IN THE HIGH COURT OF TELANGANA

SUJOY PAUL, ACJ., RENUKA YARA, J.

M/s. Bigleap Technologies And Solutions Pvt. Ltd. And Others - Petitioners

Versus

The State of Telangana And Others - Respondents

Writ Petition Nos. 21101, 5763, 20418, 20827, 20903, 20943, 20997, 21765, 22333, 22334, 22335, 22526, 22571, 22579, 22690, 23341, 26029, 29063, 29415, 29477, 29756, 30022, 31003, 31008, 31025, 31916, 32265, 32914, 32984, 33003, 33054, 33070, 33072, 33086, 33260, 33765, 33905, 33975, 34181, 34598, 35293, 35493, 35503, 35510, 35581, 35593, 35630, 35736, 35904, 35964, 35987, 35989, 36045, 36366, 36375, 36385, 36402, 36421, 36425, 36471, 36581, 36613, 36616, 36620, 36682, 36705, 36730, 36759, 36763, 36776, 36786, 36795, 36799, 36836, 36837, 36910, 36945, 36969, 37051, 37059, 37107 and 37116 of 2024 & 14, 32, 89, 109, 123, 126, 129, 148, 160, 216, 268, 270, 273, 280, 304, 330, 335, 341, 342, 349, 366, 581, 1327, 1430, 1443, 1474, 1476, 1521, 1534, 1537, 1576, 1586, 1614, 1721, 1764, 1774, 1796, 1825, 1998, 2106, 2114, 2116, 2139, 2142, 2170, 2212, 2217, 2246, 2360, 2363, 2530, 2681, 2700, 2716, 2720, 2750, 2780, 2794, 2848, 2864, 2867, 2931, 2939, 2956, 2995, 3000, 3012, 3013, 3015, 3027, 3137, 3150, 3171, 3226, 3252, 4277 and 4491 of 2025

Decided On : 28-02-2025

| Table of Content |

|---|

| 1. examination of the validity of notices absent signatures. (Para 1) |

| 2. legitimacy of show-cause notices without signatures (Para 2 , 3) |

| 3. clarification on validity under gst rules (Para 4 , 5 , 6) |

| 4. understanding statutory interpretations on signatures (Para 7 , 8 , 9) |

| 5. addressing previous case law on signature requirements. (Para 10) |

| 6. counterarguments from petitioners regarding validity (Para 11 , 12 , 14 , 15) |

| 7. the role of statutory requirements for proper authentication. (Para 16) |

| 8. discussion on binding judgments and their applicability (Para 24 , 25 , 26) |

| 9. examination of gst rules and required conditions (Para 27 , 28 , 30) |

| 10. effect of non-signature on document validity (Para 39 , 40 , 41) |

| 11. principle of comity in judicial decisions (Para 43 , 44 , 45) |

| 12. final ruling and consequences for notices without signatures (Para 48 , 49) |

ORDER :

Sujoy Paul, ACJ

In this batch of Writ Petitions, the petitioners have challenged the legality, validity and propriety of the show-cause notices and final orders which admittedly do not contain physical or digital signatures of the Proper Officer, although the impugned show-cause notices and final orders were placed on the portal.

Contention of the Petitioners:-

2. Learned counsel for the petitioners commenced their arguments by placing reliance on the judgment of coordinate Bench of this Court in the case of M/s. Silver Oak Villas LLP v. Assistant Commissioner (ST), [2024 (4) TMI 367-THC]. It is submitted that the view taken in the said judgment was consistently followed in several matters. Therefore, in absence of any physical or digital signature on the impugned show-cause notices and orders, the same cannot sustain judicial scrutiny.

Contention of the Respondents:-

3. Sri Swaroop Oorilla, learned Special Government Pleader for State Tax, at the outset, fairly admitted that the impugned show- cause notices and orders do not contain physical or digital signatures. However, absence of signature will not cause any dent to the said show-cause notices or orders, if the scheme of The Central Goods and Services Act, 2017 (‘GST Act’) and The Central/Telangana State Goods and Services Rules, 2017 (‘GST Rules’) are examined.

4. It was strenuously contended by Sri Swaroop Oorilla that the judgment in M/s. Silver Oak Villas (supra) is founded upon the judgment of the Bombay High Court in Ramani Suchit Malushte v. Union of India , [W.P.No.9331 of 2022 decided on 21st September 2022.]. A careful reading of said judgment makes it clear that the matter was relating to ‘Registration’. Chapter-III of the GST Rules deals with ‘Registration’. This Court in M/s. Silver Oak Villas (supra) not only followed the judgment of Bombay High Court in the case of Ramani Suchit Malushte (supra), but also heavily relied upon Rule 26 (3) of the GST Rules, which clearly provides that it relates to ‘this chapter’ i.e., Chapter-III i.e., ‘Registration’. Thus, the judgment in the case of Ramani Suchit Malushte (supra) and Rule 26 (3) of the GST Rules are of no assistance to the petitioners because neither the said Rule nor the judgment deals with either issuance of show-cause notices or passing of final orders. Thus, the judgment of M/s. Silver Oak Villas (supra) cannot be pressed into service. Reliance is placed on the judgment of learned Single Judge of Gauhati High Court in the case of Dihingia Motors Pvt. Ltd. v. Union of India ,(2025) 26 CENTAX 79 (Gau.) wherein judgment of this Court in M/s. Silver Oak Villas (supra) was considered. Learned Single Judge of Gauhati High Court in the said judgment opined that the manner in which the Proper Officer should authenticate the show-cause notice or order in so far as other Chapters, the GST Rules are silent except Chapter-III, which deals with ‘Registration’. Thus, the view taken in M/s. Silver Oak Villas (supra) is clearly distinguishable and not binding.

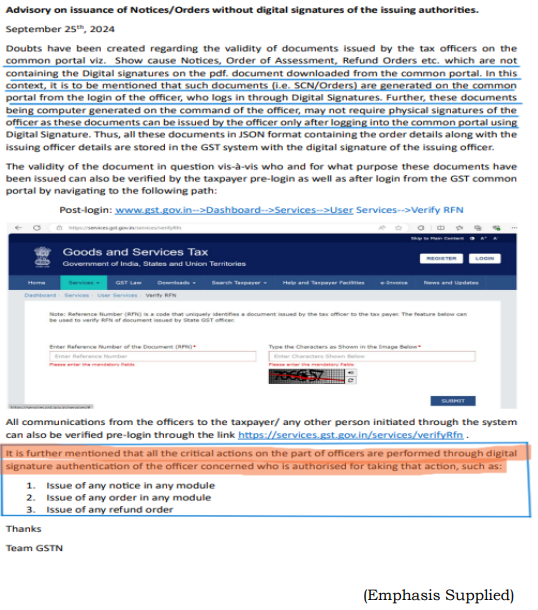

5. It is highlighted that statutory Form issued under Chapter-III are in Form GST REG. Chapter-XVIII of th

Documents lacking requisite signatures from proper officers are invalid under GST regulations, upholding judicial precedents that highlight procedural integrity.

A Summary of Show Cause Notice cannot replace a proper Show Cause Notice, and failure to provide a hearing violates natural justice principles.

Unsigned orders uploaded on the GST Portal are valid due to proper authentication, and the petitioner failed to show due diligence in addressing tax obligations post-registration cancellation.

The main legal point established in the judgment is that an unsigned order cannot be enforced, and the provisions of Sec. 160 and Sec. 169 of the CGST Act, 2017 were not applicable in this case.

Unsigned notice u/s.148 without issuing authority's signature violates mandatory Section 282A(1), rendering it void ab initio and depriving jurisdiction for reassessment, regardless of electronic mod....

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :