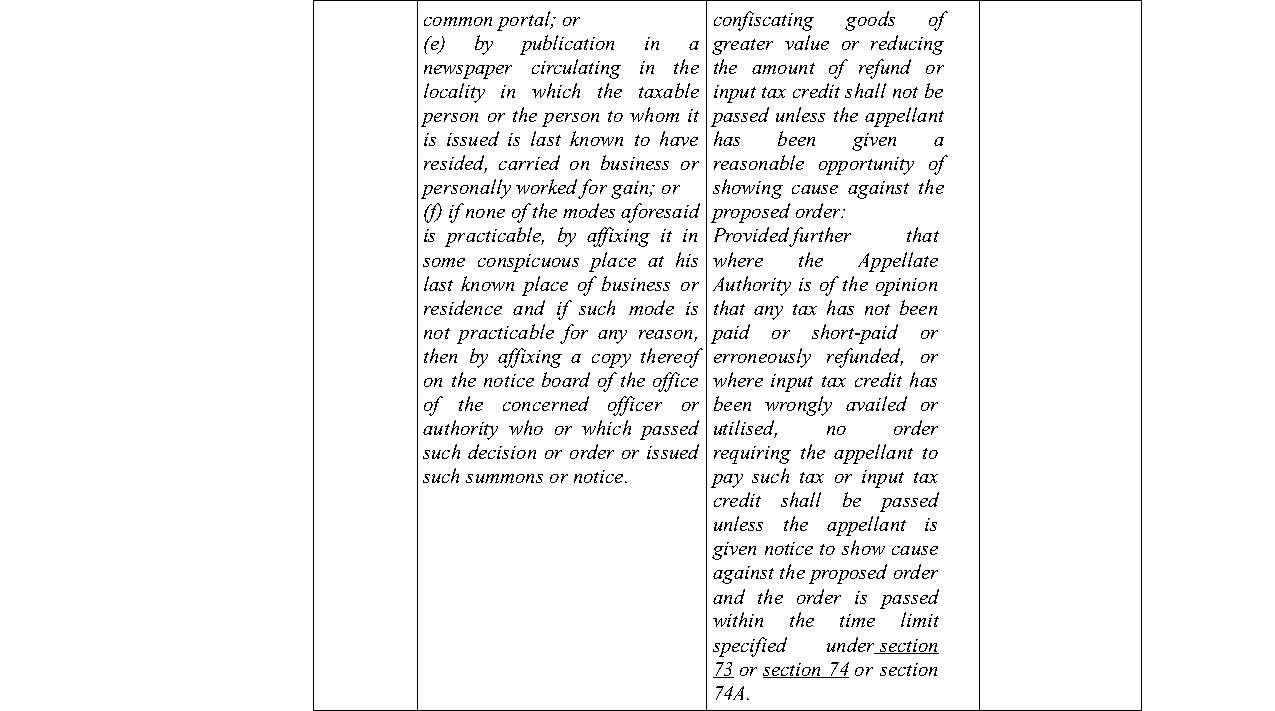

The legal document discusses the communication and service of notices and orders under GST laws, emphasizing that effective communication is essential for the initiation of limitation periods for appeals. The court clarifies that merely uploading notices or orders on the Common Portal does not automatically constitute effective service or communication unless it satisfies specific legal criteria, such as actual or constructive receipt by the noticee.

The document highlights that the methods of service explicitly prescribed in the statutes include physical delivery, registered or speed post with acknowledgment due, or publication in newspapers, with each method having clearly defined legal effects. Uploading notices on the portal or sending email alerts alone do not necessarily amount to service unless accompanied by mechanisms that confirm the notice has been viewed or acknowledged by the recipient.

Further, the court notes the importance of the language used in the statutes, indicating that the phrase “making it available” on the Common Portal does not inherently mean the notice has been ‘served’ or ‘communicated’ in the legal sense. The absence of mechanisms to verify when a notice or order has been accessed or viewed by the recipient renders such electronic uploads insufficient to start limitation periods or to be deemed effective service.

The document also discusses the applicability of the Information Technology Act, clarifying that while it recognizes electronic records and communication, it does not equate uploading a notice on a portal with service or communication unless it meets the criteria of actual or deemed service as per the statutory provisions. The importance of acknowledgment, either explicit or implied, is underscored to establish effective service.

In conclusion, the court allows the writ petitions, setting aside individual adjudication orders, but conditions their validity on the deposit of a specified percentage of tax demand. The orders emphasize the need for the revenue authorities to ensure proper, verifiable methods of service to uphold principles of natural justice and to maintain the integrity of the legal process.

| Table of Content |

|---|

| 1. petitioners challenge adjudication orders under gst. (Para 1 , 3 , 12) |

| 2. communication of orders and its effect on appeal timelines. (Para 2 , 4 , 5 , 6) |

| 3. violation of natural justice and rights of assessees. (Para 13 , 14 , 66) |

| 4. response of state authorities and practical challenges in gst compliance. (Para 15 , 16 , 57) |

JUDGMENT :

(Per Saumitra Dayal Singh, J.)

1. Heard Sri Pranjal Shukla along with Sri Gauransh Mishra and Sri Parth Goswami, Ms. Pooja Talwar, Sri Vedant Agrawal and Sri Rishi Raj Kapoor, Sri Anup Shukla holding brief of Sri Devansh Mishra, Ms. Akashi Agarwal and Sri Vishwaraj Singh on behalf of petitioners; Sri Anoop Trivedi learned Additional Advocate General assisted by Sri Arvind Kumar Mishra and Sri Ankur Agarwal learned Standing Counsel for the State of Uttar Pradesh, Sri S.P. Singh learned ASGI assisted by Sri Gopal Verma for the Union of India and the GSTN, and Sri Gaurav Mahajan and Sri Amit Mahajan for the central revenue authorities. Also, we have taken assistance of Sri Praveen Kumar, as amicus curiae.

2. Present batch of petitions has been filed by different petitioners assailing individual Adjudication Orders passed against them, under the UPGST Act, 2017 (hereinafter referred to as the ‘State Act’) and the CGST Act, 2017 (hereinafter referred to as the ‘Central Act’). At the outset, strong preliminary objection has been raised by the revenue as to maintainability of these petitions. It has been submitted that the Adjudication Orders are appealable. Therefore, the present petitions may not be entertained, and the individual petitioners be relegated to the forum of alternative remedy. Learned counsel for petitioners have met the preliminary objection on the strength of fact assertion that neither the Show Cause Notice nor the Order in Original/Adjudication Order was served on the petitioners, at the relevant time. Only on recoveries being initiated or other consequential steps being taken by the revenue authorities, they acquired knowledge about the Adjudication Orders passed and/or recoveries pressed thereunder. By that time, the hard period of limitation prescribed under Section 107 (1) read with (4) of the State/Central Act, namely, 120 days (including only 30 days for condonation of delay), expired. In face of the law as has been laid down by the Supreme Court in Commissioner of Customs & Central Excise vs Hongo India Pvt. Ltd.; (2009) 5 SCC 791 and Assistant Commissioner (CT) LTU, Kakinada vs Glaxo Smith Kline Consumer Health Care Limited; (2020) 19 SCC 681, the petitioners have been left remediless under the enacted law. Therefore, they have been constrained to approach this Court under its extraordinary writ jurisdiction.

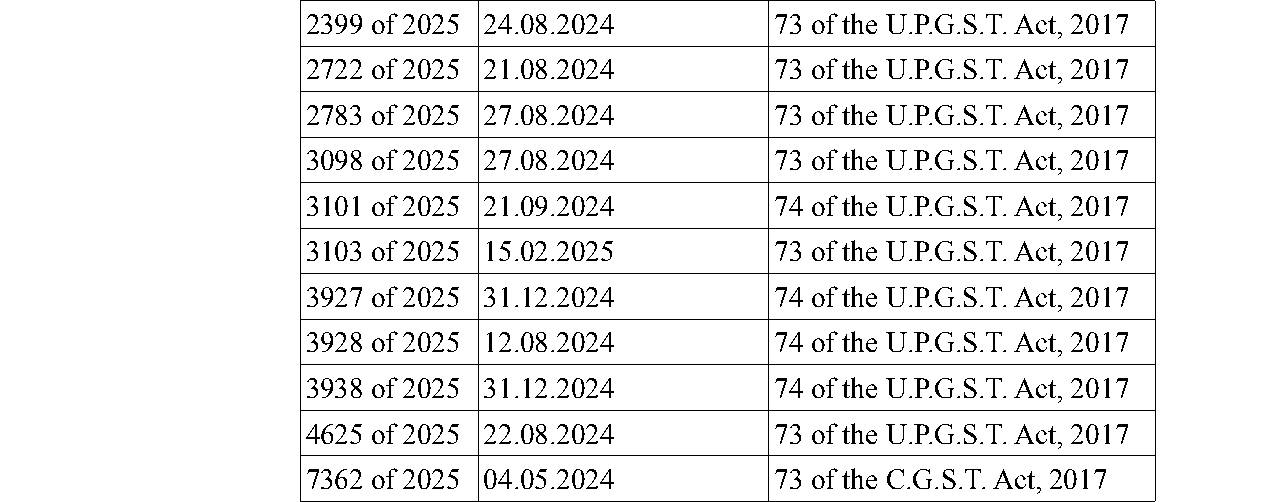

3. In all cases, Adjudication Orders and the Show Cause Notices preceding those orders and the impugned orders are described to have been served on the individual petitioners by the revenue authorities - by uploading and thus making them available on the Common Portal, designed and managed by GSTN, a corporation of Union of India. Details of the Adjudication Orders involved in this batch, together with dates are tabluated below:

4. In such facts, a question has arisen-if the orders impugned in the individual writ petitions have been ‘communicated’ to the individual petitioners, within the meaning of that word used in Section 107 of the State/Central Act? Unless the orders to be appealed are effectively ‘communicated’ to the person aggrieved (by that order), who may then seek an appeal remedy thereagainst, the period of limitation of three months to file such appeal, may not start running.

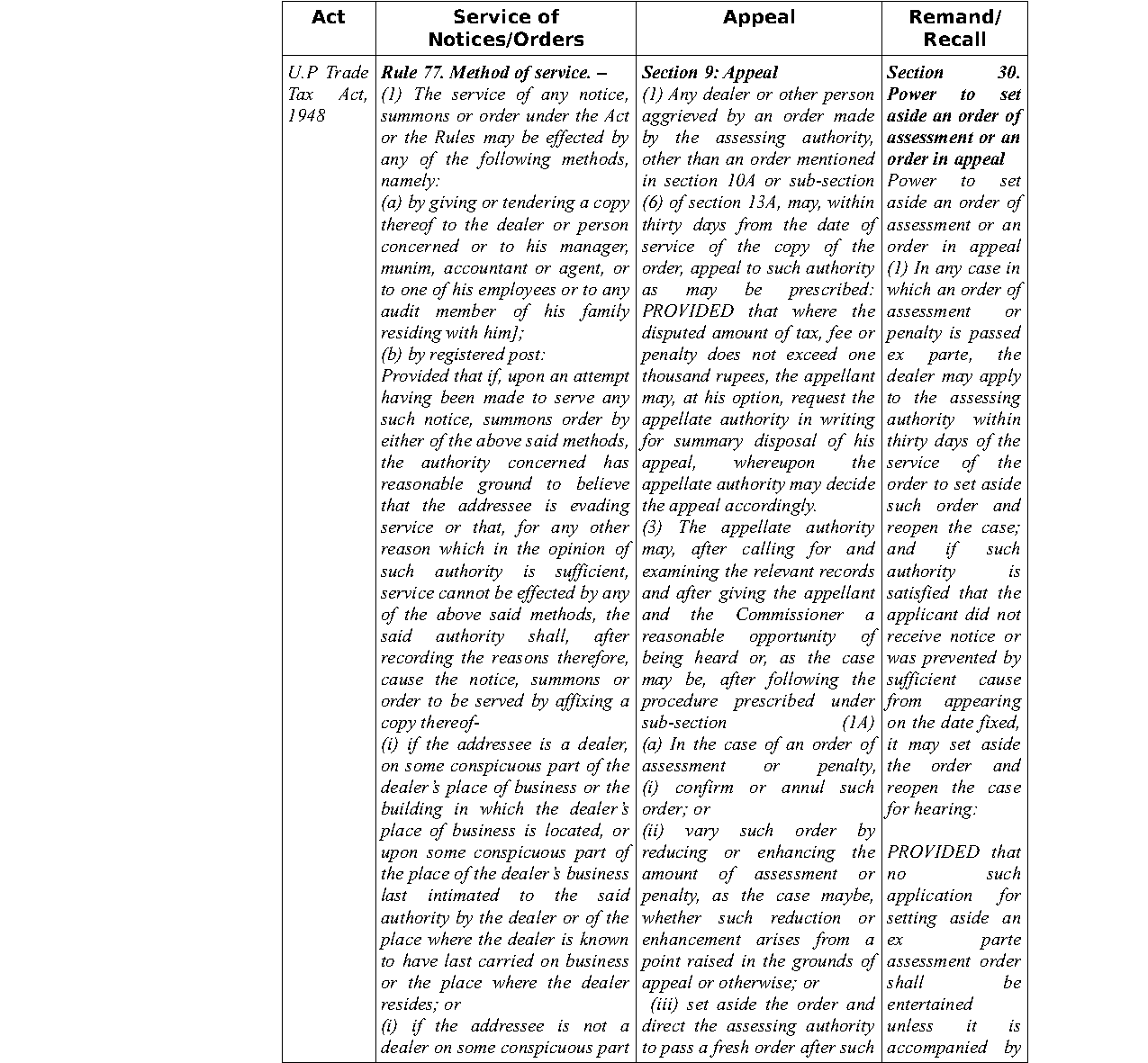

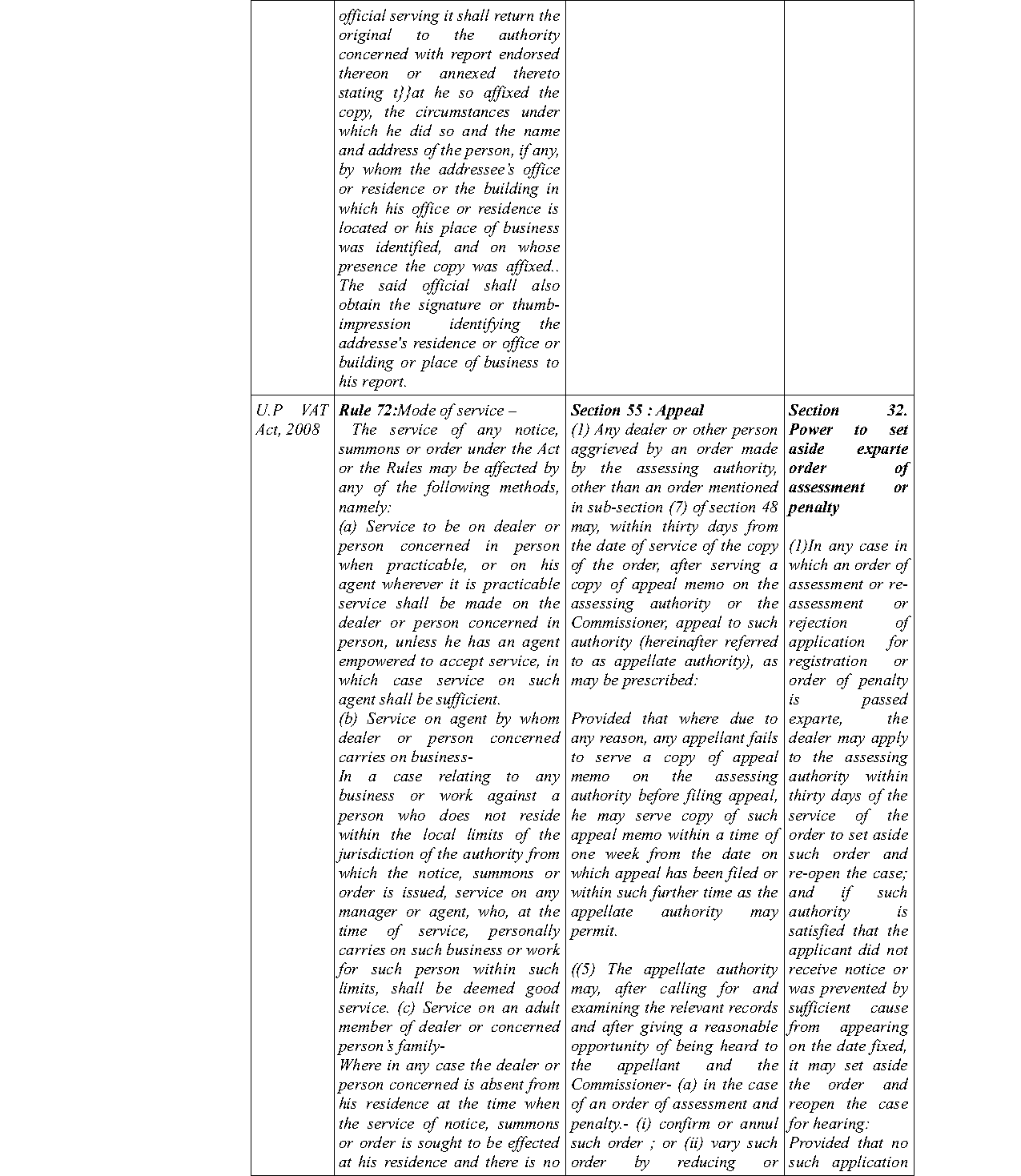

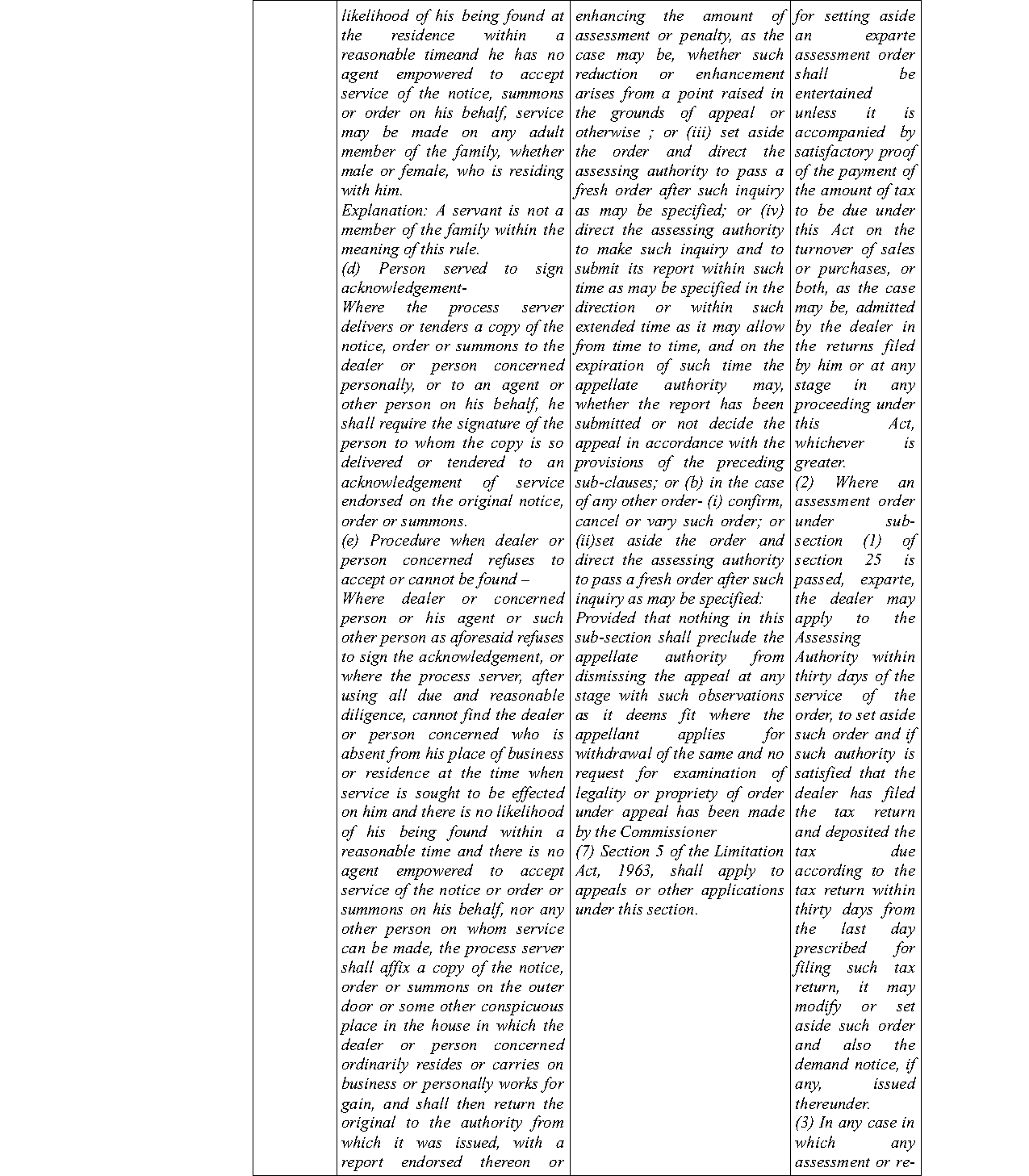

5. The word ‘communicated’ is not defined under the State/Central Act. However, learned counsel appearing for either party have referred to Section 169 of those Acts as also Sections 4, 12 and 13 of the Information Technology Act 2000 (hereinafter referred to as the ‘IT Act’).

6. Seen in that light, a legal issue has arisen - if a Show Cause Notice or other notice or order pa

Effective communication of adjudication orders is essential for initiating limitation under GST laws, and electronic service via the Common Portal alone does not satisfy this requirement.

The court upheld that notification via the common portal is sufficient under Section 169(1)(d) of the GST Act, but emphasized the necessity of effective communication methods to uphold principles of ....

The court held that service of notices via an online portal under an unusual column is insufficient, violating principles of natural justice, leading to the annulment of the ex parte order.

Effective service of notice under the GST Act is critical, with failure to serve properly resulting in quashing of demand and recognition of violation of natural justice principles.

Effective communication of orders is essential for the commencement of the limitation period for appeals under the Central Excise Act.

The failure to provide valid notice and opportunity to be heard constitutes a violation of natural justice, necessitating quashing of ex parte orders under the GST Act.

Section 148 of the Act denotes 'issue of notice where income has escaped assessment'. Once the Assessing Officer has reason to believe that any income chargeable to tax has escaped assessment, then h....

Service tax demands confirmed without valid service of notice violate natural justice principles, leading to appeal's success.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :